- Indonesian curbs continue to tighten global nickel supply

- Tsingshan’s recent price hike supports firm Indian prices

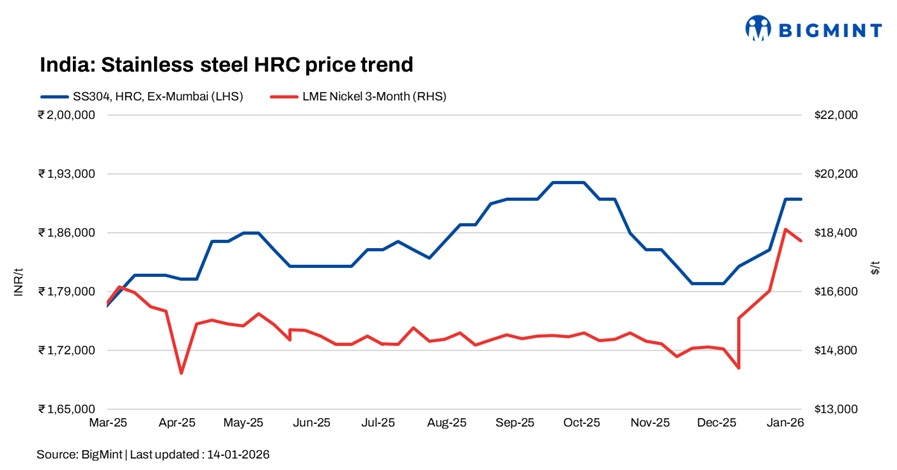

India’s stainless steel prices remained firm on 14 January 2026, supported by rising nickel costs and improving domestic demand, though trade slowed during the Makar Sankranti and Lohri holidays. Indonesian supply-side curbs continued to lift nickel costs, prompting mills to maintain higher price levels.

Finished flats prices remain firm

The finished flats segment remained firm on better domestic demand and elevated global prices. Tsingshan’s recent price hike further reinforced market sentiment, sources said. Higher nickel and ferro molybdenum costs, coupled with Indonesia’s production curbs, tightened supply and lifted production costs.

BigMint’s benchmark assessment for 304 hot-rolled coils (HRCs) was at INR 190,000/t ex-Mumbai, while 316 HRCs stood at INR 336,000/t, both steady w-o-w.

Indicative levels of imported 304 cold-rolled (CR) narrow coils were heard at around $1,960-1,980/t, and CR wide coils were heard at around $2,050-2,060/t CFR Vietnam.

Cost pressures support finished longs prices

The finished longs market, both domestic and export, remained active. According to mill sources, higher nickel prices and expectations of further cost escalation prompted mills to raise their purchase offers to secure adequate volumes at current market levels.

BigMint’s benchmark assessment for stainless steel 304L (25 to 100 mm) black round bars was at INR 160,000/t ex-Mumbai, up by INR 2,000/t. Meanwhile, SS 316L black round bars were at INR 278,000/t ex-Mumbai, up INR 3,000/t w-o-w.

Chinese stainless steel and NPI prices

In China, prices of domestic stainless steel 304-grade CRCs stood at RMB 14,400/t ($2,064/t) exw, while FOB tags of 304-grade CRCs were firm at $2,010/t. Indonesian FOB prices of nickel pig iron (NPI) (12-14%) were at $126/t, and NPI (10-12%) stood at $125/t.

LME nickel prices decline w-o-w

Benchmark three-month contract nickel prices on the London Metal Exchange (LME) were at $18,105/t on 14 January, down by 3.4% from $18,650/t in the previous week. Prices eased from recent highs, though they remained elevated amid tight supply due to Indonesian production curbs. LME-registered nickel stocks stood at 284,148 t, an 3.1% increase compared to 275,634 t in the previous week.

Raw material market overview

Ferro molybdenum: Indian ferro molybdenum prices increased by INR 50,000/t ($554/t) w-o-w. End-user demand was stable, leading to higher offers from sellers. Deals were also concluded at higher levels. As per BigMint’s assessment on 14 January, ferro molybdenum prices in India were at INR 2,940,000/t ($32,601/t) exw.

Ferro chrome: Indian high-carbon ferro chrome (HC60%) prices remained steady w-o-w at INR 105,700/t ($1,181/t) exw-Jajpur.

Ferro silicon: Indian ferro silicon (70%) prices remained unchanged w-o-w on 12 January. The price stability could be attributed to steady trading activity, as most deals were concluded at Bhutan’s announced prices for January, that is, INR 94,000/t ($1,042/t) exw.

Ferro silicon prices in India were at INR 94,000/t ($1,042/t) exw-Guwahati, as per BigMint’s assessment on 12 January. In Bhutan, prices slipped marginally by INR 100/t ($1/t) w-o-w to INR 93,900/t ($1,040/t) exw.

Ferrous scrap: India’s imported containerised ferrous scrap market remained subdued, with ample availability of cheaper domestic sponge iron and unworkable offer levels keeping buyers cautious despite some improvement in steel demand. UK-origin shredded scrap was offered at around $355-358/t CFR, while HMS 80:20 was indicated near $330-335/t CFR.

Outlook

Stainless steel prices are expected to stay firm next week, supported by elevated nickel and alloy costs. Overall, volatility in nickel prices and developments around Indonesian supply policies will remain key market drivers in the coming weeks.

Leave a Reply