Hot-rolled coil (HRC) prices remained stable, establishing a range between INR 52,900-56,600/t ($635-679/t). Also, cold-rolled (CR) coil prices exhibited a degree of stability, maintaining a range of INR 58,300-63,500/t ($699-762/t) across various markets. The current state of the trade market reflects persistent sluggishness in trading activity, as sales have dropped significantly.

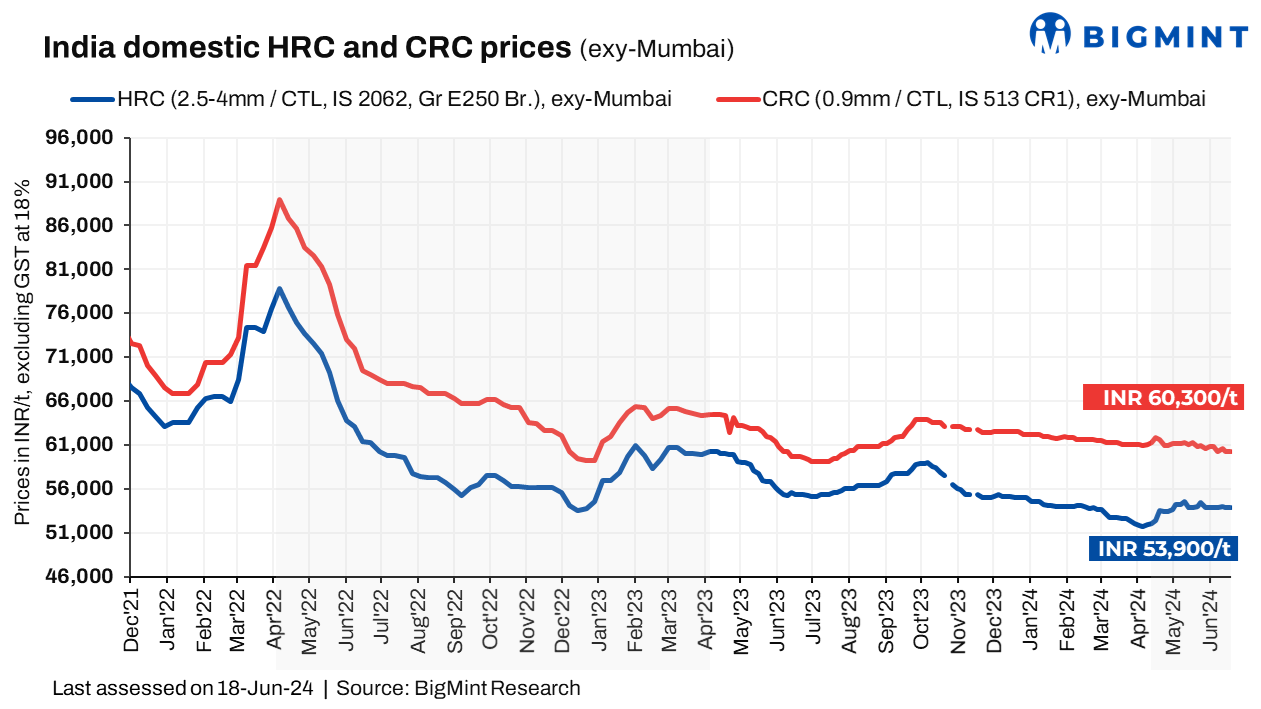

BigMint’s benchmark assessment (bi-weekly) for HRC (2.5-8mm, IS2062, Gr E-250 Br.) prices remained stable at INR 53,900/t ($647/t) on 11 June 2024, compared to the previous week. Also, CRC (0.90mm, IS 513, CR1) prices remained stable at INR 60,300/t ($723/t) during the same period. These prices are quoted ex-Mumbai, excluding 18% GST, and are for cut-to-length (CTL) deliveries. (INR 1 = USD 0.0119948 ; USD 1 = INR 83.3739)

Market updates

1. HRC market experiences sluggishness, CRC faces supply constraints: The HRC market is currently exhibiting persistent sluggishness, with a notable decline in sales volume. This softness in demand has put downward pressure on prices, as buyers are increasingly seeking negotiations below listed rates.

“Market demand has weakened, and material can only be sold at the lower end of the price range,” commented a market participant. “With margins under pressure and declining sales, the market faces additional challenges from rising imports and a global trend of falling prices. Any mill price increase could further aggravate these pressures and a potential influx of imports,” the participant added.

2. Export, import trends: India’s imports of bulk HRC and plates have begun to grow out pacing the exports as per the recent data from the vessel line-up data maintained with BigMint.

Indian exports of HRC to Southeast Asia and the Middle East (ME) remained subdued over the past week, influenced by sluggish global market sentiments compounded by Eid holidays. Chinese competitive pricing continued to dominate, with reports of deals concluded from China to the ME just ahead of the holiday period.

Meanwhile, Indian steel mills maintained their HRC export offers (S275, 3mm) to Europe unchanged this week, focusing on the domestic market as a priority. In contrast, European HRC prices experienced a marginal uptick despite lacklustre demand. This increase coincides with the European Union’s extended safeguard measures, aimed at restricting imports from specific countries and potentially tightening supply within Europe.

Outlook

The onset of the monsoon season is anticipated to reduce demand across various regions of India. This, alongside narrowing profit margins and reduced sales within the trading sector, is fostering a pessimistic market sentiment. Moreover, the increasing influx of imports is poised to exert additional downward pressure on prices. Consequently, the market is expected to remain within a stable range in the near term.