- Sponge iron and melting scrap prices remained firm w-o-w

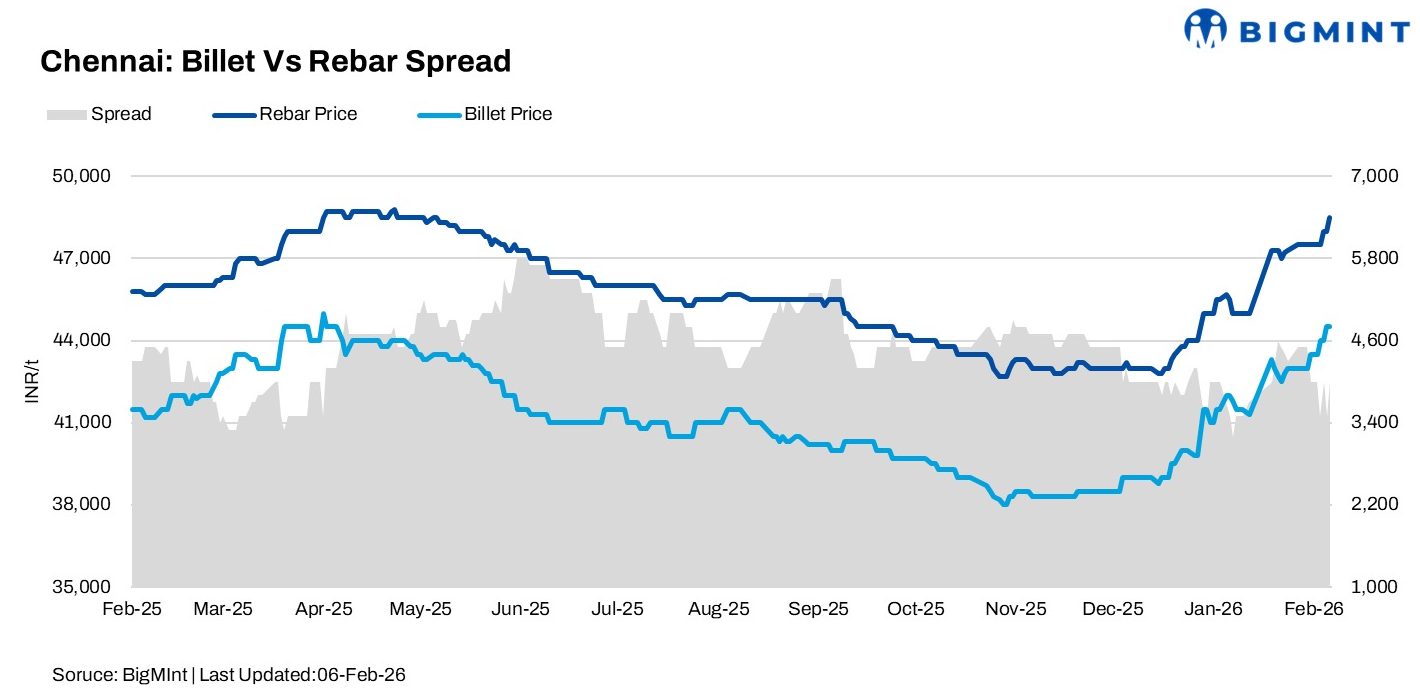

- MS billet prices in the Chennai increased by INR 1,500/t w-o-w

Sponge iron prices in the Bellary cluster remained slightly supported, rising by around INR 500/t on w-o-w basis. The increase was mainly driven by higher iron ore pellet and non-coking coal prices, along with a shortage of melting scrap within the region.

Limited scrap availability has further strengthened sponge iron demand, as steelmakers increasingly relied on DRI as an alternative raw material. This substitution trend helped maintain firmness in sponge iron transactions despite moderate buying activity.

Currently, pellet-based DRI prices in Bellary are assessed at INR 26,500/t Ex-Works on regular payment terms. Suppliers showed limited willingness to negotiate, citing elevated input costs and restricted raw material availability.

Meanwhile, melting scrap prices in the Chennai region turned marginally positive. The improvement was supported by rising global scrap prices and continued domestic supply constraints.

Due to unreliable domestic scrap availability, steel manufacturers are increasingly opting for imported scrap via containerized shipments, even at slightly higher prices. This preference for supply security over price sensitivity is expected to keep scrap prices supported in the near term.

Semi-Finished Trends :

MS billet prices in the Chennai cluster witnessed an increase of around INR 1,500/t (DAP Chennai) on week on week basis. The price rise was mainly supported by tight spot market availability, as billet producers offered limited volumes while demand from southern consuming markets remained steady.

The shortage of spot material prompted buyers to accept higher offer levels, allowing sellers to strengthen prices in the local market. As a result, MS billet prices are currently assessed at around INR 44,500/t DAP Chennai for regular payment terms, with limited scope for immediate correction.

Finished Long Steel Scenario :

On the finished steel front, rebar demand improved compared to previous weeks, supported by a price hike announced by blast furnace route producers for the February cycle. The increase provided a firm pricing benchmark and improved overall market sentiment.

The higher BF-route rebar prices enabled induction route manufacturers to revise their offers upward. Elevated semi-finished steel prices and rising conversion costs further supported this move, as producers aimed to maintain healthy conversion spreads.

At present, blast furnace route rebar prices (12-25 mm) are assessed at around INR 57,500/t ex-yard for Chennai and Hyderabad.

Leading steel manufacturers continue to offer induction route rebars in the local market at prevailing levels, with limited discounting observed amid stable demand conditions.

Outlook :

Near-term steel prices are likely to remain stable to firm, supported by the absence of selling pressure across major clusters. Tight availability of key raw materials, including melting scrap, continues to limit aggressive selling. Meanwhile, healthy demand from steel manufacturers across key consuming regions is expected to sustain current price levels.

Leave a Reply