- Secondary zinc market pressured by weak downstream procurement

- Buyers remain focused on immediate requirements as market seeks direction

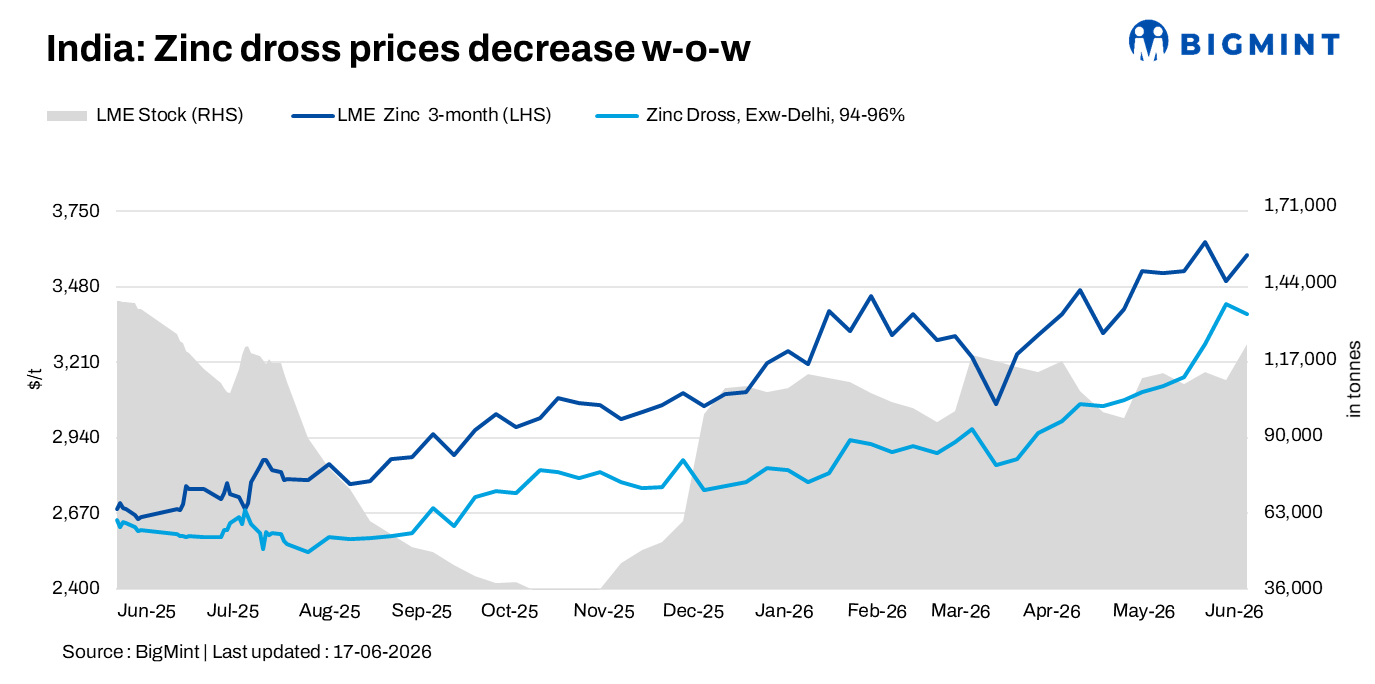

India’s zinc dross and zinc oxide prices declined w-o-w as of 17 June 2026, as cautious buying activity and resistance to higher offers weighed on the domestic secondary zinc market. The correction came despite broadly firm London Metal Exchange (LME) zinc prices during the assessment period, reflecting subdued downstream procurement and limited appetite for inventory accumulation.

Benchmark three-month LME zinc prices averaged around $3,558/t during the week ended 17 June, compared with approximately $3,548/t a week earlier. Meanwhile, LME zinc inventories increased to 122,375 t on 17 June from 109,575 t recorded on 10 June, indicating a notable rise in exchange warehouse stocks.

While international zinc prices remained relatively supportive, domestic buyers largely refrained from aggressive purchasing activity. Market participants reported that most transactions were concluded against confirmed orders, with consumers remaining cautious amid recent price volatility and uncertain demand visibility.

Zinc dross, oxide price movements

Domestic zinc dross prices declined by around INR 3,400/t w-o-w to approximately INR 318,000/t ex-Delhi. In western India, zinc dross prices were heard at around INR 316,000/t ex-Mumbai, down from INR 318,000-319,000/t a week earlier.

Meanwhile, zinc oxide (99% Zn) prices fell by around INR 2,000/t w-o-w to INR 306,000/t ex-Delhi. Market participants reported moderate demand from the rubber and chemical sectors, although buying interest remained largely need-based.

The correction in secondary zinc values reflected softer procurement activity rather than any significant deterioration in underlying market fundamentals.

Scrap segment trends

In the north Indian zinc scrap market, large-sized Tukdi (97% Zn) prices were heard at around INR 306,000-307,000/t ex-Delhi. Regular-grade Tukdi was assessed at INR 302,000-303,000/t, while small-sized Tukdi was heard at INR 299,000-300,000/t.

Scrap prices remained relatively stable during the week despite softer dross and oxide values. Market participants indicated that availability of quality scrap remained adequate, preventing any sharp movement in procurement prices. Most consumers continued to maintain lean inventories and purchased material primarily to meet immediate production requirements.

Market sentiments

Market participants reported a cautious tone across the secondary zinc market during the week. Although LME zinc prices remained broadly supportive, downstream consumers showed limited willingness to accept higher offers following the recent rally in domestic prices.

Several buyers preferred to delay larger purchases and monitor the direction of international zinc markets before committing to additional volumes. At the same time, processors faced increasing resistance when attempting to pass through elevated replacement costs, resulting in a gradual correction in finished secondary zinc prices.

Trading activity remained moderate, with most deals concluded on a back-to-back basis rather than for stock building. Market participants noted that end-user demand from key consuming sectors remained stable but lacked the momentum needed to support further price increases.

Outlook

In the near term, zinc dross and zinc oxide prices are expected to remain range-bound, supported by relatively firm LME zinc prices and stable downstream consumption. However, cautious procurement behaviour and the absence of aggressive buying interest may continue to limit upward price momentum.

Market participants are expected to closely monitor LME price movements, inventory trends, and demand from the rubber and chemical sectors for clearer market direction in the coming weeks.

Leave a Reply