- Chennai billet prices increased by INR 300/t week-on-week

- Steel demand improved across South India, supporting overall market sentiment

Sponge iron prices in the Bellary–Hospet region increased sharply by around INR 500–600/t at the beginning of the week. However, the momentum gradually slowed and prices stabilized toward the latter part of the week. The initial rise was supported by firm iron ore pellet and non-coking coal prices, which kept input costs elevated and sustained overall market sentiment, with limited downside visible in the near term.

Steel manufacturers continue to increase the usage of pellet-based sponge iron due to the persistent shortage of melting scrap in the cluster. This has resulted in healthy offtake and sustained demand across the region. Most sponge iron producers have already secured bookings for the next 7–10 days, thereby avoiding immediate sales pressure and maintaining price stability.

Meanwhile, melting scrap prices in Chennai rose by INR 300–400/t amid improved demand from steelmakers and slight material scarcity. Firm global cues, with HMS 80:20 (Australian origin) assessed at around $349/t CNF Chennai, are encouraging steelmakers operating DRI kilns to enhance the sponge iron ratio in their production mix to maintain output levels.

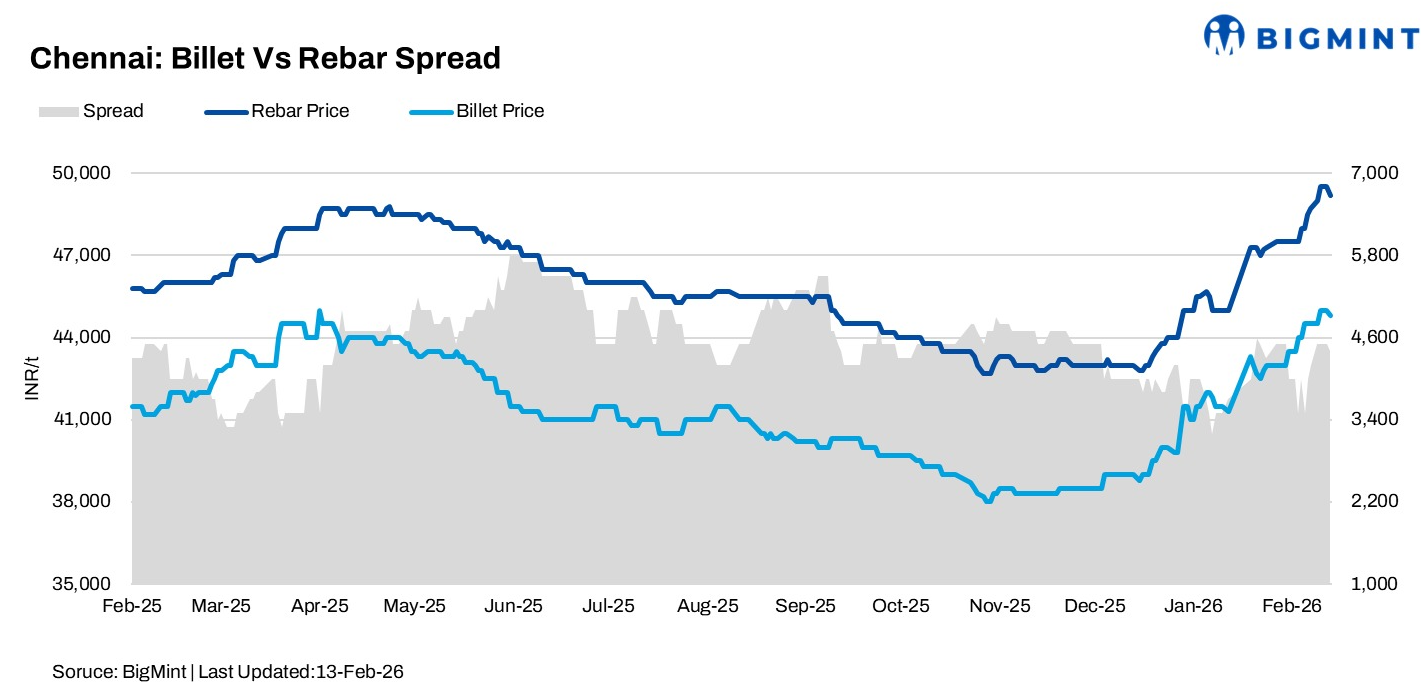

Semi-finished steel – Billet trends

Semi-finished steel – Billet trends

MS billet prices in the Chennai clusters remained supported, witnessing a marginal uptick. The firmness is primarily driven by scrap scarcity, which has tightened raw material availability and restricted billet supply, enabling mills to improve offer levels.

Improved demand in the finished steel segment, particularly rebar, has further strengthened billet buying sentiment. Merchant suppliers have slightly increased their offers, with the current assessed price for Chennai billet standing at around INR 44,800/t FOR Chennai under regular payment terms.

Finished steel scenario:

Finished steel demand across South India has shown steady improvement over the past few weeks. Project segment activity has picked up, with the current supply mix assessed at around 65% project and 35% retail demand. Approximately 70–80% of daily production is being dispatched within the region, indicating healthy market absorption. The price gap between induction furnace (IF) and blast furnace (BF) route materials currently stands at around INR 8,000/t in the Chennai and Hyderabad markets. BF route rebar prices in these regions are assessed at approximately INR 57,500–58,000/t exy, reflecting firm demand conditions.

Price outlook

Steel prices in South India are expected to remain stable or witness slight support in the near term. The outlook is backed by healthy offtake in the finished steel segment and consistent material movement across key markets. Additionally, rising raw material costs and ongoing scarcity, coupled with firm global price benchmarks, are likely to provide underlying support to domestic steel prices.

Leave a Reply