- Mills cut prices amid weak downstream demand and falling raw material costs

- Inventory pressure and panic selling weigh on market sentiment

- China market remains subdued despite firm spot prices

India’s stainless steel market remained under pressure during the week ended 10 July 2026, as weak downstream demand, monsoon-related disruptions and volatile raw material prices continued to weigh on trading activity. Procurement remained largely hand-to-mouth across both flat and long product segments, while mills adopted a cautious approach amid subdued order bookings, liquidity constraints and rising inventory pressure.

Finished flats market under pressure

The finished flats segment witnessed slow trading activity as demand from key consuming sectors remained weak during the monsoon season. Market participants indicated that liquidity constraints continued to affect business activity, resulting in slower order conversion across the value chain. Procurement remained largely need-based, while mills increasingly relied on promotional discounts and price revisions to support order volumes.

Market sentiment weakened further due to elevated inventories and aggressive price competition. Participants noted that inventory pressure has triggered panic selling in the domestic market. At the same time, imported material remained largely uncompetitive despite firm international prices. Indicative prices for imported 304 cold-rolled coils were heard at $2,100-2,150/t, while JT-grade cold-rolled coils were indicated at $1,150-1,160/t. Market participants added that Chinese and European stainless steel prices remained firm, limiting import opportunities, particularly for 300-series products, while only limited volumes of 400-series material may remain viable due to the narrow price differential.

Market prices also softened following the extension of BIS certification for select stainless steel products until 31 March 2027, which provided continued relief to manufacturers while retaining compliance deadlines for stainless steel hot-rolled products and billets.

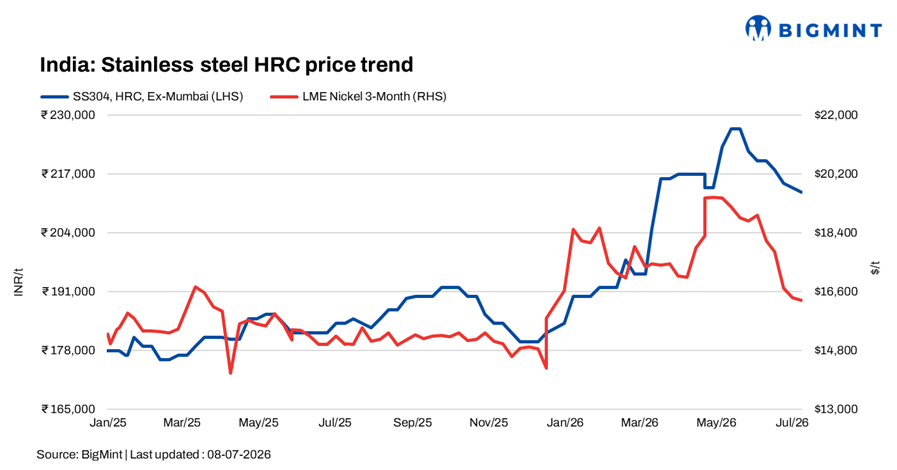

According to BigMint’s assessment, 304-grade hot-rolled coil (HRC) prices declined by INR 1,000/t w-o-w to INR 213,000/t ex-Mumbai, while 316-grade HRC prices fell by INR 5,000/t to INR 390,000/t ex-Mumbai.

Adding to the bearish sentiment, a leading domestic stainless steel producer reduced prices of HR and CR stainless steel coils effective 6 July, marking its first revision of the month. Prices of 304/304L HR and CR coils were lowered by INR 5,000/t, while 316/316L HR and CR coil prices were reduced by INR 7,000/t. Prices of 430-grade HR and CR coils declined by INR 3,000/t, whereas 200-series prices remained unchanged.

Finished longs market remains subdued

India’s stainless steel long products market remained weak during the week, with demand from construction and engineering sectors constrained by the monsoon season. Distributors remained cautious amid slow order inflows and continued to procure material only against immediate requirements.

BigMint’s benchmark assessment for 304L black round bars declined by INR 1,000/t to INR 187,000/t ex-Mumbai, while 316L black round bar prices fell by INR 3,000/t to INR 337,000/t ex-Mumbai.

Export enquiries also remained limited, with overseas buyers maintaining a wait-and-watch approach due to weak global demand and geopolitical uncertainties. Indicative export offers for 304 bright bars were heard at $2,350-2,400/t FOB India, while 316 bright bars were indicated at $4,150-4,200/t FOB India.

China market updates

China’s stainless steel market remained under pressure during the week as weaker futures and sluggish seasonal demand weighed on sentiment. In the spot market, 304/2B cold-rolled coil prices in Foshan stood at RMB 15,750/t. Despite weak futures, spot prices remained relatively firm as major steel mills maintained ex-works prices and inventory levels stayed manageable due to ongoing maintenance and production cuts.

However, the traditional off-season, subdued downstream demand and cautious buying sentiment kept transactions sluggish, with most buyers purchasing only for immediate requirements. Lower nickel raw material costs also improved steel mill margins, partially offsetting weak market fundamentals.

Outlook

India’s stainless steel market is expected to remain under pressure through July, with monsoon-related disruptions and weak downstream demand likely to keep procurement largely need-based. Mills may continue offering discounts and implementing selective price revisions to support order volumes, while elevated inventories and cautious sentiment are expected to limit any meaningful recovery. Market participants will closely monitor nickel price movements, inventory trends and post-monsoon demand indicators for clearer direction.

Leave a Reply