- Secondary zinc market pressured by softer LME prices, cautious demand

- Consumers continue to purchase only to meet immediate requirements

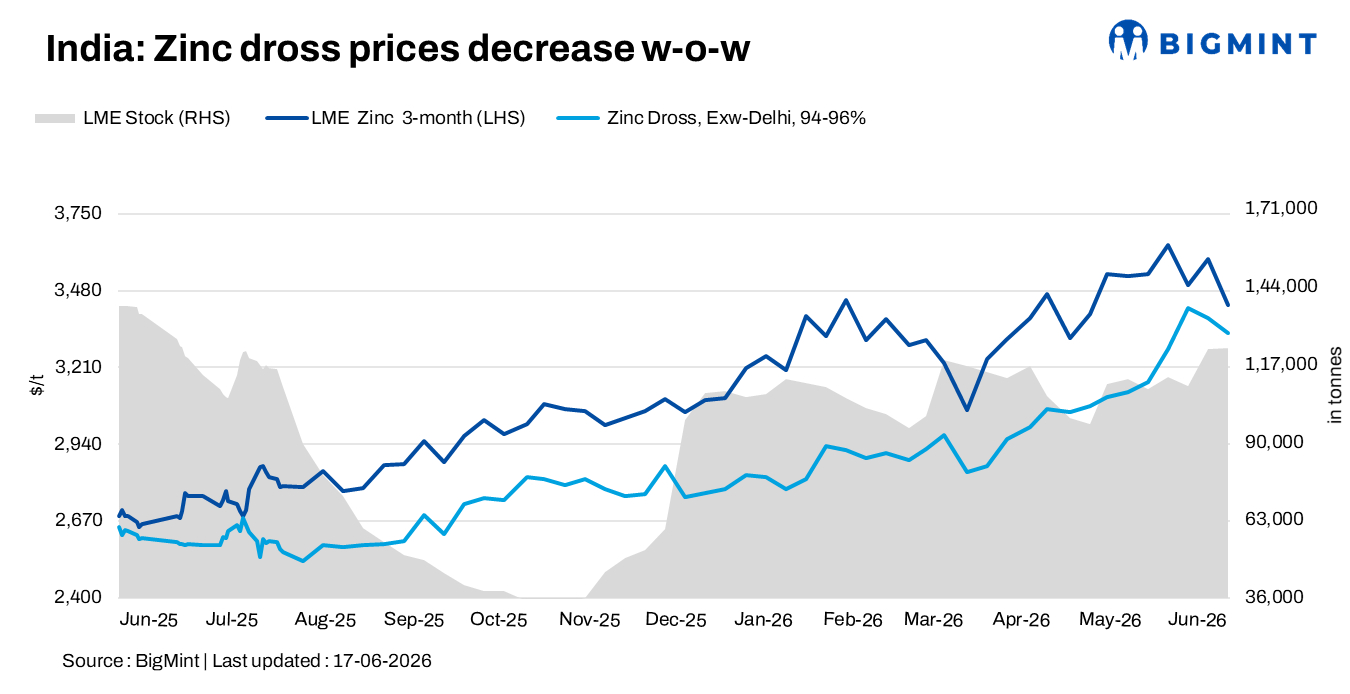

India’s zinc dross and zinc oxide prices declined w-o-w as of 24 June 2026, as softer London Metal Exchange (LME) zinc prices and cautious downstream procurement weighed on the domestic secondary zinc market. Buyers continued to resist higher offers and largely restricted purchases to immediate production requirements amid uncertain demand visibility.

Benchmark three-month LME zinc prices averaged around $3,553/t during the week ended 24 June, compared with approximately $3,558/t a week earlier. Meanwhile, LME zinc inventories increased marginally to 122,825 t on 24 June from 122,375 t recorded on 17 June, indicating broadly stable exchange warehouse stocks.

The decline in international zinc prices, coupled with a recent reduction in Hindustan Zinc Ltd’s benchmark zinc prices, added pressure to domestic market sentiment. Market participants reported that most transactions continued to be concluded against confirmed orders, with limited appetite for inventory accumulation.

Zinc dross, oxide price movements

Domestic zinc dross prices declined by around INR 4,800/t w-o-w to INR 313,200/t ex-Delhi from INR 318,000/t a week earlier.

Meanwhile, zinc oxide (99% Zn) prices fell by around INR 1,800/t w-o-w to INR 304,200/t ex-Delhi, compared with INR 306,000/t in the previous week. Market participants reported stable demand from the rubber and chemical sectors, although procurement activity remained largely need-based.

The correction in secondary zinc prices reflected softer replacement costs and subdued buying activity rather than any significant deterioration in underlying consumption fundamentals.

Scrap segment trends

In the north Indian zinc scrap market, regular-grade Tukdi prices were heard at around INR 300,000-301,000/t ex-Delhi, down from INR 302,000-303,000/t a week earlier. Small-sized Tukdi was assessed at INR 298,000-299,000/t compared with INR 299,000-300,000/t in the previous week.

Scrap prices softened modestly during the assessment period in line with the broader decline in secondary zinc products. Market participants reported adequate material availability, while consumers continued to maintain lean inventories and procure material primarily against confirmed requirements.

Market sentiments

Market participants reported a cautious tone across the secondary zinc market during the week. The decline in LME zinc prices reduced replacement costs and encouraged buyers to delay purchases in anticipation of further corrections.

Although end-user demand from key consuming sectors remained broadly stable, buyers showed limited urgency to secure additional volumes. Processors also faced increasing resistance while attempting to maintain previous offer levels, resulting in lower transaction prices across several product categories.

Trading activity remained moderate, with most deals concluded on a back-to-back basis rather than for stock-building purposes. Market participants continued to closely monitor international zinc price movements and domestic demand trends for clearer market direction.

Outlook

In the near term, zinc dross and zinc oxide prices are expected to remain range-bound to slightly weaker, influenced by softer replacement costs and cautious downstream procurement. While stable demand from the rubber and chemical sectors may prevent a sharp decline, limited inventory-building activity and buyer resistance to higher offers are likely to cap any meaningful upside.

Market participants are expected to closely monitor LME zinc price trends, inventory developments and downstream consumption patterns for further cues in the coming weeks.

Leave a Reply