- Fall in global prices impact flats

- Longs struggle with fiscal-year-end woes

- Lower raw material prices keep finished tags down

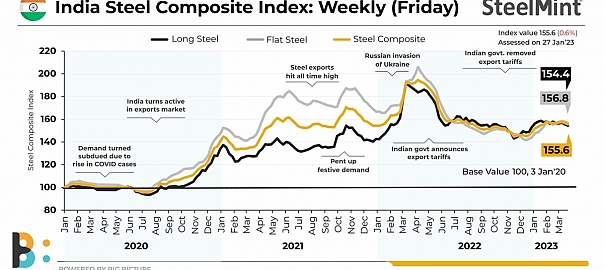

Morning Brief: The India Steel Composite Index hit a seven-week low. For the week ended 24 March, 2023, it fell another 0.6% to 155.60 points (156.70 points in the previous week).

The India Flat Steel Composite Index dipped by 0.74% to 156.80 points, against 158.00 points in the previous week. The India Long Steel Composite Index too edged down 0.68% to 154.40 (155.50) points w-o-w.

What factors are pulling down the index?

Global sentiments affect flats

Mixed trend in trade-level prices: Domestic prices in Mumbai and some of the other key markets remained stable at around INR 60,000-61,500/tonne (t). But other markets witnessed a decline this week amid the start of Ramzan and year-end liquidity issues.

Fall in Chinese steel prices: Global prices have been trending down. Although there was no clarity on prices earlier in the week, these weakened later. The Shanghai Futures Exchange (SHFE) HRC Futures showed a w-o-w drop of RMB 142/t or 3% to RMB 4,224/t on 25 March against RMB 4,366/t on 18 March. The SHFE Rebar Futures fell RMB 168/t or 4% to RMB 4,090/t against RMB 4,258/t in the same period.

Export market quiet: The export index fell marginally in the week under review by $4/t. No deals took place in this time-frame as the Middle East, which has been mainly captured in the export index, has been quiet because of the start of the Holy fasting month of Ramadan. Vietnam was happy to feed on domestic supplies despite the higher prices because of the shorter delivery time. Mills avoided the latter market, observing the low realizations it would fetch them.

Chinese offers have also turned weak and not many deals were reported as buyers moved to the sidelines, waiting to see if prices would sustain or fall further.

Global banking crisis impacts global sentiments: The global banking crisis is impacting global sentiments. The US banks — Silvergate, Silicon Valley Bank and Signature Bank, collapsed over a span of three weeks, taking the global banking community by surprise. In Europe, globally acclaimed Zurich-based Credit Suisse sent further shockwaves as it buckled down. Markets have become restrained because of inflation, high interest rates and liquidity fears.

Longs struggle with year-end lack of liquidity

Rebar prices slide: Demand for longs has been seeing a decline with the project segment well- stocked up over January-February. March, thus, forced mills to opt for price corrections. Traders resorted to discounts and rebates to lure back buyers. The weekend saw a slight increase in semis’ prices but marketmen said this was not enough to return to previous levels. The BF-route rebar, ex-Mumbai, fell w-o-w by INR 500/t. IF-route rebars, also ex-Mumbai, dropped by around INR 600/t. Over the last one month, IF-route rebar prices have eroded by INR 2,000/t in an overall dull market, dragging down BF-grades too.

Fiscal year-end slows down market: Buying usually slows down towards the financial year-end. As accounts books close, financial tightening is common. With March 31, 2023 signalling the end of financial year 2022-23 (FY23), lack of liquidity has taken the shine off the market.

Raw material prices drop: Prices of key raw materials retreated w-o-w amid falling global prices, impacting Indian finished rates. Chinese imported iron ore fines Fe62% have fallen almost $10/t w-o-w.

Domestic pellet and sponge iron prices also showed a downtrend, and so did coking coal. The pellet export index recently fell to a two-month low while sponge prices have also inched down by INR 300-400/t.

Coking coal FoB Hay Point Australia was down around $20/t w-o-w.

Outlook

SteelMint heard Indian primary mills are mulling another hike in offers for April sales of INR 1,000-1,500/t citing elevated raw material prices. A primary mill source informed SteelMint that coking coal and iron ore prices are still steep and that internationally offers, including China’s, are higher compared to India’s. “So, domestic steelmakers are still under pressure,” the source said.

In secondary sector, longs prices too may rise since the current levels are not sustainable or raw material prices should correct further, the source said.

The India Steel Composite Index

The India Steel Composite Index is assessed on a weekly basis: every Friday at 18:30 IST, as per the weighted average prices based on manufacturing capacity and production.

SteelMint considers the Composite Index with the base year being 3 January 2020 (financial year 2019-2020) and the base value as 100. The Composite Index does not give the absolute price but a trend of the market. The Indian steel industry is broadly classified into the BF-BOF and the electric/induction furnace routes. Keeping this broad classification in view, SteelMint proposes to release the Composite Index by considering both production routes by manufacturing capacity and the production weighted method to compute the index for India. For details click to view the methodology document.

Leave a Reply