The trade market price levels have continued to stay range-bound amid the availability of cheaper alternatives and the need-based buying pattern of the end-industrial buyers. Sellers in the traders’ market segment are cautious and trying to maintain offer levels to evade further losses with the fiscal year end around the corner.

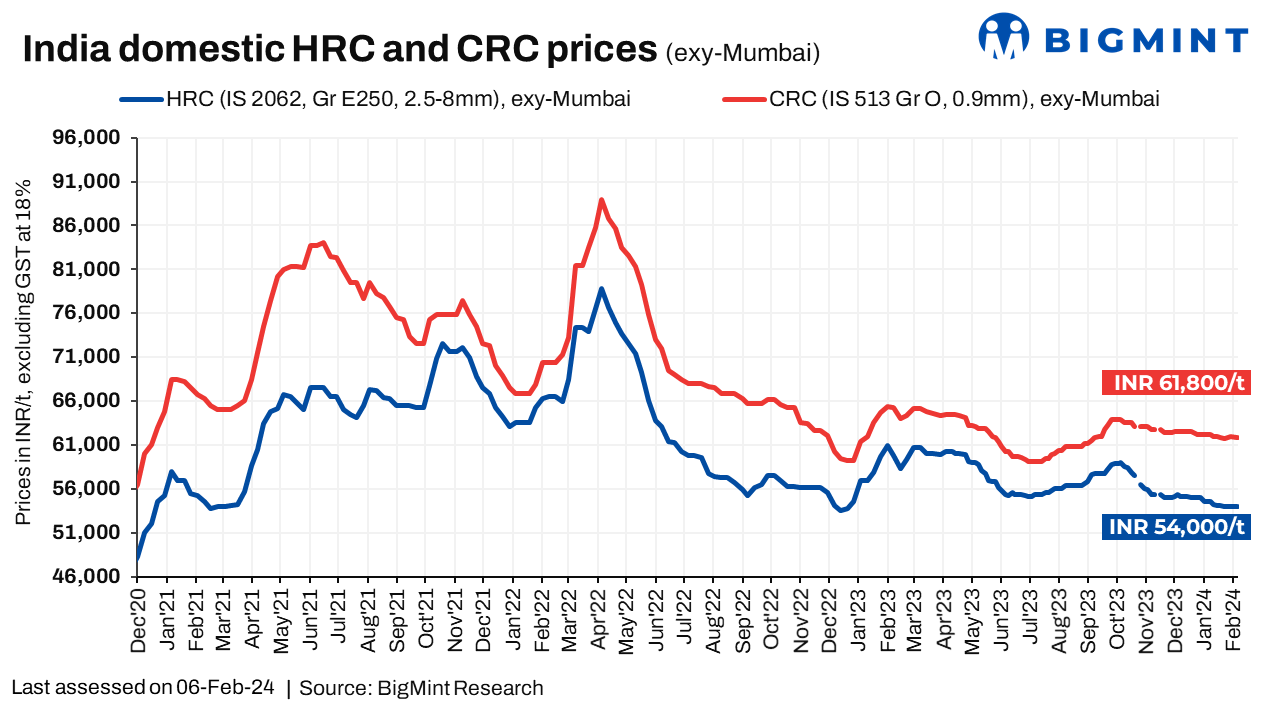

BigMint’s benchmark assessment for HRC (IS2062, 2.5-8mm) hovered around INR 53,500-54,500/t ($644-656/t) exy-Mumbai as on 6 February 2024. Concurrently, CRC (IS513, Gr-O, 0.9mm) prices stayed unchanged at INR 61,500-62,500/t ($740-752/t) exy-Mumbai. The prices mentioned above are for cut-to-length (CTL) forms, excluding GST at 18%. (INR 1 = USD 0.0120378 ; USD 1 = INR 83.0714)

On top of the initial announcement by SAIL for flat steel prices, there has been another announcement about an additional INR 500/t ($6/t) increase in HRCs for February 2024 sales. Subsequent to the announcement, the company’s price tag increased to INR 55,500-56,000/t ($668-674/t) landed. Whereas, for CRC the mill’s prices were further increased by INR 1,000/t ($12/t) to hover around 60,500-61,000/t ($728-734/t) landed. As per industry sources, the mill has announced a rebate of INR 2,000/t ($24/) for HRC and Plates while INR 2,500-3,000/t ($30-36/t) for CRC.

Meanwhile, updated price tags of private mills for February 2024 stand around INR 57,500-58,500/t ($692-704/t) landed for HRC and CRC around INR 63,000-63,750/t ($758-767/t) landed. The rebates offered by private mills are being heard at around INR 2,000-2,500/t ($24-30/t) for January 2024. The prices mentioned are effective from 1 February 2024, for coil forms and excludes GST at 18%.

Increased price levels of raw material that are to be consumed for production now, along side price increase announcements by mills on the global platform are among the primary reasons behind mills taking this hike. It can be recalled that the Chinese, Vietnamese and European mills have increased their offer price tags in their respective territories in the past couple of weeks.

Market updates:

1. Domestic trade-level prices remained stable: Trade market sentiments have remained subdued despite mills increasing list prices for February 2024. In majority of markets need-based buying persists although some regions have started to show increase in the inquiries. Liquidity concerns and price favourability continue to weigh on market activities, hinted some industry sources.

“Price hikes by mills had minimal impact on the market, which is likely to remain stable in the near term. Liquidity constraints are prevalent; hence some players are trying to liquidate inventory at discounted prices,” said a market participant.

2. Indian HRC export prices remain range-bound: BigMint’s India HRC (SAE 1006) export index (for the Middle East and Vietnam) remained range-bound w-o-w at $599/t FOB against $600/t FOB east coast India.

Indian HRC exports to the Middle East (ME) stood un-wavered w-o-w at $630-635/t CFR. A prominent Indian steel player closed a 30,000 t HRC deal at $630/t CFR for March shipments. Meanwhile, Chinese prices to the ME dipped to $605-610/t CFR UAE.

In Vietnam, Indian HRC price indications hold steady w-o-w at $610-615/t CFR Ho Chi Minh City, although trade activities remain sluggish. Chinese HRC offers to Vietnam decrease w-o-w to $595-600/t CFR.

In Europe, Indian HRC exports dip marginally w-o-w to $715-720/t CFR Antwerp, impacted by a 1.9% Euro depreciation against the dollar. Domestic HRC prices remain high, deterring buyers amid elevated inventories and weak demand.

3. Imports rise in January 2024: India’s imports of bulk hot-rolled coil (HRC) and plates saw a notable increase in January 2024, according to provisional vessel line-up data tracked by BigMint. Total import volumes reached 6,60,344 tonnes, marking a significant rise from 5,29,661 tonnes in December 2023.

As of 5 February, 2024, provisional data suggests sustained import activity, with volumes already reaching 61,300 tonnes.

Outlook:

Market prices for Hot-Rolled Coils (HRC) and Cold-Rolled Coils (CRC) by traders are expected to hover around in a similar range in the coming weeks, influenced by the availability of more affordable domestic and imported alternatives. Whereas mills are banking upon increasing export businesses considering absence of Chinese competitors on the global platform because of the Lunar New Year holidays.