- IF rebars rise amid demand spurt, cost push

- BF-route rebar prices rise on cue from IF mills

- Mills raise flat steel prices despite dull demand

- Short term looks range-bound as polls loom nearer

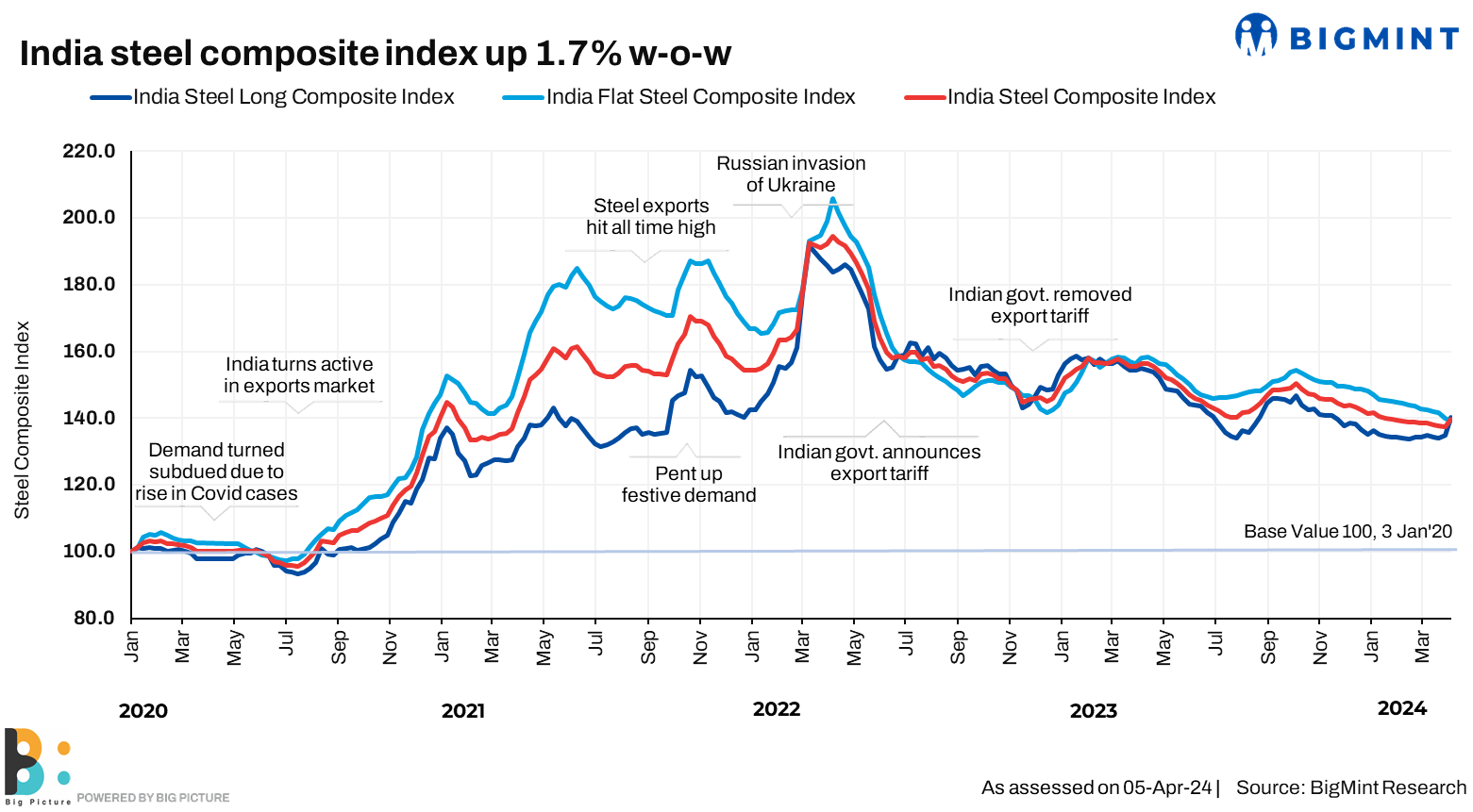

Morning Brief: Breaking out of months of range-bound movements, the BigMint India steel composite index rose to over a year high of 1.7% w-o-w, closing on 6 April at 139.8 points (137.5 points). Similar levels were last seen on 3 February, 2023. Longs fared slightly better although the flat steel index continued to be on the backfoot.

