- Domestic zinc prices fall INR 3,300/t w-o-w on cautious buying

- Coated steel demand remains mixed across segments

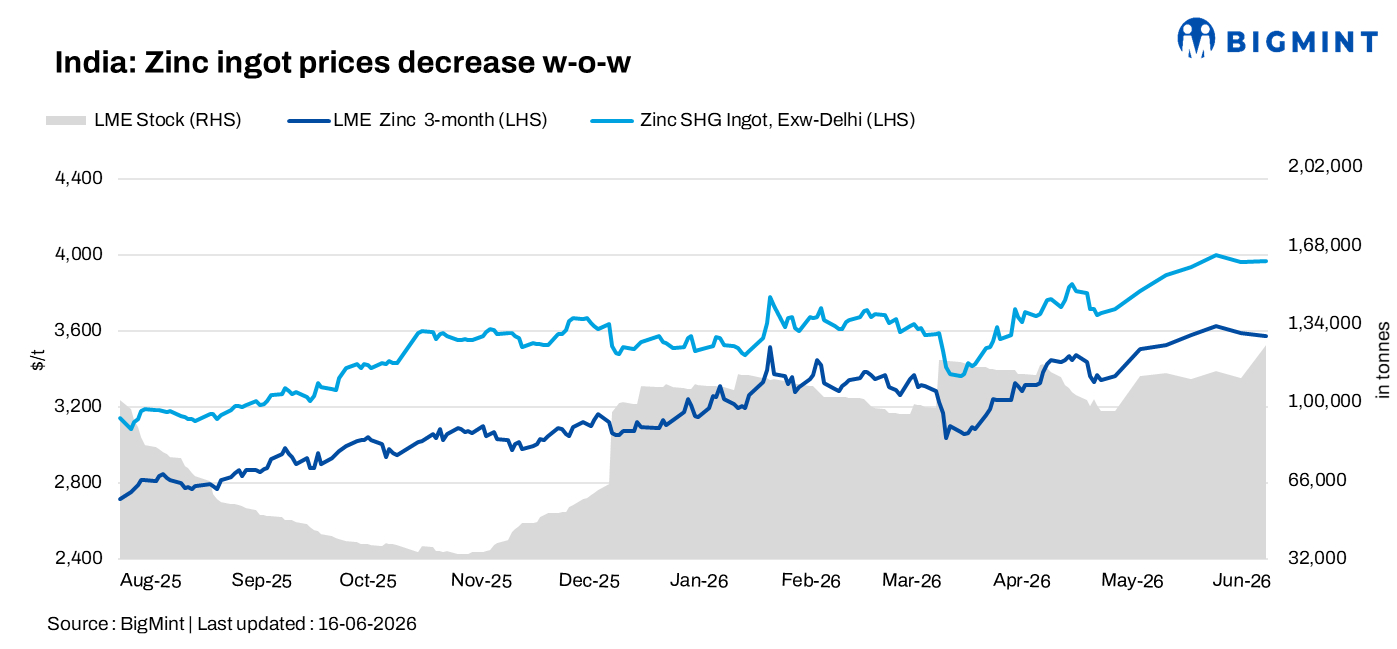

India’s zinc ingot (99.995%) prices declined by INR 3,300/t w-o-w to INR 373,000/t ex-Delhi on 16 June 2026, according to BigMint’s assessment. The downturn was driven by softer producer pricing, weaker London Metal Exchange (LME) trends, and continued cautious buying from galvanisers and alloy manufacturers. Market participants largely restricted procurement to immediate requirements amid subdued downstream consumption and limited visibility on demand recovery.

HZL revision weighs on domestic sentiment

Domestic market sentiment weakened further after Hindustan Zinc Ltd (HZL) reduced zinc ingot prices by INR 2,000/t on 15 June. Following the revision, HZL’s benchmark Special High Grade (SHG) zinc prices stood at INR 375,600/t, narrowing the premium over spot market levels. Market participants indicated that the price correction encouraged buyers to delay bulk purchases in anticipation of further adjustments.

Meanwhile, LME three-month zinc prices eased to $3,571/t on 16 June from $3,588/t a week earlier, while cash settlement prices declined to $3,550/t from $3,576/t. However, LME zinc inventories increased sharply to 124,550 t from 110,400 t over the same period, signalling improved exchange availability.

Import market remains subdued

Trading activity in the imported market remained limited despite stable overseas premiums. South Korean SHG zinc premiums were heard around $260/t, while Australian-origin zinc ingots were offered at approximately INR 376,000/t ex-Delhi. South Korean-origin units were indicated near INR 372,000/t, while PMI-grade zinc was reported at INR 333,000-334,000/t.

Most spot transactions continued to be linked to domestic producer pricing, reflecting adequate local availability and limited appetite for imported material.

Alloy and coated steel market update

Downstream alloy prices remained largely stable despite the weakness in primary zinc. Zamak 3 was assessed at INR 383,000-384,000/t, while Zamak 5 was heard at INR 390,000-391,000/t ex-works.

In the coated steel segment, demand remained mixed. GP coil prices declined by INR 700/t w-o-w to INR 75,800/t amid sluggish bookings. PPGI prices were stable at INR 85,200/t, supported by some pre-monsoon procurement activity. Meanwhile, BGL prices increased by INR 1,200/t to INR 90,500/t due to tighter availability, particularly in thinner gauges.

Outlook

India’s zinc ingot prices are expected to remain range-bound to weak in the near term, pressured by softer producer pricing and cautious downstream buying. While stable alloy demand and tighter availability in certain coated steel segments may provide limited support, ample domestic supply and subdued consumption are likely to restrict any significant upside.

Leave a Reply