- Festive lull keeps India’s SS market muted

- Global outlook flat amid weak demand, oversupply

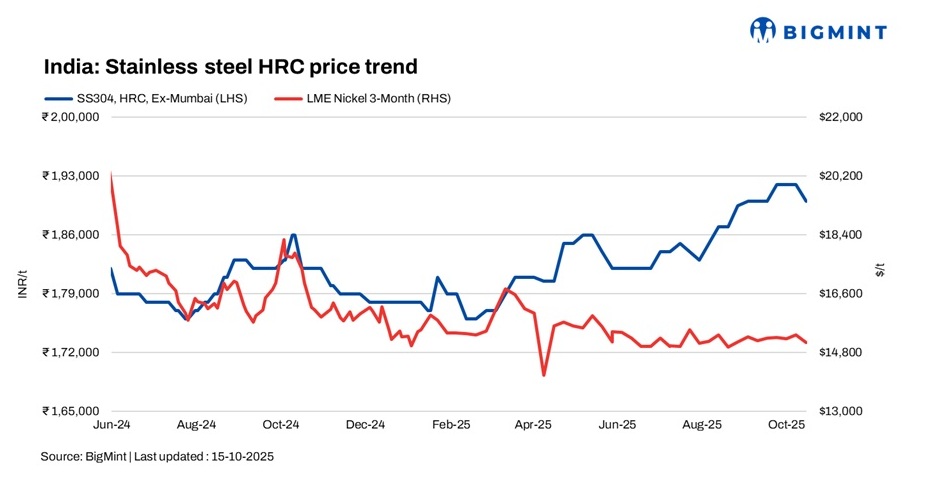

India’s stainless steel (SS) finished market remained largely inactive this week as festive holidays kept most participants away from trading. Consequently, BigMint’s weekly assessments for 304-series hot rolled coils (HRCs) at INR 190,000/t ex-Mumbai and 304L black round bars (25-100 mm) at INR 160,000/t stayed unchanged w-o-w. Similarly, 316-series hot rolled coils (HRCs) were assessed steady at INR 345,000/t, while cold rolled coils (CRCs) held firm at INR 350,000/t, both unchanged w-o-w.

Global market highlights

China’s stainless steel prices are expected to stay largely flat in Q4 amid weak demand, high inventories, and tariff concerns. Despite the traditional September-October peak, oversupply and soft consumption kept prices under pressure. Stainless output in September rose 3.4% m-o-m to 3.43 mnt, but demand lagged as buyers turned cautious after August restocking. For October, output may edge up 0.6% to 3.45 mnt, sustaining supply pressure. While nickel ore prices firmed slightly, NPI softened and ferrochrome imports jumped 40.7% m-o-m, ensuring ample supply. The looming 100% US tariff from November adds further uncertainty for Chinese exports.

Raw materials scenario

Ferro Molybdenum: Indian ferro molybdenum prices rose by INR 68,000 w-o-w to INR 3,100,000/t, driven by a surge in global market rates, particularly in China, coupled with higher raw material costs.

Ferro Chrome: Indian ferro chrome prices remained stable at INR 120,400/t exw-Jajpur w-o-w, with limited new offers post-OMC’s chrome ore auction as the market stayed largely inactive during the week. At the OMC auction on 17 October, around 83,100 t was sold out of 86,400 t offered. Bids increased by 0.4–18% (INR 40–5,550/t) for most grades, while some saw declines of 8–10% (INR 1,894–2,764/t) m-o-m. The overall uptick was supported by firmer ferro chrome prices and strong buying interest in Vedanta-FACOR’s recent auction.

Ferro silicon: Indian ferro silicon (70%) prices edged up by INR 1,700/t w-o-w, supported by strong export demand and tender obligations, which created a mild supply shortage and pushed offers higher.

Ferrous scrap: India’s imported scrap market remained subdued amid weak steel demand and tight liquidity, limiting mill buying interest. Festive holidays further slowed trade, as mills prioritized cash flow management and cost reduction. Imported shredded scrap was assessed at $355/t CFR India, and HMS 80:20 at $325/t, with most bids trailing offers by $5-10/t.

LME nickel tags remain stable w-o-w

At the time of reporting, three-month nickel prices on the London Metal Exchange (LME) were at $15,163/t, marking a marginal increase of $53/t from last week’s $15,110/t. Meanwhile, LME-registered nickel inventories rose to 250,878 t, up by 7,620 t from 243,258 t a week earlier.

Outlook

The stainless steel finished market is expected to stay subdued as festive holidays and weak buying interest keep trading activity muted during the Diwali period.

Leave a Reply