- Australian zinc premiums inflated despite muted demand

- Heavy July-August imports weigh on domestic trade

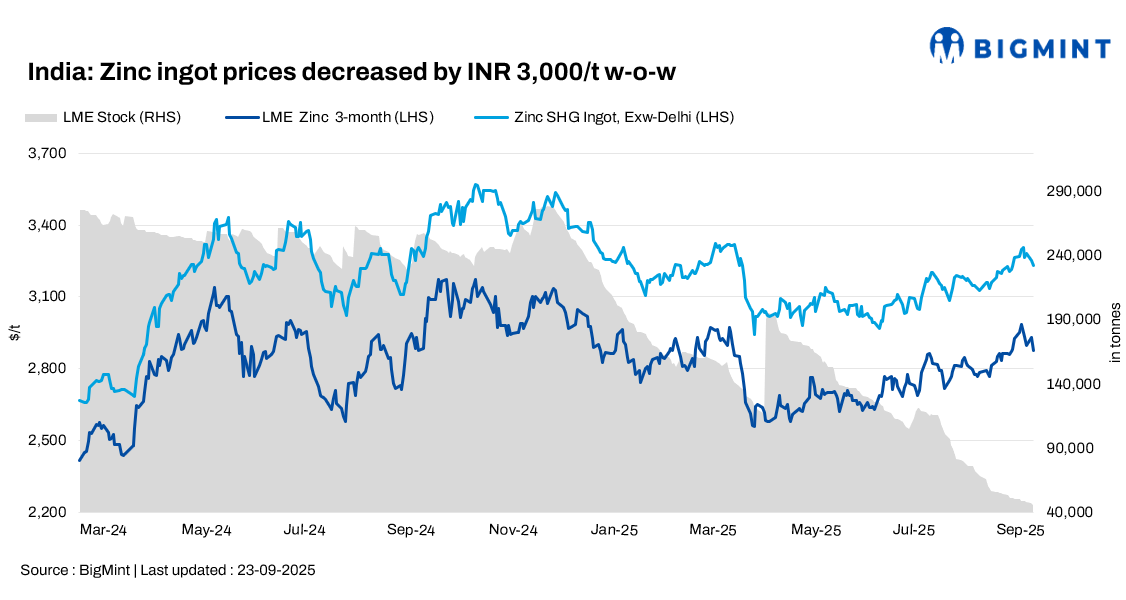

India’s zinc ingot (99.995%) prices slipped by INR 3,000/tonne (t) week-on-week to INR 287,000/t ex-Delhi, according to BigMint’s assessment. The fall reflects oversupply from recent import surges, weak buying interest, and downward adjustments in official pricing by Hindustan Zinc Limited (HZL).

On 22 September 2025, HZL reduced zinc ingot prices by INR 4,500/t ($51/t) compared with 18 September, fixing revised tags at INR 302,200/t ($3,457/t) ex-Chanderiya. In the spot market, SHG zinc ingots were offered at INR 280,000/t ex-Mumbai, while Australian zinc was quoted at INR 365,000/t ex-Delhi, down INR 10,000/t week-on-week.

Import glut weighs on market

India’s zinc market has been unsettled by a sharp inflow of semi-finished ingots. Imports surged to 32,000 tonnes in July–twice the monthly average–and an estimated 25,000 tonnes in August, creating a glut that disrupted trading and left buyers hesitant.

Although some traders continue quoting Australian zinc premiums as high as $750/t, most market participants reject these levels, pointing to more realistic values near $400/t.

“The market is oversupplied and buyers are reluctant to take positions. Imported stocks are piling up, and liquidity is tight, so no one wants to overcommit,” said a Delhi-based zinc trader.

“Even at lower offers, demand is sluggish. Galvanizing and oxide units are running below capacity, while alloy makers are only buying in small parcels,” noted a western India ingot dealer.

Coated flat steel market

India’s coated flat steel market remained soft this week. GP coil prices slipped INR 500/t to INR 61,900/t ex-Mumbai, while PPGI dropped INR 400/t to INR 73,100/t. Weak downstream demand and high inventories continue to pressure trade, with recovery prospects uncertain in the near term.

Global and local contexts

India’s semi-finished zinc ingot imports climbed 38% year on year in Jan-Aug 2025 to 171,548 tonnes, compared with 123,996 tonnes a year earlier. The sharp rise highlights stronger inbound supply against muted domestic offtake, reinforcing bearish undertones in the market.

Globally, sentiment stayed subdued. LME three-month zinc futures edged slightly lower, trading at US$2,875-2,885/t on 23 September, pressured by persistent macroeconomic uncertainty. On the Shanghai Futures Exchange, the October zinc contract softened to RMB 22,065/t, as sluggish downstream demand and continued stock build weighed on market confidence.

Outlook

Oversupply pressures are expected to persist near term, with elevated July-August imports continuing to weigh on sentiment. Domestic zinc prices may face further downside unless demand revives from galvanizing, alloy, or infrastructure segments. Import premiums are likely to normalize closer to $350-400/t as inflated offers lose traction.

Leave a Reply