- BF rebar prices drop INR 100/t w-o-w

- HRC trade tags rangebound, CRC prices dip

- GST reforms expected to trigger higher steel demand

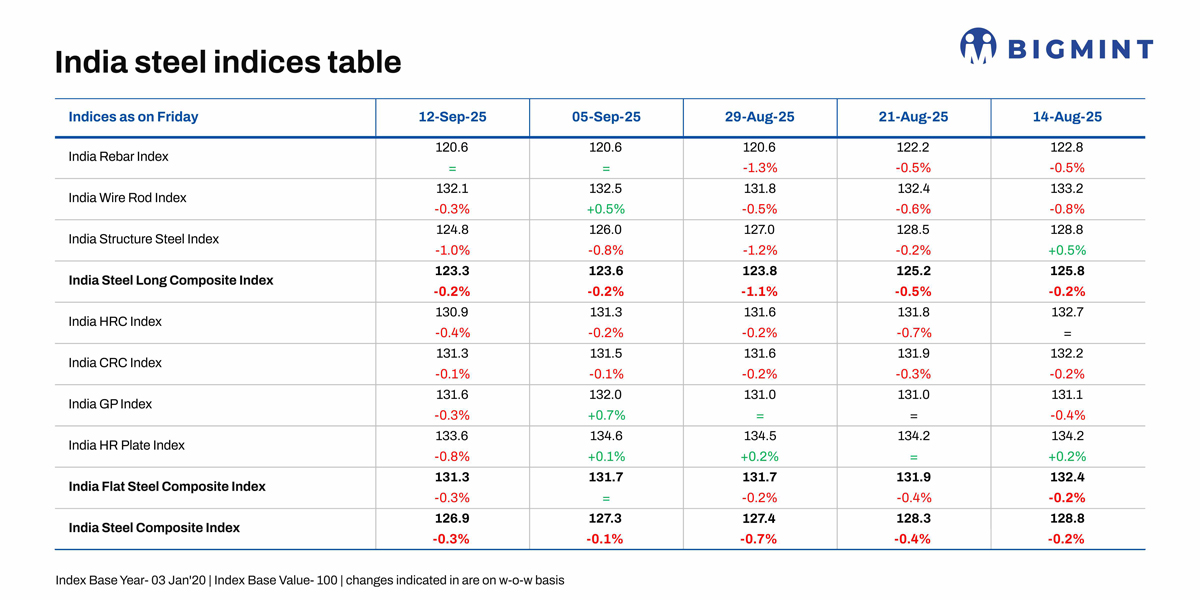

Morning Brief: BigMint’s India steel composite index, a barometer of the domestic market, continued to dip w-o-w in mid-September 2025, reaching close to five-year lows. The index, assessed at 126.9 points, is currently languishing at the lowest level since the pandemic period in early December 2020 – a 57-month low.

The composite index edged down by 0.3% w-o-w on 12 September as market conditions weakened with an extended monsoon weighing on trade sentiment. The longs and flats indices fell by 0.2-0.3% w-o-w but a revival in manufacturing activity in August and September and landmark tax policy announcements boosted market sentiment.

Highlights of price movements

HRC trade prices rangebound, CRC tags drop: Trade-level prices of hot-rolled coils (HRCs) remained rangebound w-o-w at INR 49,500/tonne (t) ($562/t), as of 5 September. Cold-rolled coil (CRC) prices saw a marginal dip of INR 100/t ($1/t) w-o-w to INR 56,700/t ($643/t) from INR 56,800/t ($645/t).

Leading Indian steel manufacturers officially raised prices of HRC and CRC by INR 750-1,000/t ($9-11/t) for September sales as compared to net sales prices in end-August. M-o-m, average trade-level prices of HRC rose by INR 500/t ($6/t) to INR 49,900/t ($566/t) in August against INR 49,400/t ($560/t) in July.

India’s Manufacturing PMI rose to 59.3 in August, the highest point in 17 years, showing strong growth in production and new orders. Moreover, demand was broad-based across capital and consumer goods, prompting firms to step up input buying and rebuild inventories.

Latest GST reforms, effective from 22 September, are expected to indirectly support flat steel prices, even though the steel tax rate remains unchanged. Market participants note that rate cuts in key end-user sectors – automotive, consumer durables, and construction – will likely spur downstream demand. In particular, the reduction of GST on automobiles from 28% to 18% is expected to ease cost pressures, stimulate production, and drive stronger steel consumption.

HRC imports edge down: India’s bulk imports of HRCs totalled 394,083 t in August, down 37% y-o-y from 624,179 t in August 2024. Imports also declined 19% m-o-m from 484,879 t in July. This clearly points to the impact of trade remedial measures.

South Korea, China, and Japan were the top bulk HRC exporters to India during the month, shipping 134,503 t, 102,957 t, and 78,864 t, respectively. Imports from South Korea declined 26% y-o-y, while volumes from China and Japan fell by 28% each.

Rebar prices remain under pressure: Trade-level BF rebar prices edged down by INR 100/t ($1/t) w-o-w to INR 47,200/t ($534/t) exy-Mumbai, as per BigMint’s assessment on 12 September. Prices are exclusive of GST at 18%. BF rebar trade prices dropped w-o-w across major markets, with the leading mills either increasing their discounts or reducing list prices due to subdued market sentiments.

“Construction and infrastructure activities have slowed down due to heavy monsoons, labour shortages, and logistics disruptions. Procurement remains minimal as overall market sentiment stays weak,” informed a buyer. Inventories at mills rose slightly by around 8% in mid-September compared with levels seen at the beginning of the month.

Although IF prices edged up in most key markets except Mumbai, bookings remained moderate, with buyers largely limiting purchases to immediate requirements while opting to wait and watch for further clarity. Current mill inventories are estimated at 12-14 days, while dispatches of previously booked material are moving smoothly. Market participants anticipate near-term volatility to persist.

Outlook

Seasonal slowdown in infrastructure and construction activities due to an extended monsoon is weighing on steel prices. However, policy reforms and surge in manufacturing demand ahead of the Dussehra-Diwali festive season is expected to provide a fillip to steel prices. As raw material prices remain firm, steel prices are unlikely to fall further.

On the global front, a potential FTA with the EU will be a major development for the domestic Tier-1 mills; however, weaker-than-expected peak construction demand in China and the prospect of softening steel prices are headwinds the domestic producers have to contend with.

India Steel Composite Index

The India Steel Composite Index is assessed on a weekly basis, every Friday at 18:30 IST, as per the weighted average prices based on manufacturing capacity and production.

BigMint considers the Composite Index with the base year being 3 January 2020 (financial year 2019-2020) and the base value as 100. The Composite Index does not give the absolute price but a trend of the market. The Indian steel industry is broadly classified into the BF-BOF and the electric/induction furnace routes. Keeping this broad classification in view, BigMint proposes to release the Composite Index by considering both production routes by manufacturing capacity and the production weighted method to compute the index for India.

Leave a Reply