- BigMint HRC benchmark dips INR 200/t w-o-w to INR 53,600/t

- North sentiment weakens on delayed hike

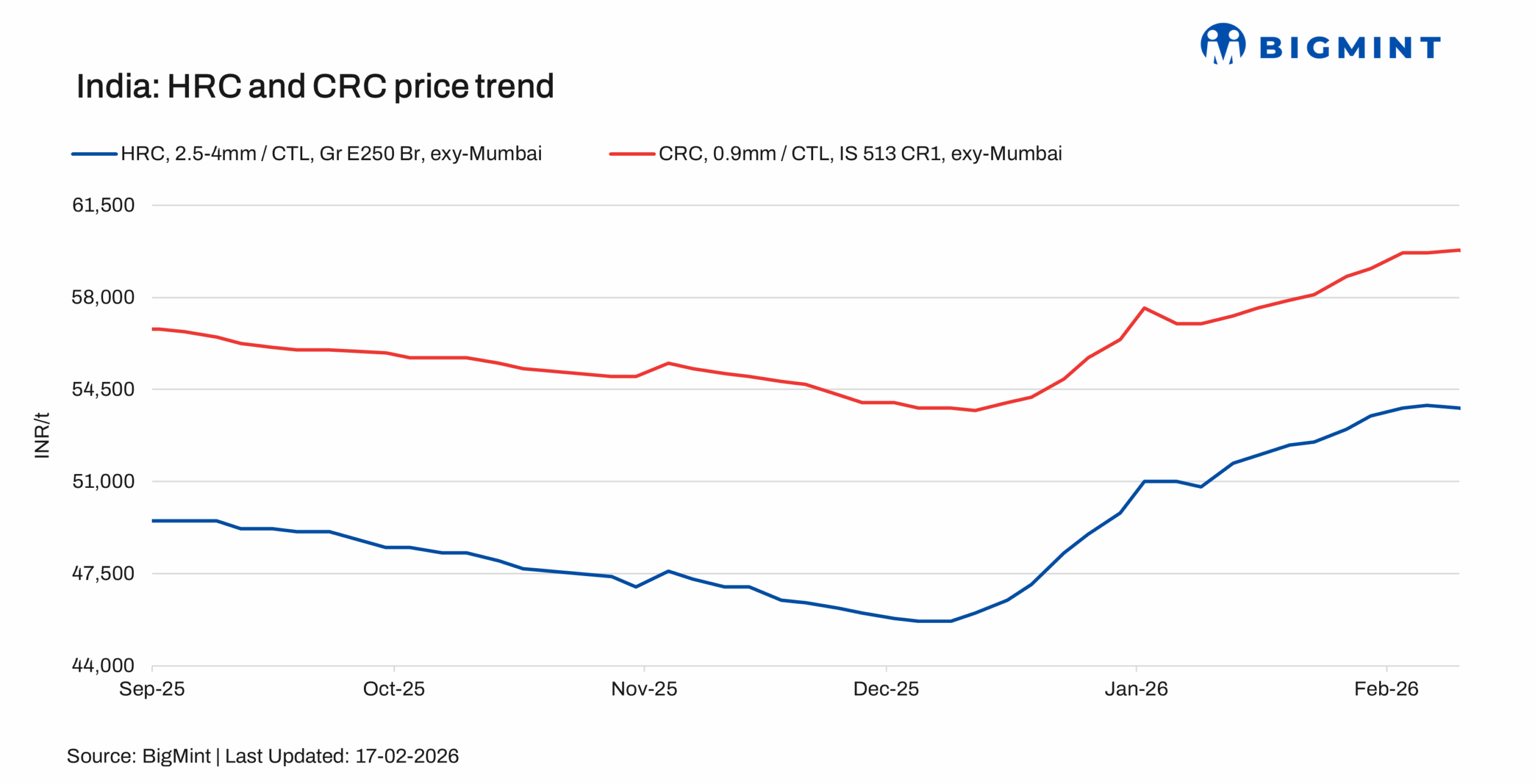

The trade-level prices of hot-rolled coils (HRC) in India held steady in most regions during the week ending 17 February with HRC prices assessed in the range of INR 52,000-55,100/t ($573-608/t) and cold-rolled coil (CRC) prices assessed at INR 56,500-62,000/t ($623-683/t).

BigMint’s benchmark assessment (bi-weekly) for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) observed downtick of INR 200/t ($2/t) w-o-w at INR 53,600/t ($591/t) on 17 February against INR 53,800/t ($593/t).

CRC (IS513, Gr O, 0.9 mm/CTL) prices saw slight decrease of INR 300/t ($3/t) w-o-w to INR 59,500/t ($656/t) on Tuesday against INR 59,800/t ($659/t) a week ago. These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Two major mills have raised HRC and CRC prices by INR 500/t ($5/t) for mid-February sales. However, price hike announcements from other mills are still awaited.

Market updates

South

Demand in the South remains steady, with consumption maintaining normal levels across key sectors. However, a participant from the region noted that “supply has tightened due to a maintenance shutdown at one of the mills”. Overall, the region remains stable, though supply-side constraints are affecting short-term pricing and availability.

North

Market sentiment in the North has weakened over the past week. There was initially strong anticipation of a mid-month price hike from the mills, but since this has not occurred, confidence has declined. Consequently, participants informed Bigmint, “traders have begun booking profits, particularly due to the higher price levels compared to the previous cycle”.

West

The Western market is currently fairly balanced, though trading activity has slowed in recent days. Distributors reported that, “mills are trying to raise prices to counteract the slight decline in market rates and weakening sentiment”. Market feedback suggests that mills are working to maintain pricing discipline despite lower trading volumes. Meanwhile, demand remains steady, and supply in the trade market is sufficient.

Import volumes: India’s bulk imports of HRCs touched 149,529 t as of 13 February, based on vessel line-up data. Around 2,55,163 t of additional cargoes are expected by mid-March.

Export volumes: India’s bulk exports of HRCs touched 31,250 t as of 13 February. Around 1,08,500 t of additional cargoes are in transit.

Outlook

HRC prices in India are expected to remain firm ahead of anticipated mill price hikes next week, despite slightly subdued market sentiments. Additionally, increased demand in key sectors and higher imported cost may create some room for price correction.

Leave a Reply