- Slowdown in steel market weighs on demand

- Margin pressure persists due to elevated raw material prices

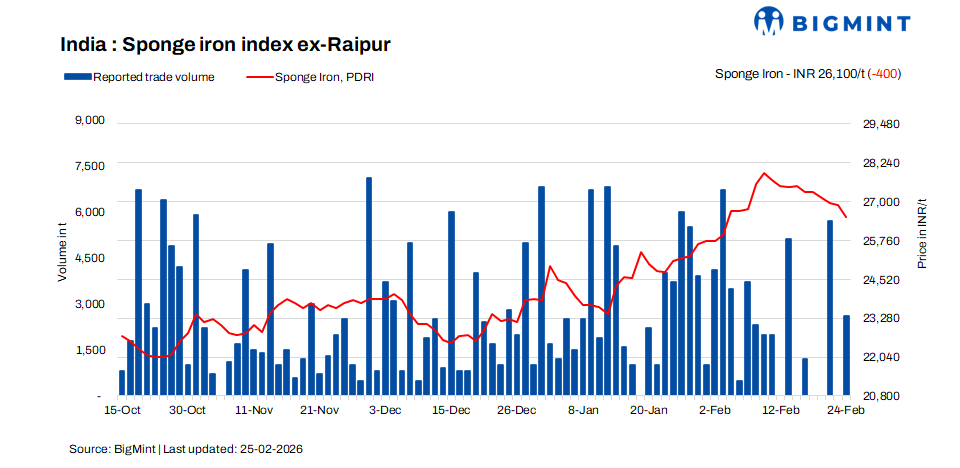

Indian sponge iron prices extended their downward trend on 25 February 2026, with prices declining by INR 50-500/t d-o-d across major regions, as weak finished steel demand continued to dampen sentiment. Subdued downstream offtake weighed on procurement activity, resulting in thin trading. Buyers restricted purchases to immediate requirements, anticipating further corrections amid persistent weakness in rebar and wire rod demand.

Although raw material prices remained elevated, exerting pressure on producer margins, sellers were compelled to trim spot offers in an attempt to stimulate bookings. However, the price reductions failed to significantly improve liquidity, as cautious sentiment and expectations of additional downside kept buyers defensive.

Market participants reported limited enquiries and an absence of bulk transactions, reflecting broader lack of confidence in the steel value chain. A Raipur-based induction furnace operator said, “Even with lower sponge iron prices, finished steel movement remains slow, limiting raw material consumption.”

Producers, despite facing higher input costs, adjusted prices downward to align with prevailing bids. The imbalance between firm raw material costs and weak finished steel demand continued to suppress trade momentum, keeping overall market activity subdued.

Rationale

Prices have been derived based on transactions, offers, bids, and indicative price data sets. Transactions are considered as T1 and given a weightage of 50%, whereas other data sets are considered as T2 and given a weightage of the balance 50%.

Click here for detailed methodology

Leave a Reply