- Buyers explore domestic options amid falling imports

- India’s HRC offers to Europe increase by $20/t w-o-w

Trade-level hot-rolled coil (HRC) offers surged by up to INR 1,000/tonne (t) ($11/t) w-o-w to INR 50,200-52,500/t ($586-613/t) across domestic markets. Cold-rolled coil (CRC) prices increased by up to INR 1,300/t ($15/t) w-o-w to INR 56,000-59,000/t ($654-689/t). Notably, material shortages and expanding export opportunities drove up prices this week.

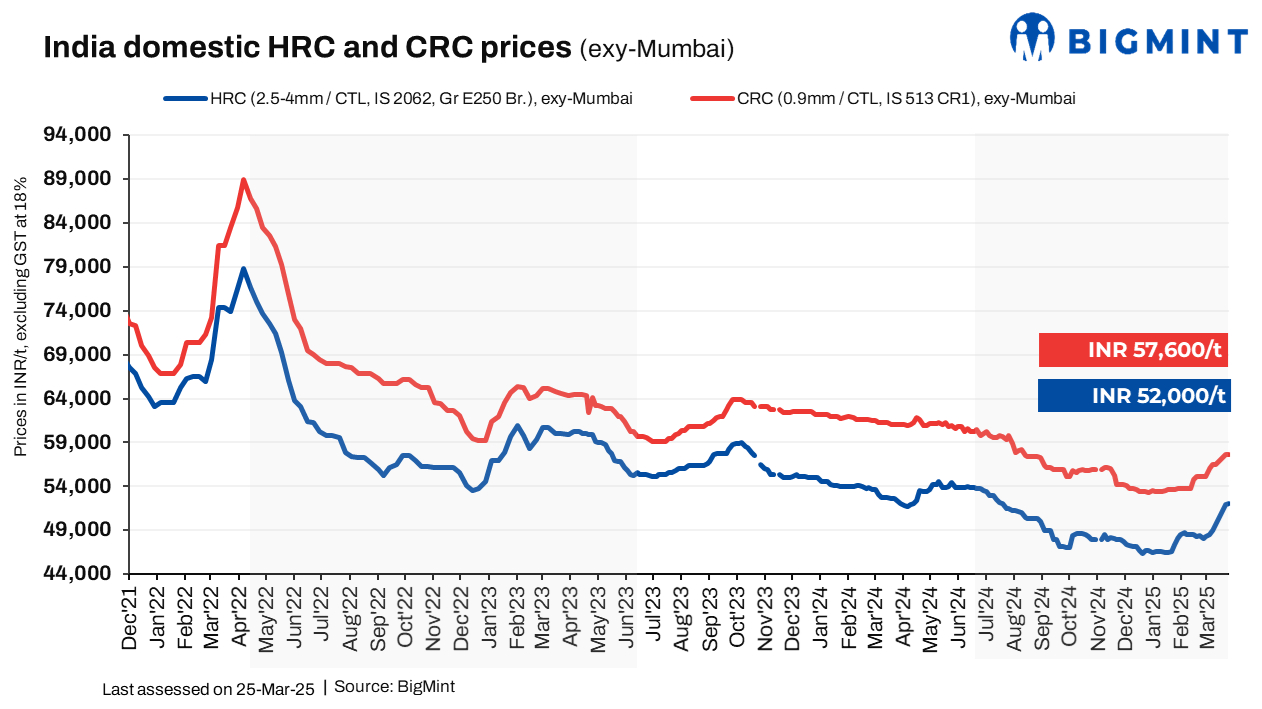

BigMint’s benchmark assessment (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) increased by INR 500/t ($6/t) w-o-w to INR 52,000/t ($607/t)on 21 March. However, CRC (IS513, Gr O, 0.9 mm/CTL) prices remained stable w-o-w at INR 57,600/t ($673t). These prices are quoted ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Market updates

Market witnesses supply shortages: Material shortages emerged this week, which led suppliers to continue lifting their HRC offers. However, although tags increased, the pace of growth slowed, as buyers resisted higher offers due to the impact on their raw material costs. Moreover, with imports starting to decline, buyers actively explored domestic options.

A market participant noted, “The market has slowed, with demand declining, but material shortages are emerging. Some businesses are reducing their inventory levels to optimise their holdings.”

Import trends: India’s bulk imports of HRCs and plates touched 319,404 t as of 24 March, based on vessel line-up data from BigMint. Another 26,977 t are expected by the end of this month, and an additional 35,817 t are set to arrive in the first week of next month.

Export trends: India’s steel industry witnessed a notable rise in export activity, with HRC (SAE 1006) offers to Europe increasing by $20/t w-o-w, driven by stronger domestic prices in the region. However, Indian mills adopted a cautious approach towards exports to the Middle East and Vietnam, as market activity slowed ahead of the Eid holidays in the Middle East and domestic demand was weak in Vietnam.

Outlook

In the near term, HRC and CRC prices may remain firm amid supply shortages and cautious buying. Declining imports could further tighten domestic supply, supporting prices. However, resistance from buyers due to higher costs may limit gains.

Leave a Reply