- Domestic zinc prices increase by INR 7,000/t w-o-w

- Import availability tight, with limited exports by Asian producers

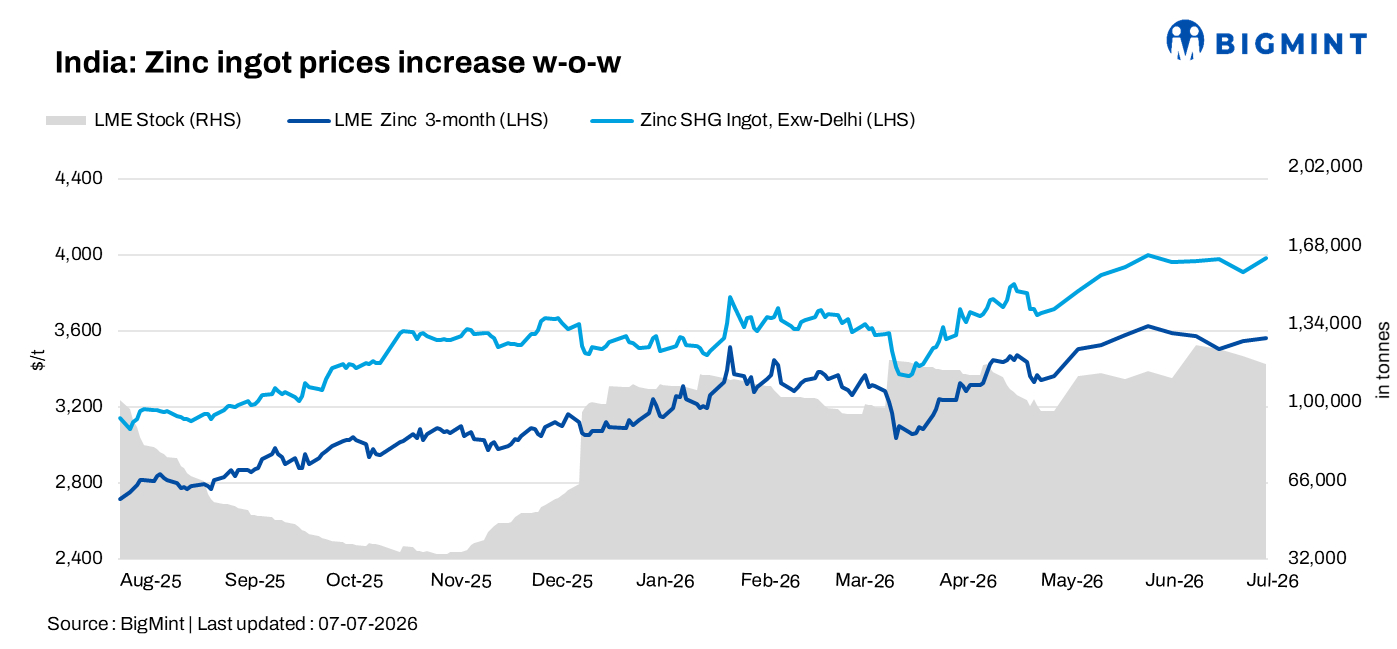

India’s zinc ingot (99.995%) prices increased by INR 7,000/t w-o-w to INR 377,000/t ex-Delhi, according to BigMint’s latest assessment. The recovery was supported by a rebound in domestic benchmark prices following Hindustan Zinc Ltd’s (HZL) upward revision, alongside firmer global zinc fundamentals and continued tightness in imported material availability. Despite the price increase, downstream demand from galvanisers and alloy manufacturers remained largely need-based, with buyers continuing to procure cautiously amid the ongoing monsoon season.

HZL’s upward revision supports domestic market

Domestic market sentiment improved after HZL increased zinc ingot prices by INR 300/t on 6 July compared with its previous revision announced on 1 July. Following the latest revision, the producer’s benchmark Special High Grade (SHG) zinc prices rose to INR 374,800/t.

Although the revision was modest, market participants noted that it reinforced confidence after the sharp corrections witnessed in the previous week. Buyers continued to limit purchases to immediate requirements, while traders observed relatively balanced physical availability across the market.

Meanwhile, global market fundamentals remained supportive. LME three-month zinc prices increased to $3,562/t on 7 July from $3,546/t a week earlier, while cash settlement prices eased marginally to $3,560/t from $3,565.5/t over the same period. LME zinc inventories, however, declined further to 116,350 t from 119,825 t, extending the drawdown in exchange stocks and indicating continued tightening in global availability.

Import market remains firm on constrained supply

Activity in the imported zinc market remained moderate as limited overseas availability continued to support offers despite subdued domestic buying.

South Korean premiums were heard around $270-280/t, reflecting continued tightness in the concentrate market and constrained export availability from major Asian suppliers.

Australian-origin zinc ingots were offered near INR 385,000-386,000/t ex-Delhi, while Korean-origin material was heard at around INR 375,000-376,000/t, remaining competitive for domestic consumers despite the recovery in local prices.

Market participants indicated that import availability remained relatively tight, with limited export volumes from key Asian producers continuing to underpin premiums. However, monsoon-related slowdown in downstream consumption kept buying interest largely restricted to immediate requirements.

Alloy and coated steel market

Downstream alloy prices strengthened in line with the recovery in zinc values. Zamak 3 was assessed at INR 387,000/t, while Zamak 5 stood at INR 394,000/t ex-works. Primary metal ingot (PMI) was assessed at INR 331,000-332,000/kg. Demand from die-casting and engineering sectors remained moderate, with consumers continuing to procure primarily against confirmed orders.

In the coated steel segment, market sentiment remained subdued.

BigMint’s benchmark assessment for Mumbai GP coil (0.8mm/CTL, 120 GSM, IS 277) declined by INR 700/t w-o-w to INR 74,600/t. The correction was driven by subdued buying activity, ample inventory availability across the supply chain, and cautious procurement by buyers awaiting July mill price revisions.

Mumbai PPGI (0.5mm/CTL, 90 GSM, IS 14246) decreased by INR 300/t to INR 85,200/t amid slow order inflows and limited spot buying, while buyers continued restricting purchases to immediate requirements.

Meanwhile, Mumbai BGL (0.5mm/CTL, 1220mm, AZ150) fell by INR 200/t to INR 89,500/t, reflecting competitive offers, cautious buyer sentiment, muted bookings, and comfortable market availability.

Outlook

India’s zinc ingot market is expected to remain cautiously firm in the near term. HZL’s latest upward revision, strengthening domestic prices, declining LME inventories and constrained import availability are likely to provide underlying support. However, ongoing monsoon-related disruptions, adequate spot availability and continued need-based procurement by downstream consumers are expected to limit aggressive price gains. Market participants will continue to monitor HZL’s pricing strategy, global inventory trends, import supply conditions and the pace of post-monsoon demand recovery for clearer market direction.

Leave a Reply