- Bid-offer disparities, monsoon dampen sentiment

- Production ramp-ups to increase supply in near term

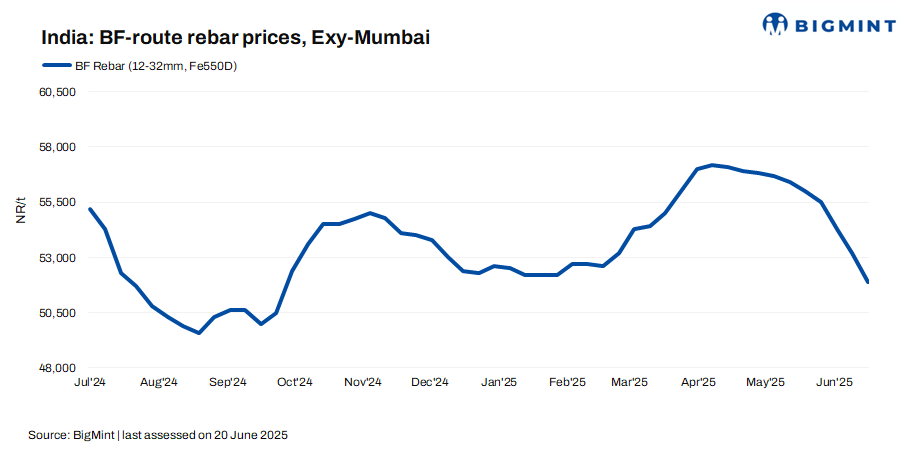

India’s trade-level blast furnace (BF) rebar prices declined w-o-w, driven by weak demand, cautious market sentiment, and a monsoon-led slowdown in trade momentum. Buyers adopted a wait-and-watch approach due to the prevailing disparity between bids and offers, while distributors focused on liquidating high-cost inventories.

Major primary steel producers reduced rebar prices amid lacklustre trade, with list prices ranging between INR 51,500-52,500/tonne (t) ($595-606/t) on landed basis. Inventories at large integrated mills rose significantly to around 400,000 t as of mid-June, according to sources.

Trade-level BF rebar prices declined by INR 1,300/t ($15/t) w-o-w to INR 51,900/t ($599/t) exy-Mumbai, as per BigMint’s assessment on 20 June 2025. Prices are exclusive of GST at 18%.

In the projects segment, prices declined further to INR 51,000-51,500/t ($589-595/t) FOR Mumbai, weighed down by continued bid-offer disparities and subdued construction activity due to the ongoing monsoon season.

Factors behind market dynamics

1. Supplies to increase in near term: On the supply side, production ramp-ups are expected to intensify pressure on prices. A major private mill has restarted its BF and hot metal production, while another has resumed normal operations at its Linz-Donawitz (LD) converter. Additionally, a third BF at a public sector undertaking (PSU) steelmaker is set to begin operations this month, likely adding further volumes to the market.

2. Selling pressure drags down IF rebar prices: IF rebar trade prices remained under pressure this week amid monsoon disruptions and labour shortages impacting construction demand. Mills cut list prices and offered discounts, as inventory levels rose to 12-15 days, with some regions seeing even higher stockpiles. Weak buying interest and continued drops in semi-finished and sponge iron prices further dampened sentiment. IF rebar prices dropped by INR 900/t ($10/t) w-o-w to INR 44,000/t ($508/t) exw-Mumbai as on 20 June.

The BF-IF rebar price gap narrowed slightly to around INR 7,500-8,000/t ($87-92/t) in Mumbai. IF rebars hold a dominant 65-70% market share in India.

3. Raw material prices show mixed trends w-o-w: BigMint’s Odisha iron ore fines (Fe 62%) index remained stable w-o-w at INR 5,050/t ($58/t) on 14 June 2025, supported by need-based buying from steelmakers. Despite weak steel demand and lower pellet prices, miners held offers steady, with moderate market activity driven by operational needs over restocking.

Australian premium hard coking coal (PHCC) prices dropped by $7/t w-o-w to $194/t CNF Paradip.

Outlook

Market participants expect rebar prices to correct further and likely bottom out in the coming days. Procurement remains cautious amid weak demand and falling prices.

Leave a Reply