Market sees limited demand with onset of monsoon: Demand was low because many parts of southern India received heavy rainfall. Additionally, the market continued to grapple with tight cash flows due to high levels of credit sales and slow payment collections.

“The market is experiencing lower demand, as monsoon rains have started in many areas, slowing down construction and related activities. Liquidity problems are also affecting buyers’ ability to make purchases. As a result, many buyers are holding off on purchases, expecting prices to drop or support from mills,” a market participant noted.

Import trends: India’s bulk imports of HRCs and plates touched 249,446 t as of 27 May 2025, based on vessel line-up data from BigMint. Around 21,648 t of additional cargo are expected by May-end and 88,820 t in June 2025.

Export trends: Indian HRC export offers remained stable w-o-w at $630-635/t CFR Antwerp ($580-585/t FOB East India), under pressure from weak demand and seasonal uncertainties. As a result, Indian mills continued to focus more on the domestic market due to better price realisations.

Meanwhile, Chinese HRC offers to the Middle East stayed firm as bookings were made for end-July shipments ahead of Eid-al-Adha. Indian mills remained less active in the Middle East, given stronger domestic margins and competitive Chinese pricing.

Outlook

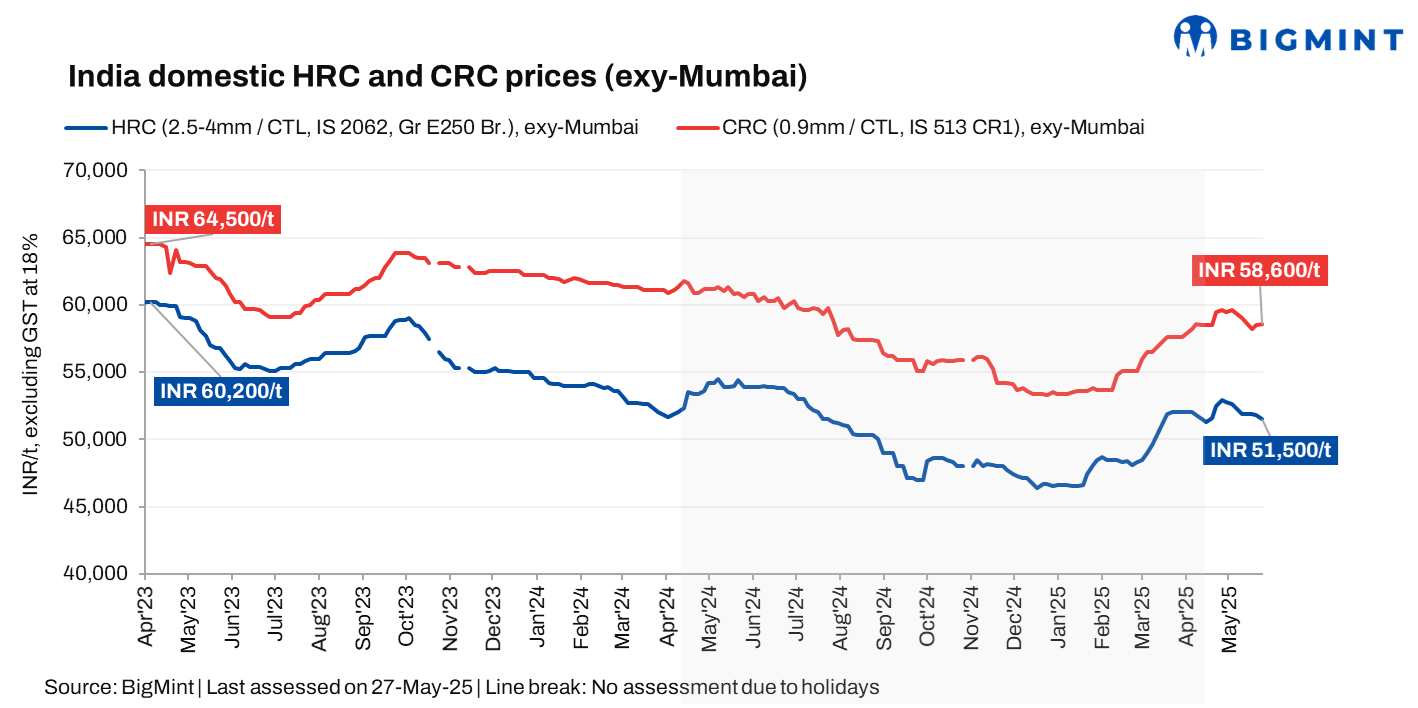

HRC prices may face further downward pressure due to low demand, the monsoon-related slowdown, and liquidity constraints. CRC prices could stay range-bound with limited upside.

Leave a Reply