- Lower interest in imported thermal coal on higher CIL production

- Silico manganese sees uptrend on improved export demand

- Price pressures may not ease in short term in dull market

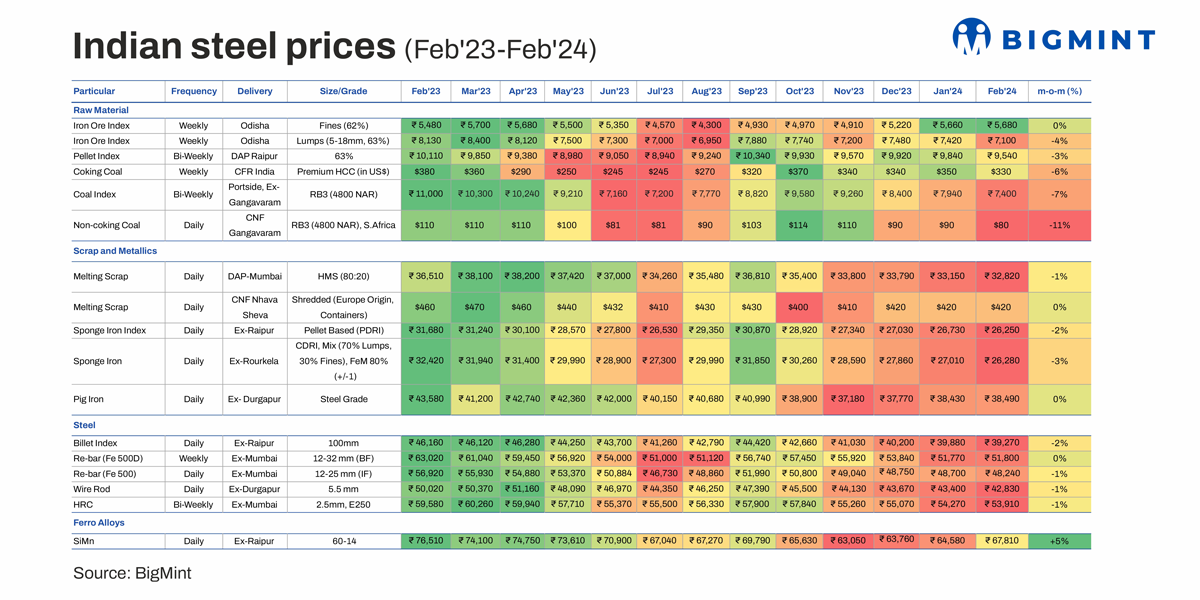

Morning Brief: Steel and raw material prices, reflecting the global trend, showed a marginal drop or remained flat m-o-m in February 2024 for the second month in a row, amid the continued tepid steel demand, geopolitical strains and the China factor. Thermal coal-the RB3 (4800 NAR) from South Africa-showed the steepest drop while silico manganese slightly bucked the trend.

BigMint goes behind the scene:

Factors that influenced domestic steel, raw material prices in Feb’24

Coal

- Australian Premium HCC coking coal: Average Australian Premium HCC coking coal prices fell 6% m-o-m to $330/tonne (t) CFR India in February 2024 compared to $350/t in January 2024.

The price erosion can be attributed to concerns persisting among end-users regarding the sustainability of prevailing price levels. The price drop was a function of sluggish demand from India and a declining Chinese market. A certain amount of wait-and-watch sentiments prevailed. Amidst this backdrop, trade remained thin in the Asian market, with some sellers refraining from actively offering their cargoes due to uncertainty surrounding a major Australian miner’s coal supply pipeline for the April-loading window.

- Indexed port-side ex-Gangavaram prices of RB3 (4800 NAR) from South Africa fell 7% to INR 7,400/t in February 2024, from INR 7,940/t in January. This same grade of thermal coal, CNF Gangavaram, fell the sharpest at 11% amongst all steel-related raw materials to $80/t last month from $90/t in January. RB3 prices dropped majorly because of low domestic demand amid sufficient port inventories in India and rise in domestic production which reduced imported coal requirement. Coal India’s production rose 9% y-o-y to 74.8 million tonnes (mnt) in February 2024 as against 68.8 mnt in February 2023.

Ferro alloys

- Silico manganese 60:14: Prices of the bi-weekly 60:14 grade silico manganese index in Raipur rose 5% m-o-m to INR 67,810/t in February 2024 (INR 64,580/t in January). The price increase was propelled by mainly three factors. One, a certain amount of production cuts led to lesser supply in the market. Two, there was a spurt in domestic enquiries. Three, a surge in export demand also played a key role. In fact, manufacturers upped prices keeping in mind the export enquiries. The second week of February saw prices touching a four-month high of INR 67,700-68,000/t.

