- BF-origin rebar prices drop INR 1,500/t m-o-m

- Mills roll over HRC prices for June

- Seasonal slowdown grips steel market

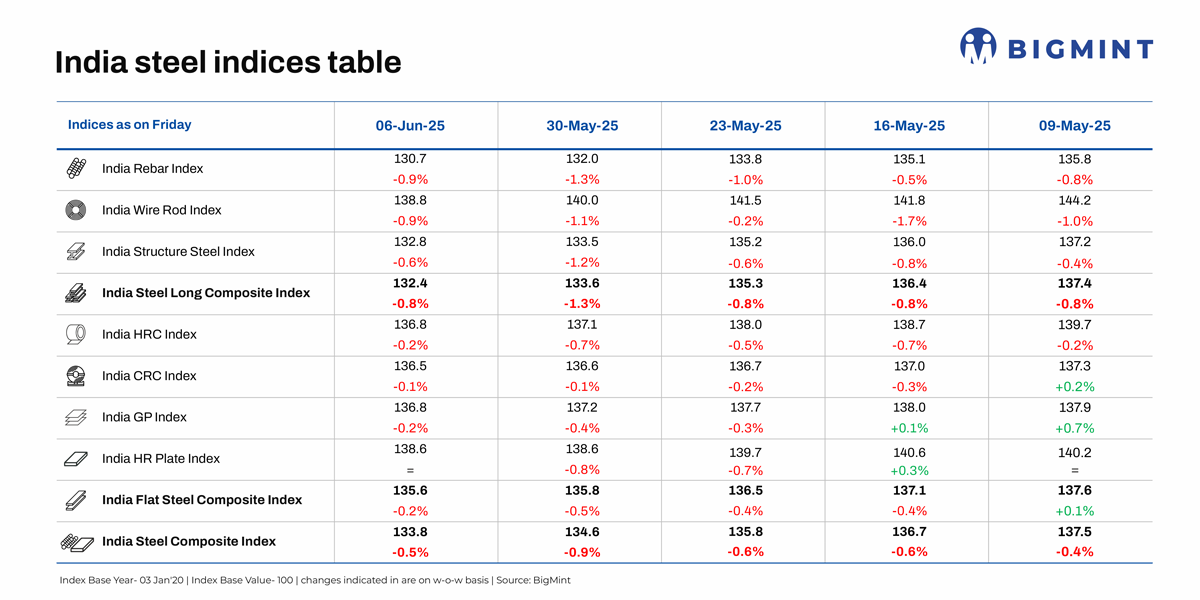

Morning Brief: Indian steel prices continued their downward trajectory in June 2025 after a lacklustre May amid global and domestic headwinds affecting the sector. BigMint’s India steel composite index – a barometer of the domestic steel market – fell by 0.5% w-o-w on 6 June, with long steel prices dropping more steeply than flats. While the flats composite index dropped 0.2% w-o-w, the longs index recorded a 0.8% decline.

In May, the flagship index had slipped by 2.7%, which indicates that the 12% provisional safeguard duty on imports of flat steel, which had come into force in mid-April, failed to have a sustained positive impact on the market amid global uncertainty and deterioration in steel prices.

Below are snapshots of steel price movements recorded last week.

Longs

Top mills cut rebar list prices: Indian Tier-1 mills reduced rebar list prices by up to INR 1,500/t ($17/t) for early-June deliveries as against prices prevailing in end-May. Post-revision, list prices were at INR 54,500-55,500/t ($635-646/t) on landed basis. Mills had offered discounts/rebates to augment sales in May.

Rebar inventories at Tier-1 mills increased by approximately 10% m-o-m in early-June, sources informed, due to sluggish sales in May, as declining prices and soft demand posed challenges for mills in securing new orders.

IF-rebar market weakens: IF-based rebar manufacturers responded to muted inquiries and slow trade activity by either rolling over list prices or offering discounts. As demand softened, especially in the monsoon-affected regions, inventory holding period increased to above 12 days by May-end. The market remained under pressure due to seasonal slowdown and cautious buying.

Rebar prices dropped by INR 1,600/t ($19/t) m-o-m to a monthly average of INR 47,800/t ($557/t) exw-Mumbai in May.

Flats

BF-based producers roll over HRC, CRC prices: Indian primary steel manufacturers, both the existing top mills and new entrants, have rolled over their list prices of hot-rolled coils (HRCs) and cold-rolled coils (CRCs) for June.

As of 6 June, BigMint’s benchmark assessment (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) decreased by INR 100/t ($2/t) w-o-w to INR 51,300/t ($620/t). CRC (IS513, Gr O, 0.9 mm/CTL) prices fell by INR 100/t ($1/t) w-o-w to INR 58,200/t ($703/t). These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

In the trade segment, the average monthly price of HRCs decreased by INR 600/t ($7/t) m-o-m to INR 51,400/t ($599/t) in May. CRCs saw a decline of INR 500/t ($6/t) to INR 58,400/t ($681/t).

The recent decline in steel prices can be traced to softening demand and the early arrival of monsoon which prompted market participants to reduce inventory levels by selling existing stocks. This proactive destocking was driven by expectations of decreased demand during the monsoon months. Labour shortages, driven by adverse weather conditions and agricultural work, also slowed down construction activity.

HRC export prices subdued: Indian mills are not actively offering to the Middle East due to competitive Chinese offers and higher domestic realisations. Meanwhile, Indian HRC export offers to Europe remained rangebound m-o-m. Subdued export market trends further pressured domestic flat steel prices even though imports of HRC and plates dropped in May.

Outlook

Indian steel prices are set to witness further decline in June, with sales volumes expected to be pressured by a continued slowdown in construction activity, liquidity shortfalls and slow payment recovery, as well as buyer resistance to prevailing prices. Parallelly, NMDC has trimmed iron ore offers by INR 150-160/t ($2/t). The downtrend is likely to extend to other commodities.

It is evident that the safeguard duty has been less effective than expected due to the global threat of import diversion to India as US tariffs spiral and trade uncertainties deepen. Market grapevine has it that the government is considering doubling the duty in order to prevent the influx of low-priced steel imports.

Nevertheless, gloomy domestic sentiment and deteriorating global steel prices point to a sustained seasonal downtrend ahead.

India Steel Composite Index

The India Steel Composite Index is assessed on a weekly basis, every Friday at 18:30 IST, as per the weighted average prices based on manufacturing capacity and production.

BigMint considers the Composite Index with the base year being 3 January 2020 (financial year 2019-2020) and the base value as 100. The Composite Index does not give the absolute price but a trend of the market. The Indian steel industry is broadly classified into the BF-BOF and the electric/induction furnace routes. Keeping this broad classification in view, BigMint proposes to release the Composite Index by considering both production routes by manufacturing capacity and the production weighted method to compute the index for India.

Leave a Reply