- Festive season, extended monsoon impact trade

- Elevated inventories at mills drag down prices

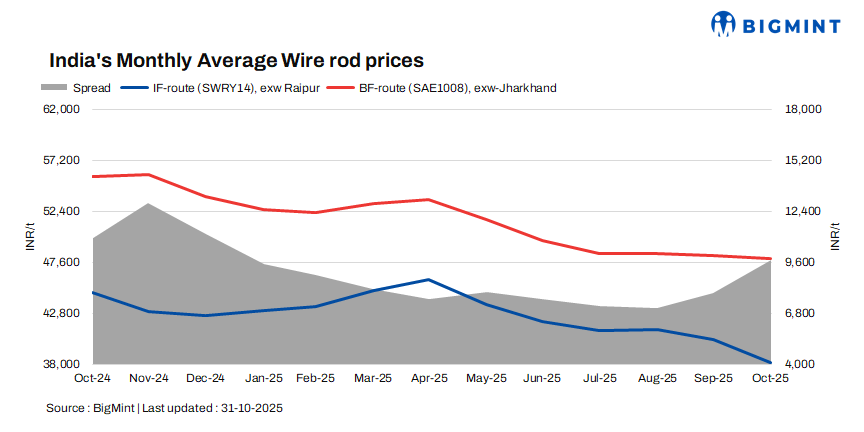

Indian wire rod prices neared five-year lows in October 2025 amid sluggish buying inquiries.

In the induction furnace (IF)-route segment, wire rod prices witnessed a monthly average decrease of INR 1,300/tonne (t) ($15/t) m-o-m to INR 37,900/t ($427/t) exw-Durgapur and fell by INR 2,100/t ($24/t) m-o-m to INR 38,200/t ($430/t) exw-Raipur as compared to September 2025 levels. Both were at their lowest since around November 2020.

The spot trade reference prices stood at INR 38,500/t ($434/t) exw-Raipur and INR 37,400/t ($421/t) exw-Durgapur as on 3 November 2025.

In the BF segment, wire rod prices (5.5-6mm, SAE1008) edged lower m-o-m by INR 300/t ($3/t) to a monthly average of INR 47,900/t ($540/t) exw-Jharkhand in October 2025. Prices touched their lowest levels in four-and-a-half years in October 2025.

Wire rod prices (5.5-6mm, SAE1008) were assessed at INR 47,800/t ($538/t) exw-Jharkhand as per BigMint’s weekly assessment on 31 October 2025.

Cumulative wire rod production via the IF and BF routes in January-September 2025 stood at 6 mnt, up 9% from 5.5 mnt in the same period in 2024, as per the JPC report. Notably, for IF-route wire rods, Raipur (central region) and Durgapur (eastern region) are the major supply centres catering to various other markets across the country.

Factors behind market dynamics

Billet prices hit nearly 5-year low: The Indian sponge iron and billet market witnessed bearish trends in October 2025. Weak demand was observed, as buyers largely adopted a wait-and-watch approach, concerned about inconsistent finished steel demand.

Considering the Raipur market as a benchmark, billet prices decreased by INR 1,600/t ($18/t) m-o-m to a five-year low of INR 35,200/t ($396/t) exw. Sponge iron (PDRI FeM 80% +/- 1) fell by INR 1,200/t ($14/t) m-o-m to INR 22,920/t ($258/t) exw (prices are on a monthly average basis).

Demand slows amid market uncertainties: Buying inquiries remained dull in the Raipur and Durgapur markets in October 2025. End‑users such as binding‑wire and GI‑wire manufacturers largely steered clear of bulk procurement, citing uncertainty in market direction. Additionally, the festive season, liquidity constraints, and lower landed costs of material from the eastern region added downward pressure on demand, prompting buyers to make need-based purchases. Meanwhile, suppliers offered attractive trade discounts to liquidate stocks, which remained elevated throughout the month.

Even wire rod manufacturers cut production by 20-30% (varying by location) in order to maintain demand- supply balance and avoid stock build‑up.

Primary mills see weak demand: In the BF segment, demand remained subdued, weighed down by the festive season slowdown and restrained offtake by downstream sectors.

Construction activity was impacted by the monsoon rains, while infrastructure projects saw slower execution. The automotive and engineering industries also displayed cautious buying amid inventory adjustments. Overall, market sentiment remained weak, with limited trading activity and expectations of demand recovery only after mid-November, once construction and industrial operations normalise.

Outlook

Wire rod prices are likely to rise further in November 2025, amid favourable conditions in the infrastructure and construction sectors, which could support domestic demand.

Leave a Reply