- South Korea emerges as largest supplier accounting for over 60% of imports

- Western India drives incremental volumes as coated steel demand strengthens

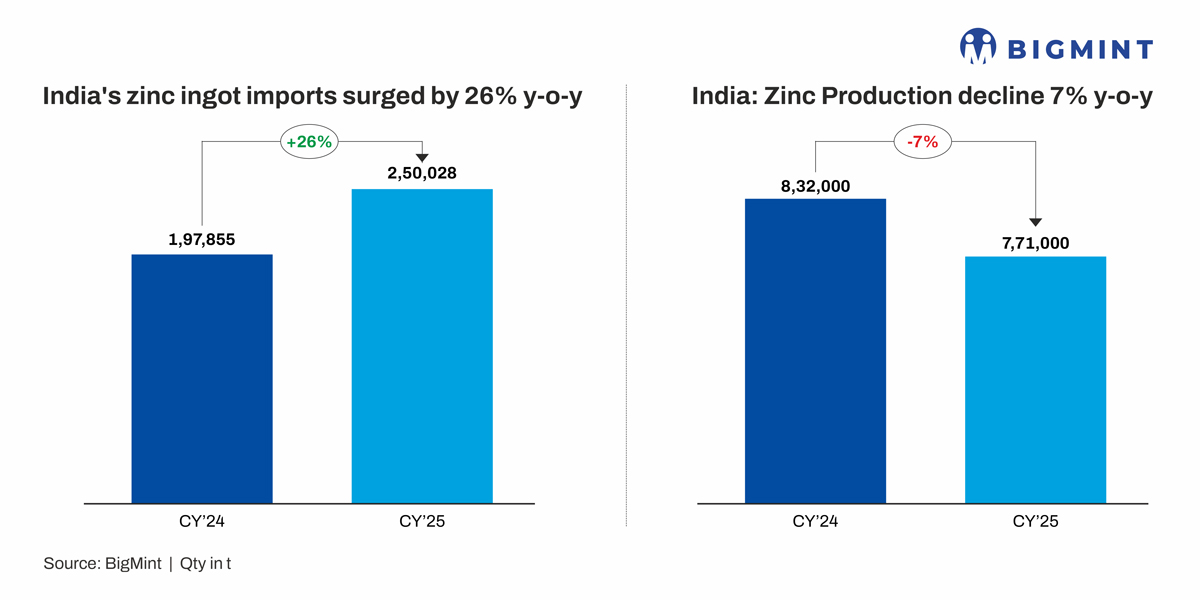

India’s zinc ingot imports rose sharply by 26% y-o-y in CY’25 to 250,030 tonnes (t), compared with 197,855 t in CY’24, driven by robust downstream demand and lower domestic availability. The increase was supported by firm consumption from galvanising, alloying, and coated steel segments, alongside a 7% y-o-y decline in domestic refined zinc production, which fell to 0.77 million tonnes (mnt) in CY’25 from 0.83 mnt a year earlier.

Higher refined zinc prices, intermittent tightness in domestic metal availability, and competitive landed costs encouraged Indian buyers to increase reliance on imported Special High Grade (SHG) zinc ingots, particularly from Asia and Europe.

Top supplying nations

South Korea emerged as India’s largest zinc ingot supplier in CY’25, shipping 153,760 t, accounting for over 60% of total imports. Strong exports from Korean smelters were supported by scale efficiencies, long-term offtake arrangements, and reliable SHG quality.

Japan ranked second with 34,630 t, followed by Singapore (24,920 t) and Spain (14,960 t). Australia supplied 6,680 t, while Switzerland, Norway, UAE, and Finland together contributed smaller but steady volumes. Imports of Indian-origin re-exports stood at 1,350 t, largely linked to merchant trade flows.

Region-wise imports in India

West India remained the largest destination for imported zinc ingots, reflecting the concentration of galvanising and coated steel capacity in the region. Imports into the western region surged to 148,615 t in CY’25 from 102,925 t in CY’24.

East Indian imports also rose notably to 56,145 t, supported by infrastructure-linked galvanising demand.

In contrast, northern India saw a decline to 20,505 t from 23,570 t, while southern India imports remained largely stable at around 24,710 t, indicating relatively balanced regional demand outside the west.

Why are zinc ingot imports rising?

Rising downstream coated steel and galvanising capacity remains the primary driver of higher zinc ingot imports, as these facilities consume significant volumes of zinc for corrosion-protection applications used across automotive, appliances, infrastructure, and construction.

- AM/NS India is expanding its downstream product capacity by over 51% to around 5 mnt per year by end-CY’25, including commissioning a new galvanising line at Hazira, Gujarat, as part of an INR 8,500 crore investment aimed at reducing reliance on imported high-strength coated steel.

