- Rising ferro alloy costs support prices as LME nickel futures fall

- Trade deals with US, EU foster optimism in pipes, tubes sector

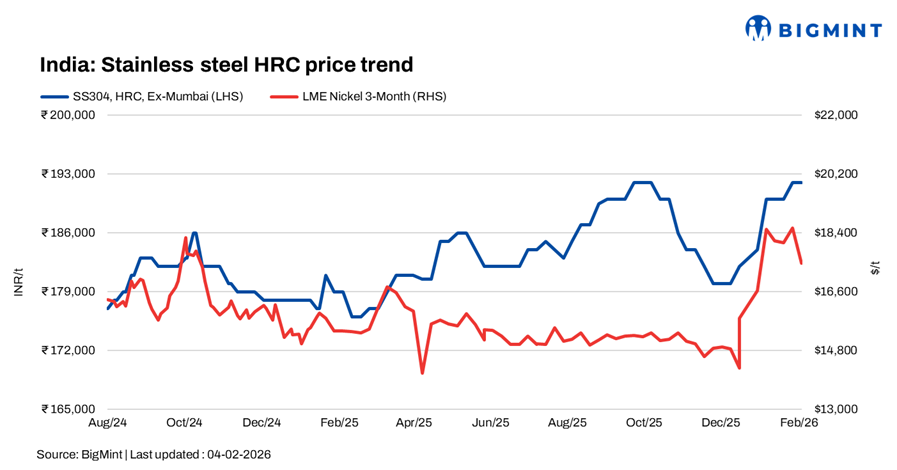

India’s stainless steel prices remained largely stable w-o-w on 4 February 2026 due to limited buying interest and heightened volatility in nickel prices. The appreciation of the Indian rupee further weighed on sentiment, keeping buyers cautious and largely in a wait-and-watch mode. However, stainless steel prices were supported by rising ferro alloys costs.

Finish flats

India’s stainless steel flat prices remained largely stable w-o-w. BigMint’s benchmark assessment pegged 304 HRC at INR 192,000/t ex-Mumbai, unchanged, while 316 HRC edged up by INR 3,000/t to INR 343,000/t w-o-w.

A stainless steel flat distributor said, “Demand is moderately strong, but imports are currently slow. Buyers are reluctant to lift large volumes. Some previously stuck material from Malaysia has been cleared, with importers reportedly paying 7.5% duty to release those cargoes.”

Another market participant noted, “The market is volatile, and demand remains very slow. However, with the India-US trade deal, more avenues are expected to open for the pipes and tubes sector, which could support flat steel demand going forward.”

Imported 304 CR wide-width coil offers from Vietnam were heard at $2,180-2,190/t CFR, while narrow-width CR was quoted at $2,110-2,120/t CFR.

In the global market, POSCO raised prices for February shipments of 300-series stainless steel by KRW 200,000/t ($137/t), citing sustained increases in raw material costs and a strong exchange rate that has lifted production expenses. The hike reflects a broader global trend, with Asian and European mills passing on higher nickel, ferro chrome, and molybdenum costs to protect margins. While alloy cost support is expected to keep Asian stainless steel prices firm in the near term, cautious buying and uneven downstream demand may cap further upside.

Finish longs

Finished longs prices remained largely unchanged during the week due to dull demand and limited buying interest. BigMint’s benchmark assessment for stainless steel 304L (25-100 mm) black round bars stood at INR 165,000/t ex-Mumbai, stable, while SS 316L black round bars were assessed at INR 280,000/t ex-Mumbai, unchanged.

A steel mill official said, “The market is highly volatile. Prices were rising over the past two weeks, but this week sentiment weakened as LME nickel corrected. However, with potential India-US and India-EU trade deals, we expect some positive impact by the end of the month, though clarity is still awaited.”

Another mill source added, “Export inquiries have improved slightly and are better than earlier weeks.”

Export offers for bright bars were heard at $2,300/t for 304 bright bars and $3,700-3,800/t for 316 bright bars on a CFR Turkiye and Taiwan basis. Freights were reported at around $50/t to Asia and $100/t to Europe.

Chinese stainless steel, NPI prices

In China, domestic stainless steel 304-grade CRC prices stood at RMB 14,950/t ($2,154/t) exw, while FOB tags for 304-grade CRC remained firm at $2,080/t. Indonesian FOB prices of nickel pig iron (NPI) (12-14%) were assessed at $135/t, while NPI (10-12%) stood at $134/t.

LME nickel prices

Benchmark three-month nickel prices on the London Metal Exchange (LME) stood at $17,540/t on 4 February, down around 5% w-o-w from $18,545/t. LME-registered nickel stocks were reported at 285,528 t, largely stable compared with 285,736 t in the previous week.

Raw material scenario

Ferro molybdenum: Indian ferro molybdenum prices rose by INR 86,500/t ($957/t) on 4 February compared with the assessment on 28 January, as sellers raised offers in line with firmer global cues and LME support, despite subdued end-user activity. As per BigMint’s assessment on 4 February, prices stood at INR 3,076,000/t ($34,032/t) exw-India, hovering at three-month highs last seen in mid-October 2025. Trading activity remained weak, with limited spot transactions as buyers resisted higher offers.

Ferro chrome: Indian high-carbon ferro chrome (HC 60%) prices increased by INR 4,600/t w-o-w to INR 124,600/t exw-Jajpur.

Ferro silicon: Indian ferro silicon (70%) prices rose by INR 1,400/t ($15/t) on 2 February compared with the 27 January assessment, following a m-o-m hike of INR 1,000/t ($11/t) in Bhutan’s February offers, set at INR 95,000/t ($1,051/t) exw. As per BigMint’s assessment, Indian ferro silicon prices were assessed at INR 95,000/t exw-Guwahati. Deals for around 1,500 t were concluded in the range of INR 92,500-95,500/t exw.

Ferrous scrap: India’s imported ferrous scrap market remained under pressure, with subdued buying interest amid comfortable domestic scrap availability and cautious mill sentiment. Market activity stayed thin, with mills procuring strictly on a need basis. Shredded scrap offers were heard at $355-365/t CFR, while HMS 80:20 was quoted around $330-340/t CFR from multiple origins.

Outlook

Stainless steel prices in India are expected to remain largely stable in the near term, with alloy cost support partially offset by weak demand and cautious buying sentiment. Movements in LME nickel, clarity on trade agreements, and export demand trends will be key factors shaping market direction in the coming weeks.

Leave a Reply