Factors that influenced the index last week

Longs were significantly aided by a spurt in demand and rise in raw material prices, especially in the induction furnace (IF) space.

IF rebar rises on cost, demand push: Prices of IF-grade rebar increased by around INR 1,000-3,900/t ($12-47/t) across regions amid improved demand and cost push from raw materials like billets and sponge iron. The improved demand for IF rebars can be attributed to two factors – 1) pre-election buying as the polls will extend from 19 April till 1 June, in seven phases. Post-which, the monsoons will set in. Thus, buyers have become somewhat proactive at this juncture. 2) A certain of panic buying took place as buyers feared prices may rise further.

Post-hike, trade reference prices of Fe 500 grade rebar was assessed at INR 46,400-46,800/t ($557-562/t) exw Raipur, INR 50,300-50,900/t ($604-611/t) exw-Jalna.

The BigMint billet index from Raipur rose INR 1,800/t ($22/t) w-o-w to INR 41,900/t ($503/t) while benchmark sponge prices in Raipur rose by INR 1,400/ ($17/t) w-o-w to INR 28,400/t ($341/t). Billets and sponge rose on the back of higher finished steel demand.

BF rebar prices rise on cue from IFs: On cue from induction furnace units, primary steel mills raised rebar prices by up to INR 1,000/t ($12/t) for early-April 2024 dispatches in order to maintain the gap with tier-2 players.

Trade-level prices of BF-route rebar also increased by INR 400-1,500/t ($5-18/t) w-o-w across key markets, propelled by the sharp increase in IF-route and primary mills’ prices. Demand in the traders’ market remained subdued during the week but prices were up by INR 700/t ($8/t) w-o-w to INR 53,400/t ($641/t) exy-Mumbai, exclusive of 18% GST.

In the projects segment, prices increased by INR 1,000/t w-o-w and are currently hovering at INR 51,000-51,500/t ($612-618/t) FOR Mumbai basis.

Mills raise flats prices but demand dull: Some of the primary steel mills raised list prices of hot rolled (HR) and cold rolled (CR) coils by INR 500/t ($6/t) for April sales. However, they extended the rebate of INR 1,500/t ($18/t) for March. Post-hike, list prices of HRCs stood at INR 53,500-54,000/t ($642-648/t) ex-Mumbai, while that of CRCs at INR 58,800-60,500/t ($706-725/t) ex-Mumbai for early-April 2024 sales.

Prices rose even as demand remained dull and buyers sustained their need-based buying pattern. Consequently, as per the BigMint bi-weekly benchmark evaluation on 2 April, trade-level HRC prices fell by INR 200/t ($2/t) to INR 51,800/t ($622/t) exy-Mumbai while CRCs remained stable at INR 61,100/t ($733/t) exy-Mumbai.

Exports dull amid fall in prices globally: The BigMint India HRC export index (for the Middle East and Vietnam) fell by $8/t w-o-w to $567/t FOB east coast India. Prices dropped amid sluggish global market sentiments and slow trade activities. China’s Shanghai Futures Exchange (SHFE) declined sharply by RMB 94/t ($13/t w-o-w while Vietnamese steel major Hoa Phat reduced domestic HRC prices by $40-45/t CIF HCMC. Plus, the offers to the Middle East remained flat w-o-w at $605-610/t because of Ramadan. Offers to Europe were also flat w-o-w at $590-600/t as the market there remained subdued in the post-Easter period. EU buyers are uncertain over safeguard duty measures.

Outlook

The market is likely to remain subdued in the near term as the general elections start rolling out from 19 April. Buyers will possibly move to the sidelines, and the current surge in procurement may resultantly drop. The buzz is the hike in prices effected last week may not get absorbed in the market. Thus, prices may be under pressure in the near term.

India Steel Composite Index

The India Steel Composite Index is assessed on a weekly basis, every Friday at 18:30 IST, as per the weighted average prices based on manufacturing capacity and production.

BigMint considers the Composite Index with the base year being 3 January 2020 (financial year 2019-2020) and the base value as 100. The Composite Index does not give the absolute price but a trend of the market. The Indian steel industry is broadly classified into the BF-BOF and the electric/induction furnace routes. Keeping this broad classification in view, BigMint proposes to release the Composite Index by considering both production routes by manufacturing capacity and the production weighted method to compute the index for India.