- Tata Steel commissioned a new Continuous Galvanising Line (CGL-1) at its Kalinganagar, Odisha complex under its Phase II expansion, increasing plant capacity from 3 mnt/year to 8 mnt with an investment of INR 27,000 crore. The line produces advanced high-strength coated steel for automotive and appliances.

- Jindal Steel launched its first Continuous Galvanising Line (CGL-1) at the Angul plant in Odisha, producing galvanised and galvalume steel under the Jindal Panther and ZINKALUME brands. The company is ramping crude steel capacity towards 12 mnt by end-CY’25 to support coated steel throughput.

These capacity additions point to a structural increase in zinc consumption, underpinning elevated reliance on imported refined metal.

Few alloy producers expanded in CY’25, with stable Zamak output led by CMR Green, while zinc wire activity saw Group Nirmal acquire Cee Dee Metalloys and Ottimo Metals launch high-purity exports.

India zinc demand

India’s zinc demand rose significantly in 2025, growing 6-7% overall to around 783-867,000 t, driven by infrastructure, manufacturing, and urbanisation amid supportive budget allocations. Galvanizing dominated consumption at over 60%, fueled by steel growth in highways, railways, and power projects absorbing HZL’s increased output. Galvanizing consumed over 60% of domestic zinc, boosted by 9.8% higher Union Budget capex (INR 11.20 trillion for 2025-26) on infrastructure like transmission towers and urban development. Steel production expansion ensured robust offtake for corrosion protection in construction and utilities.

Alloying and die-casting sector took 20-25% share, with zinc alloys rising in automotive parts, electronics, and manufacturing; HSBC PMI above 58 sustained momentum as galvanized steel aligned with EV targets. Accounting for 10-15%, zinc oxide demand grew 4-5% CAGR from tires, ceramics, paints, and chemicals, centered in Western India production hubs. Automotive used 15-20% for panels, die-casts, and batteries, with 8-10% y-o-y growth in northern/western EV clusters. Renewables (5-7%) emerged via solar panels and wind towers, eyeing doubled wind usage by 2030.

Supply expansion meets concentrate constraints

Global zinc supply continued to expand in 2025, increasing the risk of structural oversupply. Refined zinc production rose by around 3% y-o-y to 13.8 mnt, supported largely by China, where output climbed over 6% to nearly 6.8 mnt following capacity additions. Outside China, supply growth was aided by the restart of Boliden’s Odda smelter and rising mine output from Russia, Brazil and the Democratic Republic of Congo, including the Kipushi project.

Mine production grew faster than refined output, rising about 5% y-o-y to 12.5 mnt in 2025. India’s Hindustan Zinc recorded its highest-ever first-half production, supported by ramp-ups at the Rampur-Agucha mine and approvals at the Debari smelter. Meanwhile, Glencore advanced its Kidd and CEZinc projects, positioning for further output growth into 2026.

Looking ahead, the ILZSG forecasts zinc mine output to increase by 2.4% to 12.8 mnt in 2026, driven by higher production in Europe, Australia, Brazil, China and the DRC. Additional supply will come from the Aljustrel mine restart in Portugal, Bunker Hill’s Idaho project in the US and the Huoshaoyun mine in China. Refined zinc output is expected to rise similarly to 14.13 mnt, while global demand is projected to grow only 1% to 13.86 mnt, leaving a surplus of around 271,000 t in 2026.

Domestic and global zinc price trends in 2025 vs 2024

In CY’25, LME zinc cash prices strengthened, averaging around $2,867/t, up about 3% y-o-y from the prior year, while the 3-month contract averaged roughly $3,093/t. This resilience came amid sharply contracting visible inventories – LME stocks fell about 54% y-o-y to 113,670 t, with on-warrant stocks dropping over 80% through the year, driving pronounced backwardation and elevated cash premiums. Low inventory levels supported price resilience despite mixed demand signals globally.

India’s SHG zinc ingot prices strengthened on a y-o-y basis in CY’25, supported by firm domestic demand, higher input costs, and supportive global cues. Average BigMint-assessed SHG zinc ingot prices (ex-Delhi) rose 8% y-o-y to around INR 283,300/t from INR 263,500/t in CY’24. In western India, prices increased 7% y-o-y to INR 278,100/t.

Prices gained momentum in the second half of the year, with monthly ex-Delhi prices crossing INR 3,17,000/t in November-December 2025, tracking the rally in LME zinc and tightening global inventories.

Outlook

India’s zinc ingot imports are expected to remain elevated in CY’26, supported by sustained infrastructure spending, continued expansion in galvanising and coated steel capacity, and steady alloy demand. Buyers are likely to prioritise South Korean and Japanese material, while closely monitoring LME volatility, treatment charges, and domestic production dynamics. Any acceleration in domestic refined output could moderate import growth, but imported zinc ingots will remain a key balancing supply source in the near term.

Leave a Reply