- Subdued finished steel trade offsets tight scrap supply

- Construction activity may be deferred for GST benefits

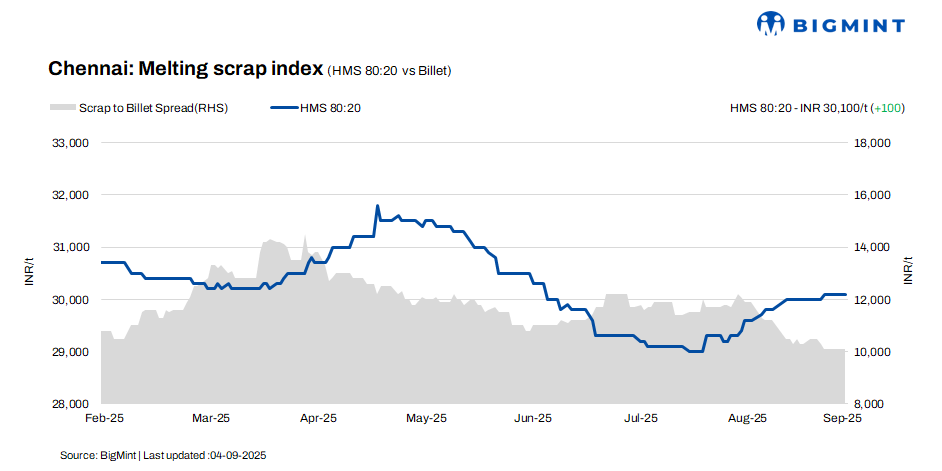

HMS (80:20) prices in Chennai inched up by INR 100/tonne (t) w-o-w to INR 30,100/t, with no change on a d-o-d basis, according to BigMint’s latest assessment. Billet prices, however, remained steady d-o-d but dropped INR 100/t w-o-w, settling at INR 40,200/t. Meanwhile, rebar prices strengthened by INR 200/t d-o-d while remaining firm w-o-w, closing at INR 45,500/t.

The market continued to show mixed trends, where stability in scrap lent support, but weak billet demand capped overall momentum.

Imported, domestic scrap price trends

According to a scrap trader, Australian shredded scrap offers are currently quoted at $360-365/t, against buyer bids of $350-355/t. HMS (80:20) is assessed at $330-335/t. Despite competitive offers, demand for imported scrap remains weak, with many buyers preferring domestic scrap due to its cost advantage and equivalent quality.

In Chennai, domestic HMS (80:20) was traded at INR 30,000-30,500/t for spot deals with immediate payment, while trades on extended credit terms were slightly higher at INR 30,500-31,000/t. Market activity largely remained within the INR 30,000-31,000/t band, reflecting the strong role of liquidity preferences and credit-based pricing dynamics in shaping concluded transactions.

Buyer-supplier sentiments

As per sources, billet demand weakened in recent days, although offers remained largely unchanged. Offers from nearby states were heard to be slightly lower than local billets. However, due to quality concerns, most mills continued to prefer sourcing locally.

Meanwhile, in the recent GST Council meeting, it was announced that the rate on cement bags will be reduced from 28% to 18%, effective 22 September 2025. This development may impact near-term demand, as buyers are likely to defer construction activities to avail the GST benefit. Consequently, rebar demand could also see a slowdown in the coming days.

According to local suppliers, domestic HMS (80:20) prices were assessed in the range of INR 30,000-31,000/t, with minor variations based on payment terms. While domestic scrap availability remained slightly tight, subdued finished steel trade activity in recent days kept buying sentiment cautious. Market participants expect scrap prices to stay range-bound in the near term, with broader trends likely to hinge on demand recovery in finished steel.

Regional comparison

In the Jalna market of western India, billet and rebar prices rose by INR 300/t d-o-d, settling at INR 39,500/t and INR 43,600/t, respectively. HMS (80:20) scrap prices also edged up by INR 100/t d-o-d to INR 31,000/t. Trade activity for rebar improved in today’s session compared to the past few days, while scrap supply was adequate to meet mill requirements.

Outlook

Sources indicate that domestic scrap prices are likely to remain range-bound in the near term, with fluctuations expected to be limited to INR +/-500/t. The relative stability is being attributed to prevailing uncertainty in the finished steel market, where both buyers and sellers are maintaining a cautious stance. Consequently, volatility in scrap prices is expected to stay subdued within a narrow band.

Leave a Reply