- Buyers preferring need-based procurements

- Exports, imports of bulk HRCs, plates decline

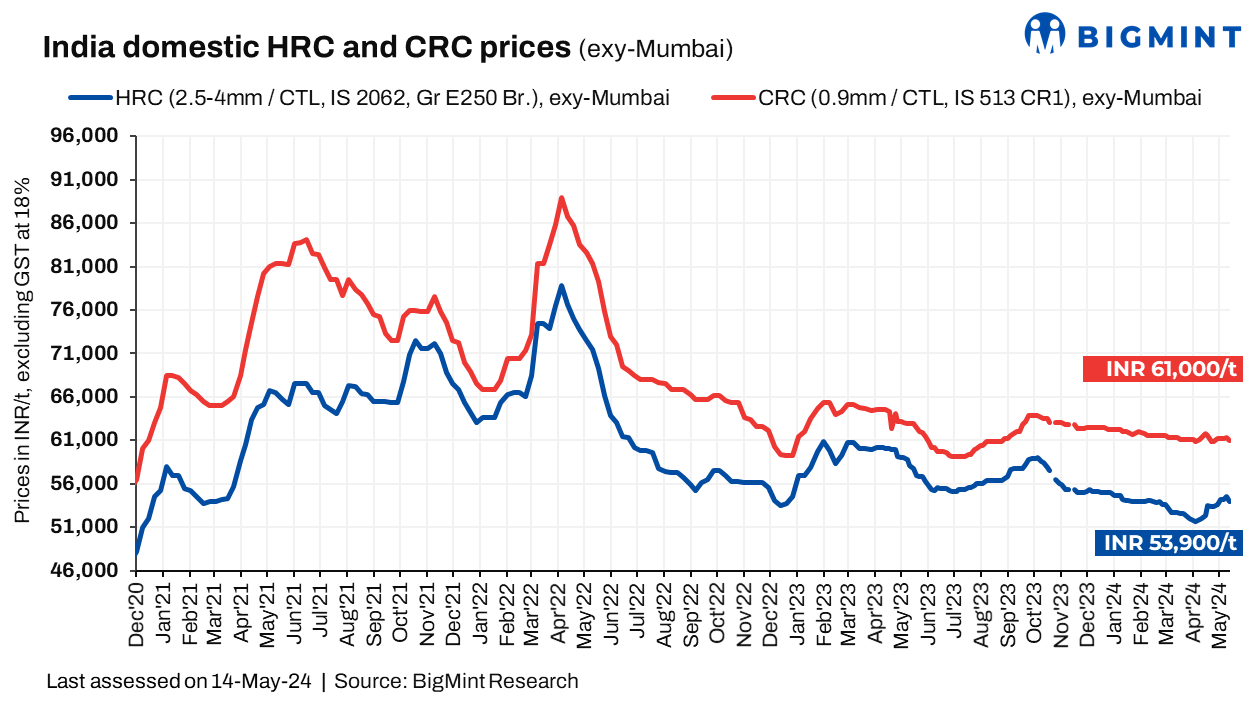

Prices of hot-rolled coils (HRC) and cold-rolled coils (CRC) exhibited divergent trends in recent observations. HRC prices experienced a decline of up to INR 600/tonne ($7/t), now resting within a range of INR 53,900-56,500/t ($645-676/t) across the majority of markets. Conversely, CRC prices saw an increase of up to INR 600/t ($7/t) , reaching a new range of INR 61,000-63,500/t ($730-760/t) across most markets. These fluctuations occurred amidst ongoing subdued trading activity, attributed to challenges in demand and supply dynamics faced by market participants.

BigMint’s benchmark assessment (bi-weekly) for HRC (2.5-8mm, IS2062, Gr E-250 Br.) prices decreased by INR 600/t ($7/t) to INR 53,900/t ($645/t) on 14 May 2024, compared to the previous week. Also, CRC (0.90mm, IS 513, CR1) prices were down by INR 300/t ($4/t) to INR 61,000/t ($730/t) during the same period. These prices are quoted ex-Mumbai, excluding 18% GST, and are for cut-to-length (CTL) deliveries. (INR 1 = USD 0.0119725 ; USD 1 = INR 83.5262)

Market updates:

1. Domestic trade-level prices decline: The trading market exhibited persistent sluggishness due to weak demand. While market participants attempt to justify higher offers as due to supply constraints, buyers are resistant. They prioritise price negotiations and smaller, need-based purchases, leading to a decline in current prices.

A market participant succinctly summarised the situation: “Market demand is currently very weak. Buyers are focused on fulfilling immediate needs with smaller purchases and are pushing back on sellers’ attempts to raise prices.”

2. Export, import trends: Recent data sourced from BigMint’s vessel line-up records indicate a deceleration in India’s exports and imports of bulk HRCs and plates.

Export offers of Indian-origin HRC (SAE1006) to the South East Asian and the Middle East (ME) markets have been on a hold for the fourth consecutive week. Better realisations in the domestic market compared with the overseas markets have kept the mills focused on the former. Furthermore, sluggish market demand within the European Union (EU) has contributed to subdued trade activities across this region.

Outlook

Participants opined that the market will maintain its range-bound trajectory. This can be attributed to subdued demand and apprehensions regarding potential rise in imports in response to further price hikes.

Participants have also expressed the view that the markets are likely to persist within a comparable range for the foreseeable future.