- Prices correct on strong arrivals while export slowdown intensifies

- Middle East tensions and Bangladesh-led demand shift reshape trade

Prices decline as peak arrivals trigger profit booking

Turmeric prices declined by 2.16% to settle at INR 15,800, as traders and stockists booked profits following the recent rally supported by tight early-season arrivals. The correction aligns with the peak arrival phase, with Agmark data indicating cumulative arrivals of 176,358 MT between February and mid-April, reflecting strong fresh crop inflows.

Arrivals surged sharply in March to 99,190 metric tonnes (t) compared to 31,205 t in February, confirming peak harvesting pressure. Although arrivals in April remain elevated at 45,963 t (till mid-month), the pace has started stabilising, suggesting that supply pressure may gradually ease in the coming weeks.

Concentrated supply keeps market sensitive to Telangana trends

Supply remains highly concentrated, with Telangana contributing 43% of total arrivals (76,250 t), followed by Andhra Pradesh (19%), Maharashtra (17%), and Karnataka (15%). This concentration keeps the market highly sensitive to supply trends from Telangana, where any slowdown could tighten spot availability and support prices.

Production estimates remain stable at around 11.41 lakh tonnes, as a 4% increase in acreage offsets localised yield losses of 15-20% caused by unseasonal rains and disease. Lower carry-forward stocks and continued farmer holding are restricting aggressive selling, maintaining a firm underlying tone. Dried turmeric output is estimated at around 90 lakh bags, higher than last season, although quality concerns persist.

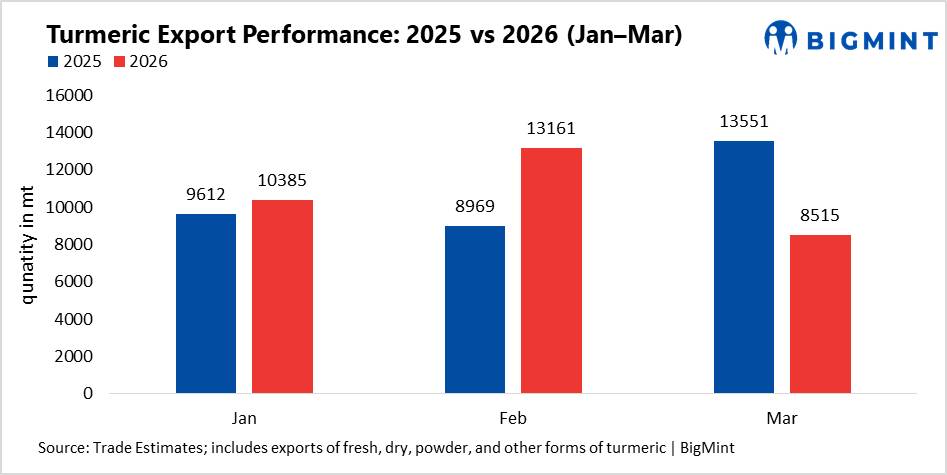

Export slowdown deepens amid geopolitical disruptions

Export demand weakened toward the end of the quarter. While shipments rose by 8% and 47% y-o-y in January and February, respectively, March exports declined sharply by 37% y-o-y to 8,515 t, resulting in flat quarterly exports of around 32,000 t.

The slowdown is also linked to geopolitical tensions in the Middle East, particularly the Iran-Israel conflict, which has disrupted trade flows, increased freight uncertainty, and delayed shipments to key Gulf markets. This has reduced buying interest from traditional destinations such as the UAE.

At the same time, export patterns are shifting. JNPT’s share declined from 58% to 45%, while Ghojadanga LCS accounted for 14%, reflecting a rise in land-route trade. Bangladesh emerged as the largest importer with a 15% share, indicating a shift toward nearby markets amid weaker global demand.

Outlook

Market positioning remains cautious, with open interest rising by 8.25%, indicating fresh selling pressure.

Going forward, the pace of decline in arrivals and recovery in export demand will be key. While peak arrivals continue to pressure prices, tight stocks, farmer holding, and shifting export dynamics are likely to limit downside, keeping the market range-bound with a cautious firm undertone.

Leave a Reply