The excess supply in rebar inventories from tier-1 mills has reversed over the last couple of months. Volumes held with the mills dropped around 25% in early April, as per information available with BigMint. From levels of 500,000 tonnes (t) seen in early March, 2024, these have fallen off to 350,000-375,000 t in early April.

Reasons behind the inventory depletion

Good projects demand in end-March: The market saw decent restocking demand last month from the project segment essentially because buyers were keen to stock up ahead of the fiscal year-end and also because they wanted to beat election-related supply disruptions. Thus, mills have been busy in April, supplying orders placed in March.

Production cuts by tier-1 mills: Around 70,000-80,000 t of production loss is expected in rebars in April, as per information available. It may be noted that mills have been undertaking production cuts since January in a bid to restore the supply-demand imbalance that led to an inventory glut in earlier in the year.

MoU completion with distributors ahead of FY closing: With the fiscal year-end approaching, many large mills increased their discounts with distributors as an incentive to lift larger volumes. Usually, an MoU is inked at the beginning of each financial year where the distributor agrees to lift a certain amount of material. However, if mills see towards the year-end that the commitment is not getting fulfilled because of certain market forces, then they increase the discounts to incentivize the trade segment. Last fiscal was no exception and led to a spurt in offtake from distributors around March.

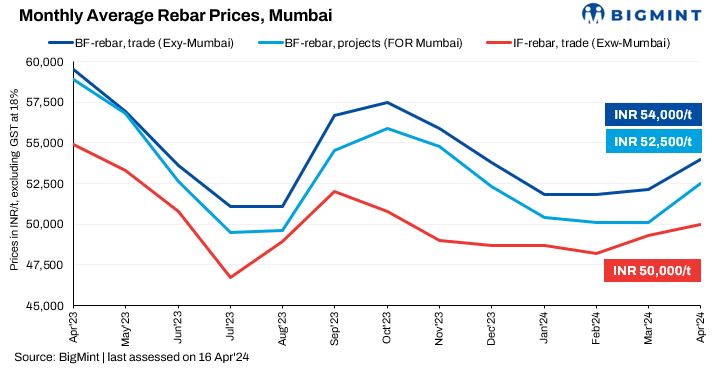

IF mills see decent bookings: In March, prices saw an uptick post-Holi. But IF mills too saw decent pre-election demand pull. As a result, the number of days for inventory idling reduced from 8-10 days in March to 5-7 days in April. Some mills undertook maintenance for 2-3 days in April, which also helped to rationalize production and keep demand buoyant and led to a price rise. Some good deals were closed on the back of the price rise, as buyers feared further price escalations. IF mills enjoy 65-70% of the rebar market.

Outlook

Rebar prices may remain firm in the near term because of a few factors. First, thanks to the inventory depletion, mills are not under any pressure. Secondly, the adequate number of bookings in March will also allow mills to hold on to their current price levels for the remaining portion of April. Thirdly, pre-election demand will keep margins healthy.