- Petcoke switching momentum loses steam, buyers have ample stocks

- Cement buyers adopt cautious stance amid approaching monsoon

US Northern Appalachian (NAPP) coal prices in India are facing renewed pressure as petcoke prices correct sharply and cement-sector demand turns cautious ahead of the monsoon season.

NAPP coal had gained traction among Indian cement producers earlier this year after petcoke prices rose sharply, making high-CV US coal a more attractive substitute. However, the fuel economics have started shifting again. With CFR India high-sulphur petcoke prices easing to nearly $133/t, the earlier advantage enjoyed by NAPP coal has narrowed significantly.

Petcoke regains competitiveness

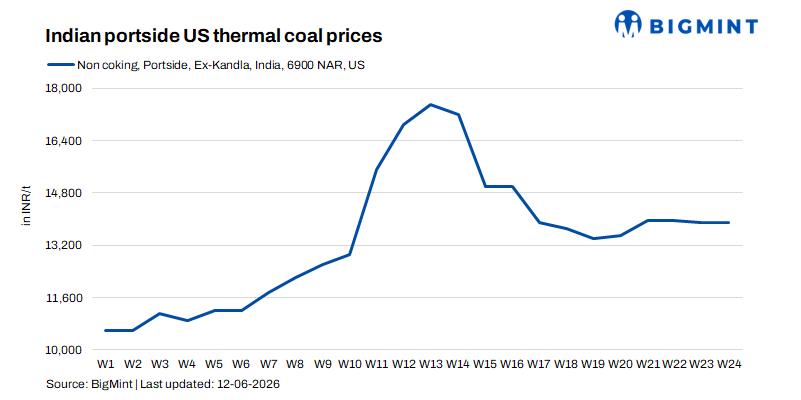

Fuel switching in the Indian cement sector remains largely price-driven. NAPP coal, with an energy value of around 6,900 kcal/kg NAR, had become attractive when petcoke prices were elevated. Cement makers increased NAPP consumption as petcoke became expensive and less readily available.

That trend is now reversing. Petcoke prices have dropped sharply from May levels, while NAPP coal offers are still heard in the low-to-mid $130s/t CFR west coast India. As a result, petcoke has again become competitive on an energy-adjusted basis.

This has prompted several cement buyers to slow fresh coal purchases and reassess their fuel mix. Buyers are not short of material and are showing little urgency to take fresh positions, especially with construction activity expected to soften during the monsoon.

Portside NAPP market turns cautious

The retail NAPP coal market at Kandla and Tuna has also softened. Ex-wharf indications are largely in the range of INR 13,500-14,000/t, but buying interest remains limited.

Retail stock across Kandla and Tuna stood at 349,244 t as of 8 June 2026. Kandla accounted for 159,704 t, while Tuna held 189,540 t. Although inventories have drawn down from 587,805 t in mid-May, availability remains comfortable.

Weekly lifting has also slowed. Retail lifting fell to 95,640 t in Week-23 from 99,486 t in Week-22 and 122,876 t in Week-21. The fall suggests that demand is being met from existing inventories rather than through aggressive fresh restocking.

Outlook

The near-term outlook for US NAPP coal in India is weak to stable. Prices are likely to remain capped by three factors: falling petcoke prices, comfortable NAPP stocks at ports, and slower seasonal cement demand.

Unless petcoke prices rebound or freight-led supply disruptions emerge, cement makers are likely to keep purchases limited and flexible. NAPP coal may continue to find demand from buyers seeking high-CV fuel diversification, but the strong switching momentum seen earlier has clearly moderated.

Leave a Reply