- Exports to Vietnam muted despite dumping exemption

- Buyer resistance, fiscal year-end may keep prices stable

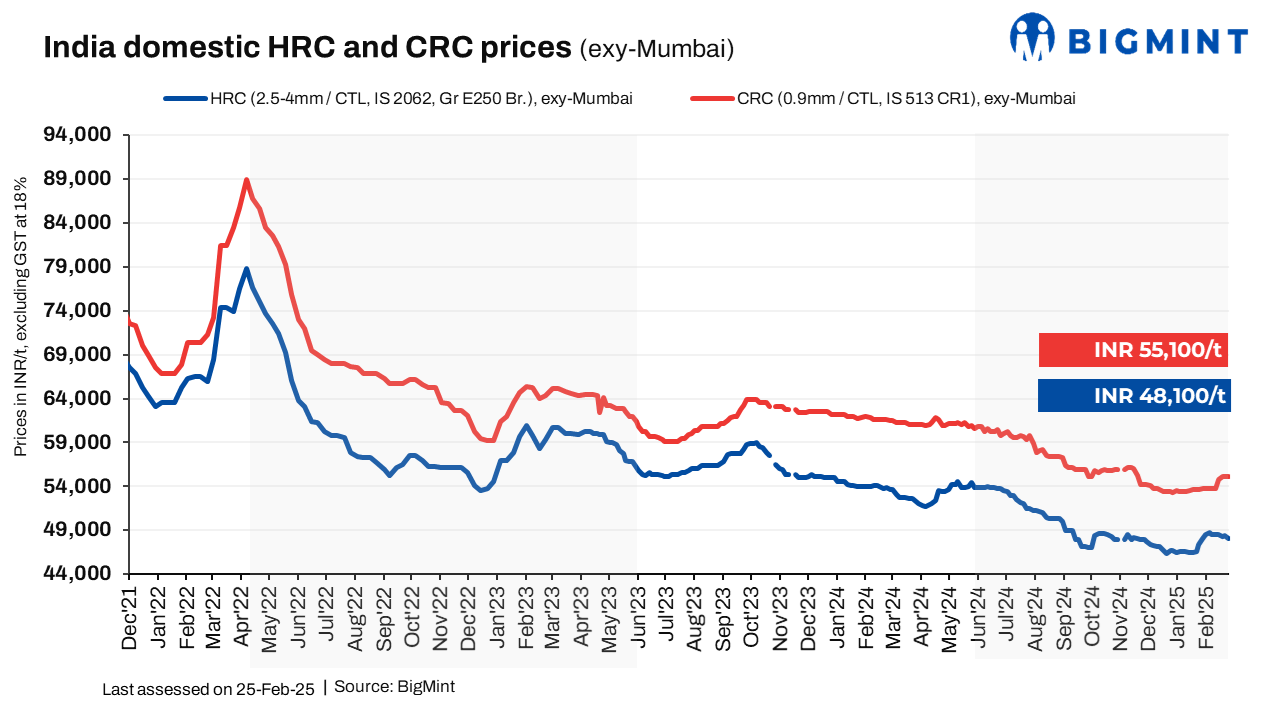

Trade-level hot-rolled coil (HRC) prices across India declined marginally by up to INR 300/tonne (t) w-o-w to INR 47,200-49,500/t. Conversely, cold-rolled coil (CRC) prices witnessed mixed trends w-o-w, settling at INR 53,100-56,000/t ($617-671/t) across markets.

BigMint’s benchmark assessment (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) declined marginally by INR 300/t w-o-w to INR 48,100/t ($549/t) on 25 February 2025. However, CRC (IS513, Gr O, 0.9 mm/CTL) prices remained stable w-o-w at INR 55,100/t ($628/t). These prices are quoted ex-Mumbai for the distributor-to-dealer segment and exclude the 18% GST.

Market updates

Domestic trade market sees need-based buying, price resistance: Market conditions deteriorated, resulting in decreased sales and demand. Buyers exhibited strong price sensitivity, restricting purchases to immediate requirements and rejecting any proposed price increases.

“Demand has significantly weakened, resulting in low sales volume. Distributors hold substantial inventory post-MOU fulfillment while awaiting some support from mills. It is anticipated that subsequent inventory liquidation, driven by balance sheet considerations, may lead to price corrections,” said a market participant.

Import trends: Imports of bulk HRCs and plates stood at 3,83,294 t till 24 February, as per vessel line-up data maintained with BigMint. It is expected that an additional 38,195 t will be imported by the month-end and 82,349 t in the first week of March.

Export trends: The BigMint India HRC (SAE 1006) export index to the Middle East and Vietnam remained stable at $505/t FOB, reflecting reduced trade activity ahead of Ramadan. Despite Vietnam’s anti-dumping duties on Chinese HRCs, and which exclude Indian imports, mills from the latter are not actively exporting to Vietnam. HRC exports to the EU are also limited, pending the outcome of the anti-dumping investigation and new import quota announcements.

Outlook

Distributors hold high inventories post-MoU fulfillment, potentially leading to liquidation-driven price corrections. Imports remain steady, with additional shipments expected in early March. Export activity is muted, with Indian mills staying cautious amid Vietnam’s duties on China and ongoing EU trade investigations.

With resistance to higher prices and the financial year coming to an end, prices are expected to remain range-bound.

Leave a Reply