- Slack procurement, dampened expectations weigh on longs

- Liquidity pressures, muted demand keep flats under pressure

- Air pollution restrictions may keep construction activity low

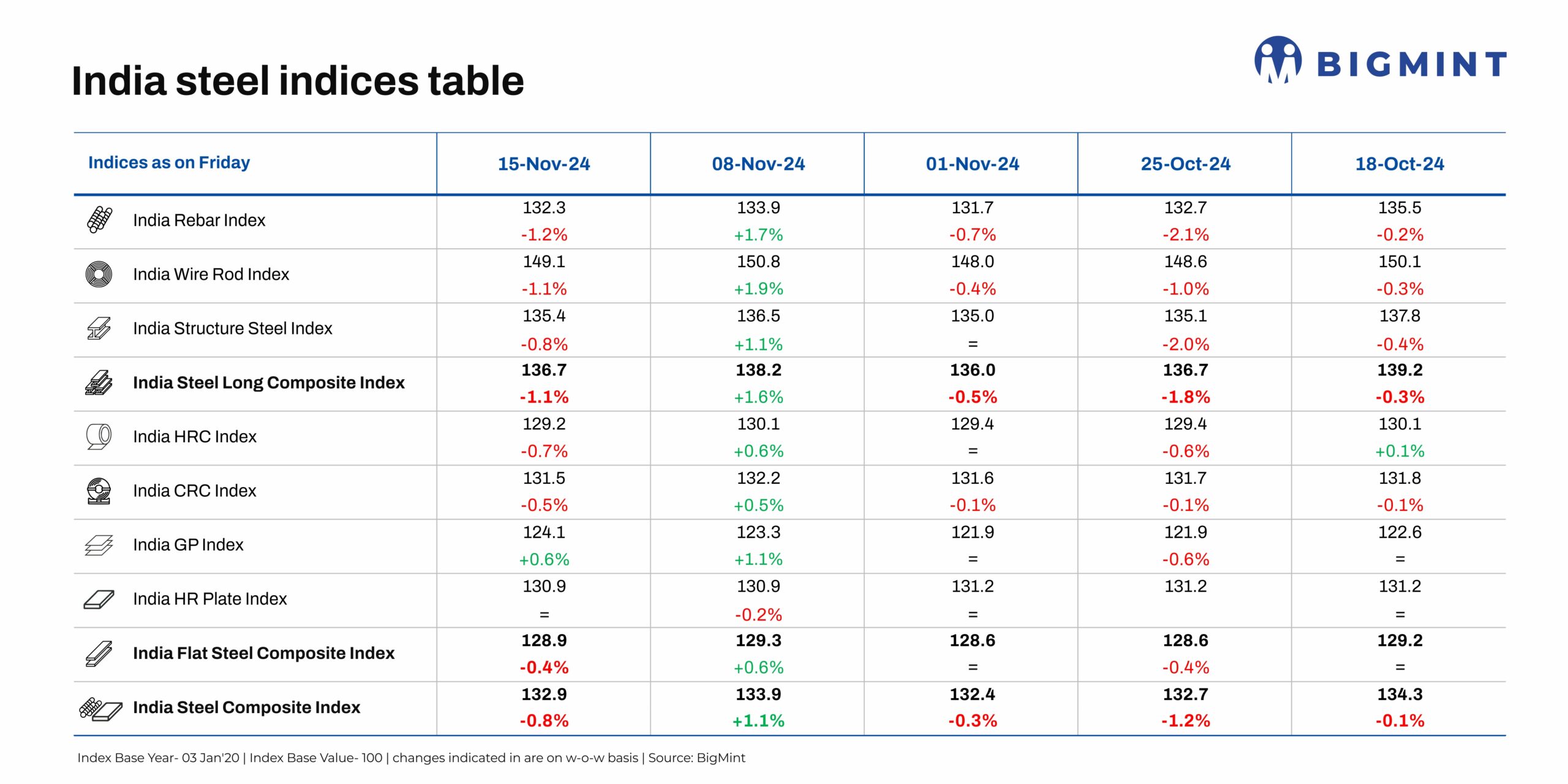

Morning Brief: Expectations of a post-Diwali recovery in steel prices continued to elude the market this week, with the BigMint India Composite Steel Index registering a 0.8% drop to 132.9 points on 15 November as against 133.9 seen on 8 November.

After tumbling for three weeks in a row, the index had closed in the green on 8 November, with a 1.1% increase. This latest assessment saw the index losing almost as much as it had gained last week.

Tags of both longs and flats fell – the former by a steep 1.1% and the latter by a modest 0.4%. The relative stability in the flats index offset a sharper fall in overall steel prices. While decent demand for galvanised plates propped up the flats index to a certain degree, the longs index contracted across all three components – rebars, wire rods, and structure steel.

Notably, the index has been languishing in the 130 zone since 12 July 2024.

