- Mills’ list price reductions fail to stimulate trading activity

- Rising inventories, slow trade lead to sharper drop in north

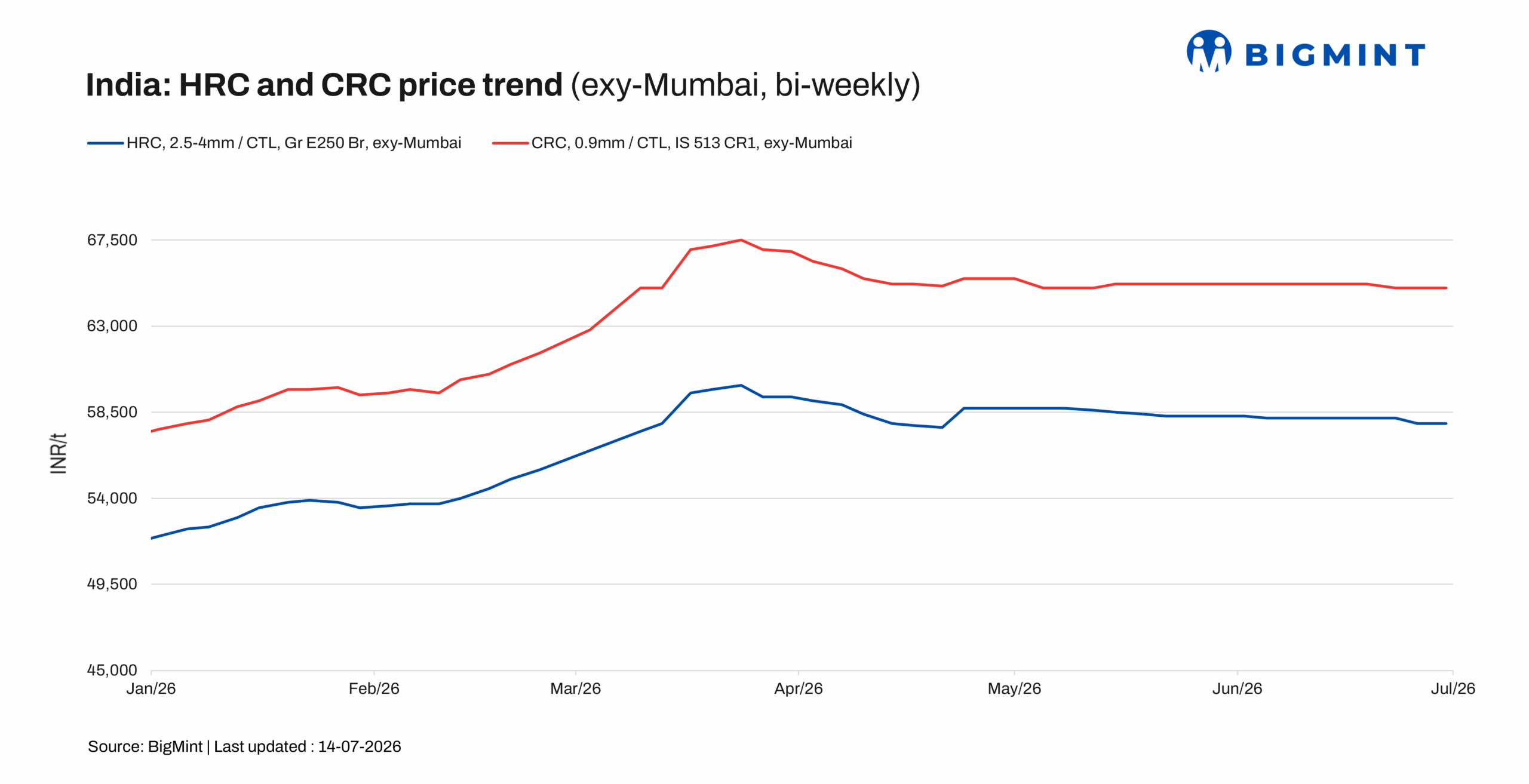

India’s trade-level hot-rolled coil (HRC) prices softened by INR 300-800/tonne (t) ($3-9/t) w-o-w across regions on 14 July 2026 amid subdued, need-based trading activity. Only the eastern market witnessed price stability, though demand was limited there as well.

BigMint’s bi-weekly benchmark assessment placed HRC (IS2062, grade E250, 2.5-8 mm/CTL) at INR 57,900/t ($602/t) ex-Mumbai and exclusive of 18% GST in Mumbai, down by INR 300/t w-o-w. Offers were heard in the range of INR 54,900-58,800/t ($571-611/t).

Meanwhile, cold-rolled coil (CRC) prices (IS513, grade O, 0.9 mm/CTL) remained stable w-o-w at INR 58,800-68,200/t ($620-718/t), reflecting similarly cautious market sentiment and muted buying activity. BigMint assessed prices at INR 65,000/t ($676/t) ex-Mumbai and exclusive of 18% GST on 14 July 2026.

Market update

Last week, major domestic mills reduced HRC list prices by around INR 1,000/t ($11/t) to INR 64,400-67,750/t ($674-709/t) to stimulate trading activity. Despite this, flat steel demand remained subdued across all regions amid weak downstream demand.

In terms of region-wise trends, prices declined the most in the northern HRC market, by INR 800/t in Faridabad. “Rising distributor-level inventories of about 20-25 days and weak downstream demand weighed on trading activity,” a trader informed BigMint. Market participants reported that buying activity was largely confined to immediate requirements, and distributors deferred purchases, as expectations of further price corrections persisted. Overall market sentiment remained weak, as ample stock availability and subdued consumption continued to discourage fresh buying.

In southern India, trading activity also slowed compared with the previous week as monsoon-related disruptions weighed on construction activity and downstream steel consumption. Market participants reported that buying remained largely need-based. Overall market sentiment stayed weak, with muted trading activity and most transactions continuing on credit at a slower pace.

In eastern and western India, market activity remained largely subdued during the week. Prices declined slightly in the western market, but trading activity remained broadly stable compared with the previous week, as buyers continued to procure only against immediate requirements.

Additional updates

Import volumes: India’s bulk HRC imports stood at 91,381 t as of 10 July and are expected to reach 189,349 t by mid-August.

Export volumes: India’s bulk HRC exports stood at 120,160 t as of 10 July.

Outlook

India’s trade-level HRC market is expected to remain subdued through mid-to-late August. Disruptions continue to weigh on construction activity and downstream steel consumption. Supply availability remains adequate across most regions, with no significant constraints reported on the domestic supply side. However, weak buying interest and predominantly need-based procurement are expected to keep trading activity muted and market sentiment subdued. Unless downstream demand improves after the monsoon, domestic HRC prices are likely to remain under pressure over the coming weeks.

Leave a Reply