- Mills defer purchases, rely on existing inventories, semi-finished imports

- Imported offers remain firm, buyers prefer domestic supply amid high freights

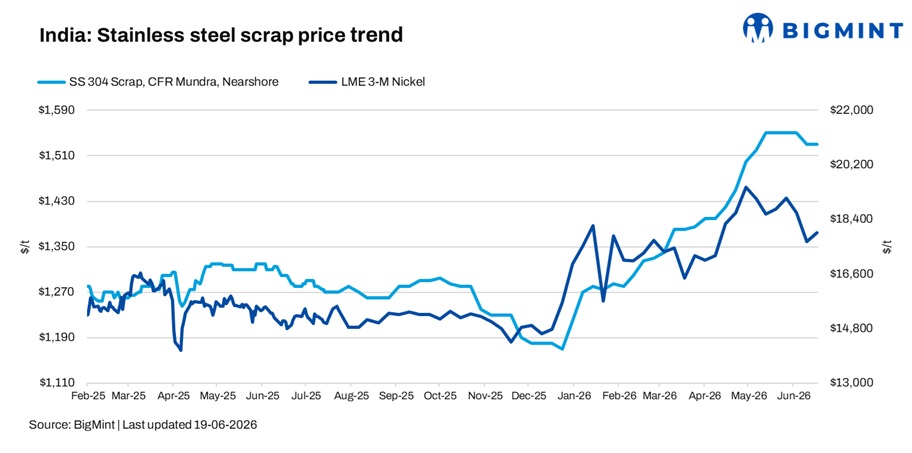

India’s stainless steel scrap market remained subdued in the week ended 19 June 2026, as weak finished stainless steel demand and uncertainty surrounding nickel prices kept buying activity restricted to immediate requirements. Market participants reported limited spot trading, with mills and traders maintaining a cautious approach despite stable imported scrap offers.

Domestic market under pressure

Buyers largely relied on existing inventories and avoided aggressive procurement, awaiting clearer direction on stainless steel and raw material prices. Domestic scrap continued to attract relatively better interest than imported material, as elevated freight costs and higher overseas offers reduced the competitiveness of imports.

Some mills also scaled back scrap purchases after securing semi-finished material. Market sources indicated that one mill booked around 10,000 t of stainless steel slabs from Indonesia, further reducing near-term scrap requirements and weighing on trading activity.

According to BigMint’s assessment, imported 304-grade stainless steel scrap remained unchanged w-o-w at $1,530/t CFR Nhava Sheva, while imported 316-grade scrap offers were steady at $2,945/t CFR India.

316 segment supported by tighter availability

In the domestic market, BigMint’s benchmark 304-grade stainless steel scrap price declined by INR 2,000/t w-o-w to INR 145,000/t DAP Delhi, reflecting weak buying sentiment and softer finished steel prices.

Meanwhile, domestic 316-grade scrap prices fell by INR 5,000/t w-o-w to INR 275,000/t DAP Delhi. The decline was largely attributed to softer ferro molybdenum prices, which were assessed at INR 4,115,000/t exw India, reducing cost-side support. However, relatively tight availability of 316-grade scrap prevented a sharper correction.

Outlook

India’s stainless steel scrap market is expected to remain cautious in the near term. Weaker nickel prices may continue to weigh on the 304-grade segment, while tight availability could lend some support to 316-grade scrap despite softer molybdenum prices. Nevertheless, weak finished steel demand, comfortable inventory levels, and requirement-based procurement are likely to limit significant price movements in the coming weeks.

Leave a Reply