Scraps and metallics

These continued to move in a narrow range in a month marked by lacklustre finished steel demand.

- Pellet-based P-DRI: Pellet-based P-DRI, ex-Raipur, dipped a slight 2% m-o-m to INR 26,250/t in February, compared to INR 26,730/t in January.

- CDRI mix: Prices of CDRI with a mix of 70% lumps, 30% fines, FeM 80% (+/-1), ex-Rourkela, declined another 3% m-o-m in February to INR 26,280/t (INR 27,010/t in January 2024).

This decline was mainly because of the prevalent negative market sentiments. Buyers were cautious about price swings, because of similar drops seen in semi-finished and finished segments as well. BigMint’s Raipur billet index (100x100mm) showed a sharp decreased of INR 600/t m-o-m to INR 39,250/t exw Raipur in February 2024.

- Steel grade pig iron: Pig iron prices remained flat m-o-m at INR 38,490/t (INR 38,430/t in January 2024). The decreasing demand for finished products has been affecting pig iron prices too. But the fluctuating prices of met coke kept pig iron supported. Thus, although production costs were stable, weak demand forced prices to remain static.

- Domestic melting scrap HMS 80:20 (ex-Mumbai): These fell m-o-m 1% to INR 32,820/t in February against INR 33,150/t in the previous month. In Mumbai and other markets, scrap held more or less steady amid enough scrap inventory. Thus, mills were not concerned about supply. Moreover, imported scrap offers were higher compared to local material. There was a gap of about INR 1,000-1,500/t between imported and domestic prices, which eased pressure on the latter.

- Imported melting scrap: Prices of shredded melting scrap of Europe origin, in containers, CNF Nhava Sheva, remained flat m-o-m in February 2024 at $420/t. In fact, these prices have been holding steady for three months in a row now.

In February, imported scrap offers from Europe remained largely unchanged m-o-m due to sellers’ resolute stance, driven by limited availability of scrap in their respective domestic markets and heightened collection costs. Despite the availability of cost-effective alternatives in the domestic market, demand from India remained subdued.

Furthermore, buyers had enough domestic inventories in hand and additionally showed a preference for non-European origins because of price viability.

Iron ore

Iron ore lumps and pellets showed a falling trend last month, although fines managed to stay inert m-o-m.

- Fines & lumps: Fe62% fines from Odisha remained static m-o-m in February 2024 to INR 5,680/t (INR 5,660/t in January) while the Fe63% lumps (Odisha) lost 4% to INR 7,100/t (INR 7,420/t) m-o-m.

- Pellets: The bi-weekly pellets (63%) index dipped 3% to INR 9,540/t (INR 9,840/t) in February amid lacklustre sponge iron demand. Pellets are a key raw material for sponge producers.

Indian pellet export prices to China dropped by around $12/t m-o-m in February amid the Lunar holidays. Thus, Indian domestic iron ore prices were impacted. Hence, high grade ore or pellets were not in demand from China, which in turn also impacted domestic pellet prices.

Moreover, Odisha iron ore fines prices edged down towards the second half of February but did not fall sharply as key Odisha merchant mines have exhausted their EC limits, which can pressure supplies.

Steel

This segment, comprising billets and finished products, mainly saw a marginal dip.

- Billets: The ex-Raipur billet index dropped 2% to INR 39,270/t in February, 2024 (INR 39,880/t in January) amid a fall in finished steel demand and sponge iron prices.

- Rebar & wire rods: The ex-Mumbai BF-grade remained flat m-o-m at INR 51,800/t (INR 51,770/t) in the period under review. Easing of BF rebar inventories in February, along with the production cuts, helped to keep prices flat. However, the IF grade fell 1% to INR 48,240/t (INR 48,700/t) while wire rods (ex-Durgapur) fell by a similar percentage to INR 42,830/t (INR 43,400/t) last month. IF-grade materials fell as billets and sponge were not so supportive.

- HRC: Ex-Mumbai trade-level HRC prices dipped 1% m-o-m to INR 53,910/t (INR 54,270/t). Sentiments continued to remain low amid additional supplies and substantial imports against a backdrop of slow demand.

Outlook

Domestic demand is still dull while Chinese exports are expected to remain aggressive in the short term while overall global demand is subdued. Thus, the cost pressure may still remain in March as market fundamentals are not likely to show sharp positive changes.