Factors that impacted the index last week

Subdued demand knocks down BF rebar: Trade-level prices of blast furnace (BF) route rebars edged down by INR 200/tonne (t) ($2/t) w-o-w to INR 54,800/t ($649/t) exy-Mumbai, excluding 18% GST. The price decline can be attributed to some factors. One, was the slack procurement, as the expected post-Diwali pick-up in demand failed to materialise. Secondly, raw material prices went down this week, impacting BF-grade prices. BigMint’s Odisha iron ore fines Fe62% index dipped by INR 150/t ($2/t) w-o-w to INR 5,450/t ($65/t) ex-mines on 9 November. Miners relaxed offers to encourage trades, and the index closed at INR 5,350/t ($63/t) this week, with a drop of INR 100/t ($1/t) w-o-w.

However,in the project segment, prices hovered at around INR 54,000-55,000/t ($640-651/t) FOR Mumbai, stable w-o-w, amid steady demand.

That apart, the only source of support (for some markets) was a moderate supply constraint from a leading state-owned steel mill, which undertook a maintenance-related shutdown at one of its plants.

IF rebar feels inventory pressure: The induction furnace segment, which commands 65-70% share of the market, witnessed a decline in prices of INR 100-1,500/t ($1-18/t) w-o-w across regions, keeping BF-rebar tags depressed. Sources indicate that following pre-Diwali restocking, IF mills had raised prices, anticipating a surge in trade momentum. However, buyers resisted engaging at higher prices and resorted to need-based procurement. As a result, inventory idling time increased to 10-15 days, and manufacturers, under pressure to offload material, slashed list prices or offered discounts to liquidate material.

However, in a slight contrarian trend, prices in Mumbai edged up by INR 200/t ($2/t) w-o-w to INR 47,800/t ($566/t) exw, since IF mills kept their list prices steady following Diwali.

Polls, pollution impact infra activity: It is worth noting that the government has reportedly kept infrastructure projects on hold, with more of its attention directed to welfare projects given a series of state elections in the offing. Additionally, with air pollution and smog gripping north India, especially the Delhi-NCR region, infrastructure activities are expected to take a breather. The Delhi government has invoked the third phase of the Graded Response Action Plan (GRAP-3), which places an embargo on non-essential construction and demolition work. These factors also impacted IF and BF rebar prices.

Selective purchasing dents HRC prices: The flats index edged down as need-based procurement prevailed, amid a cautious market, characterised by subdued demand. Hot-rolled coil (HRC) prices in the trade segment fell by up to INR 500/t ($6/t) w-o-w to INR 48,000-50,300/t ($569-596/t). Parallelly, cold-rolled coil (CRC) prices slid by up to INR 700/t ($8/t) to INR 55,700-58,400/t ($660-692/t).

Some factors influenced this trend. One is the liquidity pressure that exacerbated the situation. Buyers were interested only in materials at the lower end of the price spectrum. As a result, traders reduced prices to perk up demand.

Secondly, rumours are floating that inventories at mills have reduced to 10-15% for the current month, although this could not be confirmed. While this may spur an uptick in prices in the near term, flagging demand in the market could pose a sizeable challenge.

Thirdly, imports are showing a declining trend for the time being, with cumulative arrivals for the month at 130,519 t till 11 November 2024. An additional 231,803 t are expected by the end of November. The total volume for October was 687,297 t, and for September, 776,835 t.

Exports remain a damp squib: Although BigMint’s HRC export index revived after a six-month-long break in late-October, following the resumption of offers to the Middle East, its performance has been nothing to write home about. The index this week mirrored the listlessness observed over the past week, with weak market sentiments keeping offers to Europe and the Middle East stable.

In the Middle East, competitive quotes from China ($530-535/t CFR UAE for grades S235 and S275) edged out Indian offers, which were stable at $560/t CFR. In Europe, tepid demand, ongoing anti-dumping investigations, and lower domestic prices kept offers range-bound at $590-595/t CFR Antwerp ($540-545/t FOB, east coast India). India has used up a mere 3% of its Q3CY’24 HRC quota for EU, even though half of the quarter has already passed.

Outlook

In the near term, prices may remain range-bound, as demand has yet to improve. Although winter is usually deemed the peak steel consumption season, demand has yet to improve. Construction activity may also be depressed due to air pollution-related restrictions and the government’s shift in attention to welfare programmes. Moreover, a possible increase in export tariffs from the US, coupled with a disappointing stimulus package from China, may intensify the export deluge and predatory pricing from China. Overseas demand may remain further muted as deep winter starts setting in the northern hemisphere and China.

India Steel Composite Index

The India Steel Composite Index is assessed on a weekly basis, every Friday at 18:30 IST, as per the weighted average prices based on manufacturing capacity and production.

BigMint considers the Composite Index with the base year being 3 January 2020 (financial year 2019-2020) and the base value as 100. The Composite Index does not give the absolute price but a trend of the market. The Indian steel industry is broadly classified into the BF-BOF and the electric/induction furnace routes. Keeping this broad classification in view, BigMint proposes to release the Composite Index by considering both production routes by manufacturing capacity and the production weighted method to compute the index for India.

Leave a Reply