- Zinc ingot prices decline on weak domestic sentiment

- Import premiums and LME trends cap downside risks

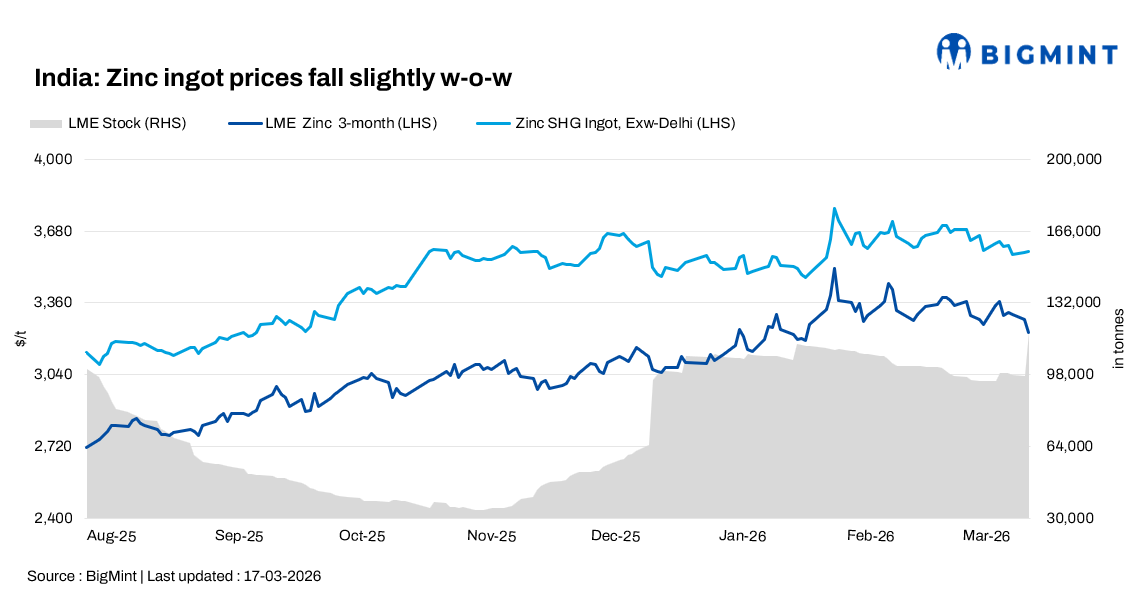

India’s zinc ingot (99.995%) prices declined by INR 2,600/t week-on-week to INR 331,600/t ex-Delhi as of 17 March, reflecting subdued domestic sentiment despite relatively firm global cues. A recent price cut by a leading domestic producer to INR 340,000/t ex-Chanderiya reinforced bearishness. Meanwhile, LME three-month zinc futures eased by $39/t w-o-w to $3,327/t, offering limited external support.

Spot market trends

Domestic spot offers weakened, with SHG zinc ingots at around INR 325,000/t ex-Mumbai, down INR 4,000/t w-o-w. However, import dynamics remained firm, with Australian-origin premiums steady at $240/t over LME on a CFR JNPT basis. In north India, Australian-origin zinc was quoted at INR 355,000-356,000/t ex-Delhi, supported by improved buying interest. Iran-origin material hovered at INR 323,000-324,000/t, narrowing the spread with domestic prices.

Downstream alloy prices mirrored the correction, with Zamak 3 assessed at INR 334,000-335,000/t and Zamak 5 near INR 339,000/t ex-works. A Delhi-based alloy producer noted that easing zinc prices have marginally reduced input cost pressures, though demand remains steady.

Coated steel segment strengthens

In contrast, coated flat steel prices moved higher w-o-w, driven by mill hikes and tight availability. GP prices rose by INR 600-1,800/t to INR 72,000/t, PPGI increased by INR 400-1,100/t to INR 77,500-78,500/t, and BGL surged by INR 1,500-2,800/t to INR 82,700/t. Trading activity improved amid expectations of further hikes.

However, supply-side concerns persist, with propane and RLNG shortages likely to disrupt production. HRC prices also strengthened to INR 55,500/t, supporting coated segment realizations.

Outlook

Domestic zinc prices are likely to remain range-bound to weak in the near term, pressured by HZL’s price cut and softer spot offers, particularly as SHG material continues to trade below replacement cost benchmarks. However, sustained import premiums at $240/t and improving traction for Australian-origin material in north India indicate underlying supply tightness, which may prevent a steep correction.

Leave a Reply