- IF-rebar prices drop w-o-w amid subdued demand

- Buyers move to side lines amid volatility in prices & uncertainty

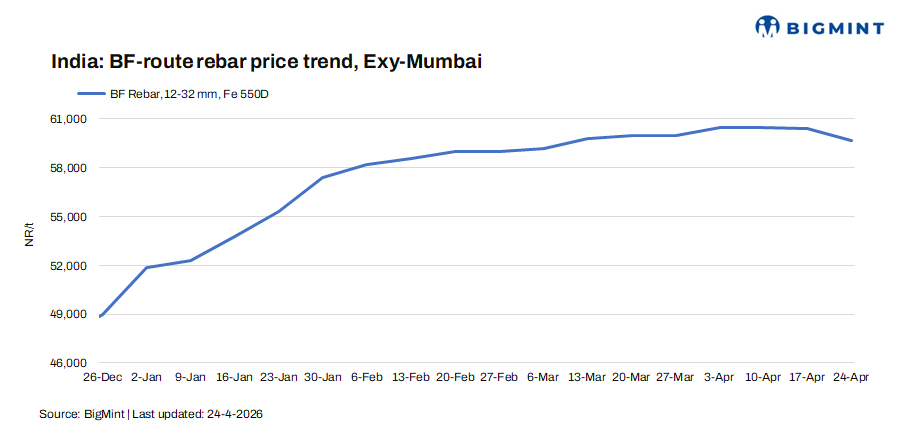

Trade-level BF-rebar prices (distributor to dealer) dropped by INR 700/t ($7/t) w-o-w to INR 59,700/t ($633/t) exy-Mumbai, as per BigMint’s assessment on 24 April 2026. Buying activities witnessed slowdown this week with buyers moving to sidelines amid cautious market sentiments.

Rebar project prices were workable in the range of INR 58,500-59,500/t ($620-631/t) on a landed basis, as per sources. Demand remained weak with limited inquiries as buying slowed. Election-related labor shortages disrupted construction activity, delaying procurement. Buyers adopted a cautious stance amid price volatility & uncertainty.

Update on projects

- H.G. Infra Engineering secured INR 519 crore order from Mirzapur Thermal Energy (UP) Private Limited for railway infrastructure works, execution period 18 months.

- PNC Infratech emerged L1 bidder for two National Highways Authority of India HAM highway projects worth INR 3,483 crore in Uttar Pradesh.

- Sterling and Wilson Renewable Energy Limited (SWREL) won INR 3,550 crore orders, including 875 MW Coal India solar EPC and 50 MW private IPP project, lifting FY26 inflows.

- L&T secures India orders including Gurugram residential towers and Haryana proving ground, strengthening Buildings & Factories expertise and execution capabilities.

- J. Kumar Infraprojects wins Mumbai Metro and MCGM contracts worth over INR 2,400 crore for metro connectivity, bridges, and road infrastructure projects.

- GR Infraprojects signs INR 413 crore EPC agreement with NTPC for battery energy storage system at Mouda thermal power station project.

- HCC won INR 2,917 crore CIDCO contract to build tunnel, water plant in Raigad, strengthening Navi Mumbai’s long-term water supply infrastructure.

- Ashoka Buildcon won $72.36 million Angola contract for power distribution network rehabilitation in Luanda, to be executed within 24 months.

Factors behind market dynamics

1. IF rebar prices drop w-o-w: Induction Furnace (IF) route rebar prices exhibited volatility & downtrend this week across major markets. Trading activity remained subdued, reflecting cautious market sentiment. Demand was weak across both finished and semi-finished steel segments, as buyers largely adopted a wait-and-watch approach amid falling prices.

In response, manufacturers reduced offers and extended discounts in an effort to stimulate buying interest. Market participants anticipate continued price fluctuations, driven by weak order bookings in the finished steel segment. Meanwhile, mill inventory levels stood around 8-12 days. Induction furnace (IF) rebar trade prices dropped by INR 1,000/t ($11/t) w-o-w to INR 51,100/t ($542/t) exw-Mumbai as of 24 April.

The blast furnace (BF) to IF rebar price spread in Mumbai widened w-o-w to around INR 8,500-9,000/t ($90-95/t) this week. IF rebar continues to dominate the Indian market, accounting for an estimated 65-70% share.

2. Raw material prices show mix trend w-o-w: Prices of major raw materials used in the BF route showed mix trends w-o-w. BigMint’s Odisha iron ore fines (Fe 62%) index was stable w-o-w at INR 5,750/t ($61/t) ex-mines as on 19 April. Iron ore prices in Odisha stayed stable as buyers waited cautiously for OMC auction, limiting spot purchases and relying on auction volumes.

BigMint’s premium hard coking coal (PHCC) prices dropped by $5/t w-o-w to $253/t CNF Paradip.

Outlook

Prices of BF-rebar are expected to exhibit a downward trend from current levels amid subdued buying pattern & weak market sentiments.

Leave a Reply