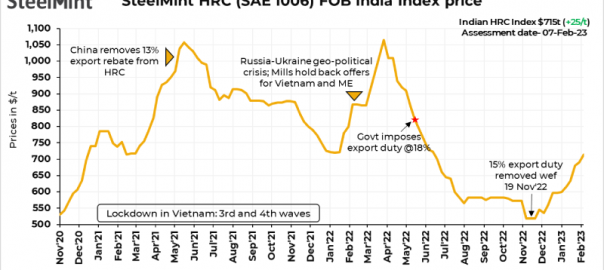

- HRC export index at $715/t FOB

- Deals concluded for Middle East, Europe

- Buying subsides amid decline in Chinese offers

SteelMint’s India HRC (SAE1006) export index rose by $25/t to $715/t FOB east coast from $690/t FOB last week. Mills continued to hold back offers for Vietnam. Meanwhile, some deals were reported for Middle East and the European Union. However, with the fall in Chinese steel futures and prices, market trends have slowed down globally.

Rationale: Six indicative prices were considered as T2 inputs. Meanwhile, a deal for 20,000 tonnes of hot rolled coils (HRCs) concluded last week at $750/t CFR UAE for delivery in March 2023 was considered as T1. The final price was an average of T1 and T2 inputs which stood at $715/t FOB. CFR prices were converted to FOB equivalent by deducting freight costs from the buyer/seller.

Why is overseas buying interest subsiding?

1. Indian offers remain on higher side: Indian mills have been quoting aggresively for HRCs on the higher side since the beginning of January 2023. Now that the export offers on the global platform are showing signs of weakening, buyers are seen moving to the sidelines.

a) Uptrend in raw material prices: The continual increases in raw material prices has led to higher offers from Indian mills while the uptrend in HRC export offers in the recent past lent further support. Furthermore, industry participants opine that raw material prices should stay range-bound in the near term.

b) Higher domestic realisations: Indian mills are enjoying higher prices in the domestic market as compared with those in the overseas markets. SteelMint’s benchmark HRC (IS2062, 2.5-8mm) prices were assessed at INR 60,500-61,500/t ($731-743/t) exy-Mumbai, excluding GST @ 18% as on 1 February 2023. This is still higher as compared with the current indications for the overseas markets.

2. Price disparity emerges in overseas markets: Indian steel mills are seeing price disparity emerging in overseas markets. Mills have not been quoting in the Vietnamese market amid competitive offers from China and Japan, which would weigh on the sales realisations. Where Chinese mills are offering HRCs (SAE1006) at $650-660/t CFR Vietnam and these are down by $30/t w-o-w, the Japanese floated offers at $700/t CFR after a long gap. “Indian mills should be eyeing counter bids at least at around $720/t CFR Vietnam to make some profits,” informed a reliable source. But they are unlikely to achieve such levels amid lower offers from China and Japan, he added.

Meanwhile, offers for Chinese HRCs (SAE1006) were heard ranging around $710-720/t CFR UAE, dropping from the level of $720/t CFR last week. Indian mill indications were heard at around $750/t CFR this week.

3. Buying interest subsides in European market: The European market also saw a decline in buying interest this week after having reported deals over the past couple of weeks at elevated price levels. Last week, a small parcel of HRCs was heard booked for exports at $800/t CFR for delivery in March 2023, informed sources. Fresh indications for HRCs (S275) were floated at $800-810/t CFR Antwerp.

Outlook

The depreciation of the euro against the dollar made buyers side-step while the Chinese export offers have started showing signs of weakening this week. The Chinese HRC futures (May 2023 contracts) on SHFE have been on a continual decline till 5 February since the market resumed tracking on 30 January. The settled price of HRC futures stood at RMB 4,065/t ($599/t) on 7 February, down by a steeper RMB 133/t w-o-w ($20/t), contrasted against RMB 4,198/t ($619/t) as on 31 January.

Leave a Reply