- HRC prices range-bound across regions

- Buyers cautious despite strong PMI

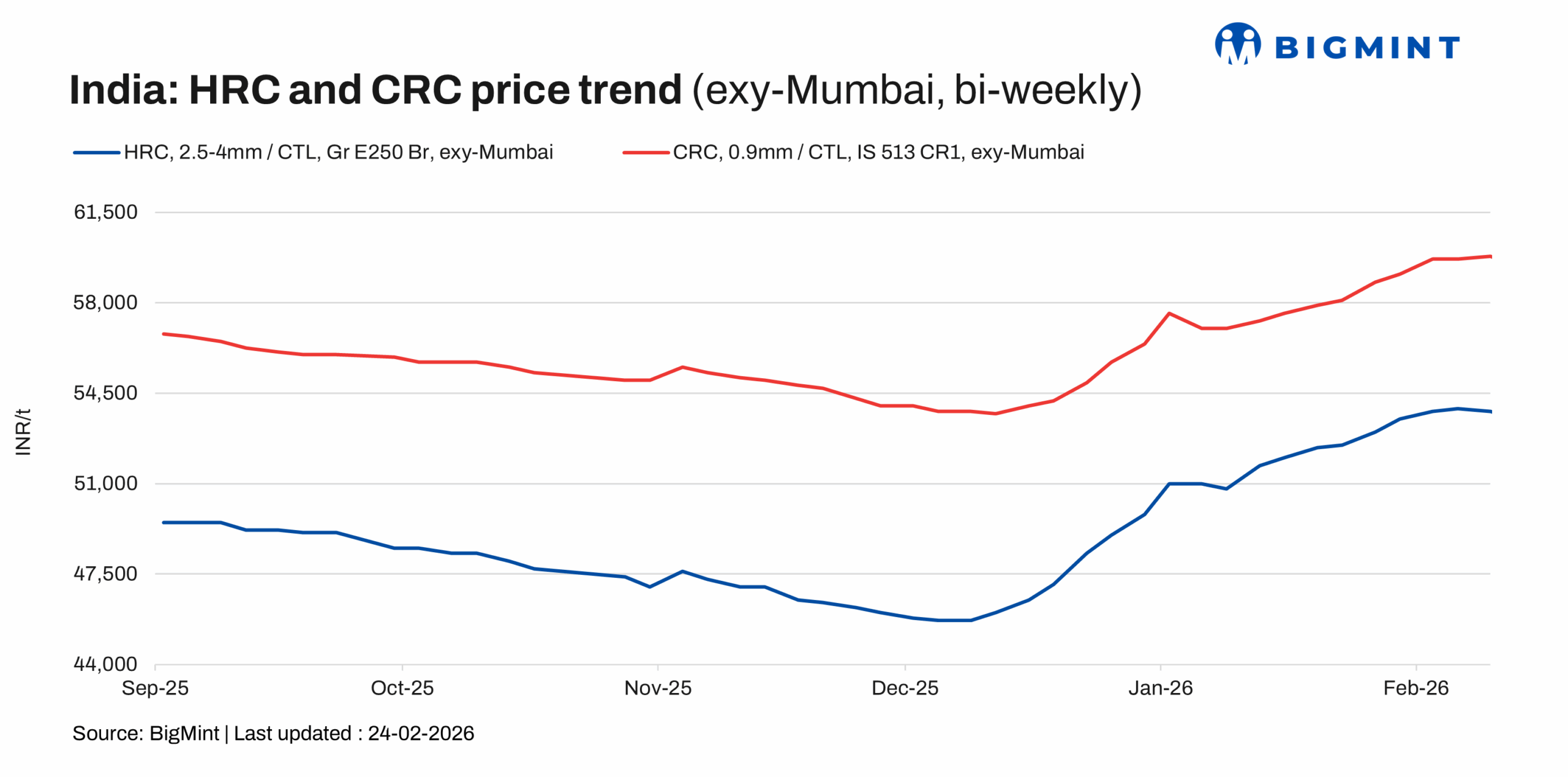

The trade-level prices of hot-rolled coils (HRC) in India remained muted across key regions amid soft sentiments and slow trading activity during the week ending 24 February with HRC prices assessed in the range of INR 52,200-54,500/t ($574-600/t) and cold-rolled coil (CRC) prices assessed at INR 56,200-61,700/t ($618-679/t).

BigMint’s benchmark assessment (bi-weekly) for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) observed slight uptick of INR 100/t ($1/t) w-o-w at INR 53,700/t ($591/t) on 24 February against INR 53,600/t ($590/t) in the same period last week.

CRC (IS513, Gr O, 0.9 mm/CTL) prices held at the same levels w-o-w at around INR 59,500/t ($655/t) on Tuesday. These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

India manufacturing PMI hits four-month high in february

The HSBC India Manufacturing PMI (Purchasing Managers Index) rose to 57.5 in February 2026, registering a four-month high and signalling a strong expansion in manufacturing activity. The uptick was primarily supported by resilient domestic demand, which led to higher new order inflows and a corresponding acceleration in production levels.

Market updates

North

Market sentiment in the northern region has softened amid declining price trends. Participants informed BigMint that “buyers have adopted a cautious stance due to the ongoing correction in prices”. Meanwhile, sellers are actively liquidating inventories, offering competitive discounts to secure sales and realise margins wherever possible. Inventory levels across the market remain adequate, further limiting immediate restocking interest.

East

In the eastern region, market participants informed Bigmint, “supply remained at moderate levels, while demand slowed, keeping prices stable over the past two weeks”. Buyers are largely procuring material on a need-based basis and are closely monitoring the market for the next price movement before committing to bulk purchases.

West

The HRC market in Western India is currently navigating a period of stagnant demand, with trade activity slowing down significantly as the month draws to a close. Market participants are showing signs of caution, remaining skeptical about the upcoming price revisions for March from major mills. A Mumbai-based trader noted that “market sentiment is very dull,” highlighting a general reluctance among buyers to commit to new volumes. This cautious stance has led to a wait-and-watch environment in the region.

South

Demand for HRC and CRC in the southern region remained weak. However, availability of thinner gauges continued to be constrained, particularly in CRC, which supported a w-o-w increase of INR 200/t. Inventory levels were assessed at moderate levels, although market participants reported shortages in select specifications. In the near term, some participants expect HRC and CRC prices to edge up by around INR 1,500-2,000/t, subject to mill pricing decisions and material availability. A BigMint source noted that “The price acceptance may remain mixed if mills announce hikes, with market chatter around the use of credit notes to support transactions.”

Import volumes: India’s bulk imports of HRCs touched 205,760 t as of 20 February, based on vessel line-up data. Around 1,21,762 t of additional cargoes are expected by mid-March.

Export volumes: India’s bulk exports of HRCs touched 102,250 t as of 20 February. Around 9,400 t of additional cargoes are in transit.

Outlook

In the upcoming week, prices are likely to undergo a mild correction due to the approaching Holi festival and persistently weak demand conditions. Market participants continue to maintain a wait-and-watch stance, reflecting cautious buying interest. Nevertheless, overall sentiment may remain guardedly steady, supported by expectations of potential price hikes from mills in the first week of March, which could set the tone for near-term market trends.

Leave a Reply