- Need-based buying continues amid nickel volatility

- China’s scrap market under mild pressure

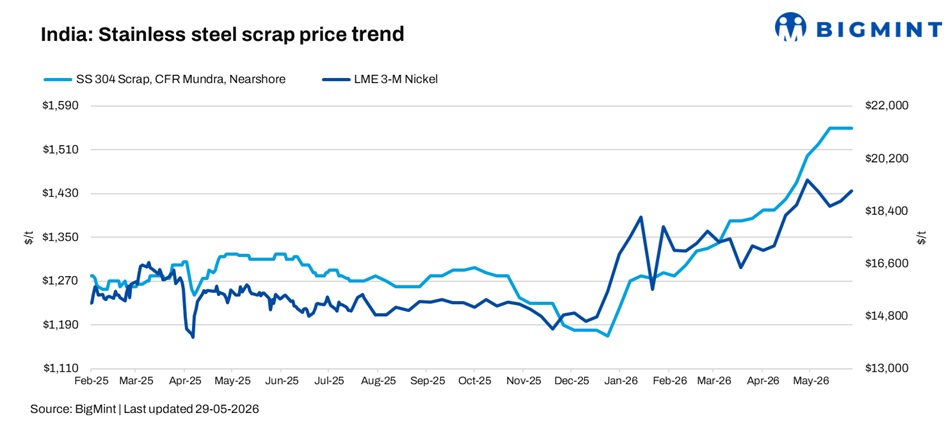

India’s stainless steel scrap market remained firm during the week ended 29 May’26, supported by elevated alloy costs and stronger import offers, although spot buying activity stayed cautious amid continued nickel price volatility. Market participants noted that procurement remained need-based due to persistent bid-offer disparities and uncertainty surrounding finished stainless steel demand.

Imported 304 stainless steel scrap offers were heard at around $1,540-1,550/t CFR Mundra, while workable bids remained lower at $1,500/t CFR India, reflecting cautious buyer sentiment and slower deal closures.

BigMint’s benchmark domestic 304 stainless steel scrap prices increased by INR 3,000/t w-o-w to INR 146,000/t DAP Delhi. Meanwhile, the 316-grade scrap segment remained stable at INR 275,000/t DAP Delhi amid limited spot availability and elevated ferro molybdenum prices currently stood at INR 4,100,000/t Exw-India, as per BigMint’s assessment.

Import offers also strengthened during the week, reflecting firm global scrap sentiment and higher stainless steel production costs internationally. BigMint’s imported 304 stainless steel scrap assessment remained steady at $1,550/t CFR Nhava Sheva, while imported 316 scrap prices increased by $10/t w-o-w to $2,910/t CFR India.

China scrap sentiment weakens w-o-w

China’s stainless steel scrap market remained under mild pressure this week as weakening downstream demand, slowing finished stainless steel transactions, and softer high-grade NPI momentum weighed on overall market sentiment. Although stainless steel futures edged up marginally, the gains failed to provide meaningful support to spot market activity amid cautious buying interest ahead of the seasonal demand slowdown. 304 stainless steel scrap prices in Shanghai declined by RMB 100/t w-o-w to around RMB 10,350/t ($1,435/t).

Market participants also highlighted that unresolved tax invoice issues and growing speculation surrounding potential steel mill production cuts in June further weakened procurement sentiment. Meanwhile, the rally in high-grade NPI prices lost momentum due to sluggish transactions, reducing raw material-side support for stainless steel scrap.

However, downside pressure remained limited as stainless steel scrap continued to maintain a clear cost advantage over NPI, with favourable melting economics providing a strong price floor. Overall, China’s stainless steel scrap market sentiment remained cautious-to-stable, with prices expected to fluctuate within a narrow range in the near term amid weak off-season demand and policy-related uncertainties.

Outlook

India’s stainless steel scrap market is expected to remain firm in the near term, supported by tight domestic availability, elevated alloy costs, and stronger import offers. However, continued volatility in LME nickel prices and cautious buying sentiment may limit aggressive spot transactions. Market participants will closely monitor developments in Indonesia’s nickel policies, Chinese stainless steel demand trends, and ferro molybdenum price movements for further market direction.

Leave a Reply