- US-India freights remain elevated, keeping delivered costs high

- Industrial buyers resist high prices amid squeezed margins

India’s prices of US high-calorific-value Northern Appalachian (NAPP) coal remained elevated in both import and domestic spot markets, but the drivers of firmness differ sharply between the industrial and retail segments — creating a two-tier market.

The reason for this divergence is structural. Retail buyers — including traders, smaller industrial consumers, and secondary distributors — are currently absorbing a large share of available tonnage. As a result, some volumes that might otherwise move to large industrial users are being diverted into the retail channel.

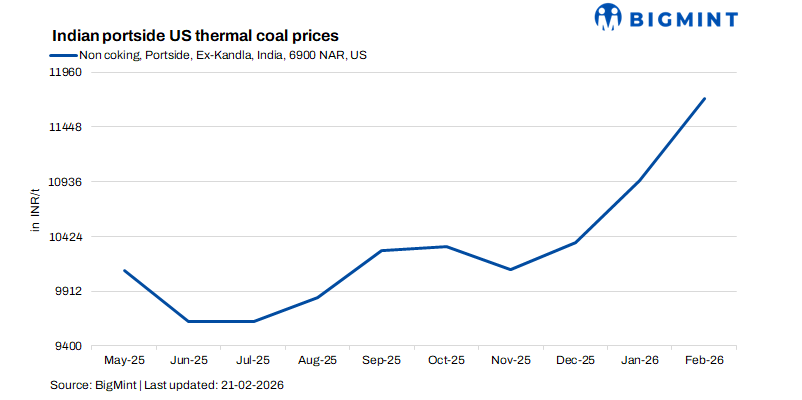

As per BigMint’s assessment, portside prices of US thermal coal in India were reported at INR 11,750/t ex-Kandla, marking a sharp w-o-w increase of INR 450/t.

Industrial buyers push back on high prices

In the industrial segment, especially among cement producers, the current price environment is being viewed as unsustainable.

Delivered offers for US NAPP coal into India are currently clustered around $125-127/t CFR, levels that many buyers consider uneconomic given stagnant cement prices and squeezed margins. Several producers indicate they are prioritising profitability over volume growth, with fuel costs rising faster than finished cement prices.

Some companies are drawing down existing long-term supply contracts rather than purchasing spot cargoes, while others are pivoting toward domestic coal or alternative imports such as Indonesian or Venezuelan fuels. The shift reflects a broader trend: industrial buyers are willing to substitute fuels when the coal-to-petcoke spread narrows.

This behaviour mirrors developments in the petcoke market, where elevated prices are already encouraging fuel switching. The same logic is now shaping procurement decisions in the NAPP coal segment.

Retail market drives domestic premiums

In contrast, India’s retail coal market remains firm, supported by steady lifting activity and tight prompt availability. Spot prices at Tuna have recently crossed INR 15,000/t, while Kandla remains lower due to quality verification delays and logistics constraints. Even after expected corrections, prices in the INR 13,500-14,000/t range still represent a premium to the levels most industrial consumers consider viable.

Strong supply pipeline could cap prices

Despite the current firmness, incoming cargo flows suggest that relief may be approaching.

Nearly 650,000 t of NAPP coal are scheduled to arrive between late February and early April, a pipeline that could significantly increase availability. Market participants note that once these cargoes discharge, prompt tightness should ease, and domestic premiums could soften.

There are already early signals of this adjustment. Some forward cargoes for March-April delivery have reportedly traded INR 1,000-1,500/t lower than recent spot peaks, indicating that traders expect supply to normalise.

Freight, global signals still support prices

Even so, global fundamentals continue to underpin US coal values. Freight from the US East Coast to India remains elevated at roughly $38/t, keeping delivered costs high and limiting downside in CFR pricing.

At origin, US export prices also remain supported by stable domestic market conditions and steady export flows.

Together, these factors suggest that while domestic premiums may ease, the floor for imported NAPP coal prices is unlikely to fall sharply in the near term.

The balancing act ahead

The Indian NAPP coal market is therefore moving into a classic balancing phase.

- Industrial buyers are resisting current prices and exploring substitutes.

- Retail markets remain firm due to prompt tightness.

- Incoming cargoes should gradually improve supply visibility.

- Freight and origin costs are keeping the import price floor elevated.

If supply arrivals proceed as scheduled, the next few weeks could see the domestic market shift from scarcity-driven pricing to inventory-driven competition.

But unless freights soften or US export prices weaken meaningfully, India’s high-CV coal prices are more likely to stabilise than collapse.

Leave a Reply