- Lower fixture levels and excess tonnage pressure Panamax market

- Weak cargo demand drags Indonesia-India rates to over a one-month low

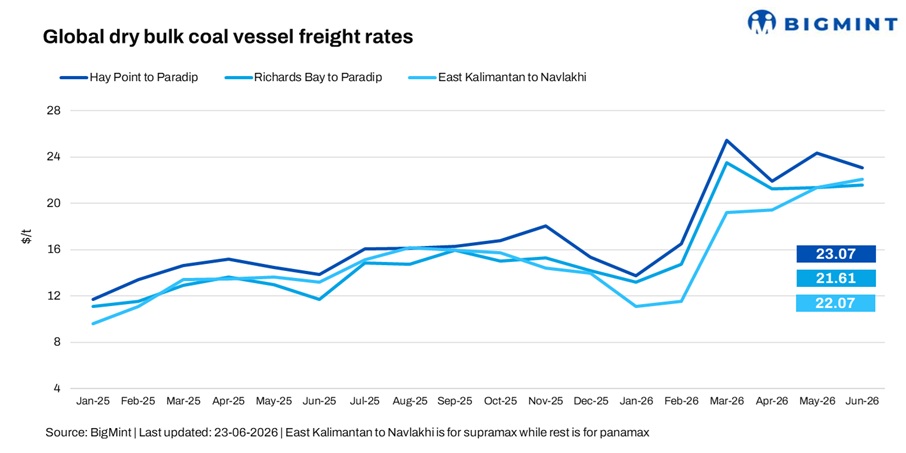

India’s dry bulk coal freight market softened in the week ended 23 June 2026, with freight rates easing across key Panamax and Supramax routes as lower fixture levels, subdued cargo demand and comfortable vessel availability weighed on market sentiment. While the Atlantic remained comparatively balanced, weaker Pacific fundamentals continued to limit freight momentum.

The Panamax market remained under pressure as owners competed for limited cargoes amid ample prompt tonnage, with several fixtures concluded at lower levels. Weak imported coal demand and cautious Indonesian regulatory sentiment slowed fresh fixing activity, pushing freight rates to over a one-month low. However, selective buying interest from India’s west coast offered some support to sentiment.

A shipbroker added, “The imported coal market remains weak. Indonesian traders continue to face regulatory challenges, while demand from India’s west coast is still present. However, trading activity is below normal levels.”

Another shipbroker said, “The Pacific remains oversupplied, with more vessels chasing fewer cargoes. Owners are becoming increasingly competitive to secure prompt employment.”

Route-wise update

The Pacific market remained subdued as muted cargo enquiries and ample vessel availability limited fresh fixing activity across Australia and Indonesia. Meanwhile, the Atlantic remained comparatively balanced, although subdued enquiries and improving vessel availability capped further momentum.

The Supramax segment also softened as post-holiday trading across Asia remained muted. Weak cargo demand dragged regional activity, pushing freight rates to over a one-month low, while geopolitical uncertainty in the Middle East kept both owners and charterers cautious.

Outlook

Coal freight rates to India are expected to remain mixed in the near term. The Panamax market is likely to remain influenced by Pacific cargo availability and vessel supply, while the Supramax segment will depend on a recovery in regional cargo demand. Bunker price movements, developments in the Middle East and evolving regulatory changes in Indonesia will remain key factors shaping freight sentiment.

Leave a Reply