- Buyers continue need-based procurement only

- Higher molybdenum costs support 316 prices

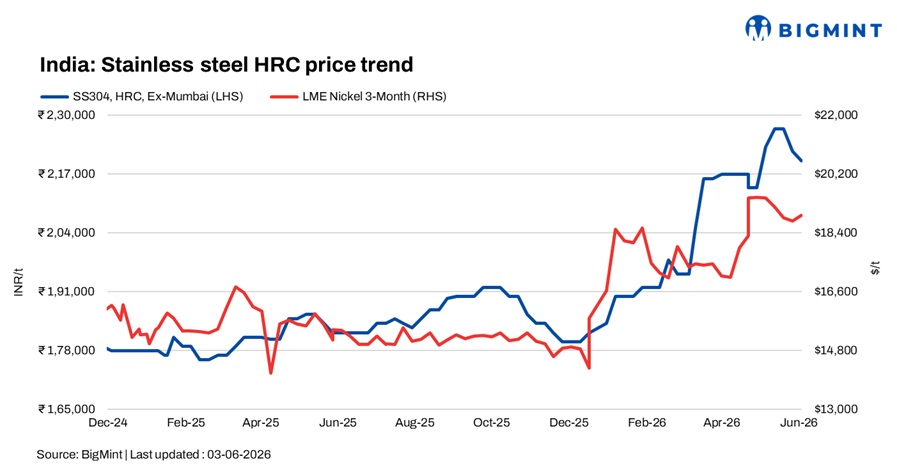

India’s stainless steel market remained subdued in the week ended 3 June 2026, as weak downstream consumption and cautious purchasing activity weighed on both flat and long product segments. Buyers largely limited procurement to immediate requirements amid uncertain demand visibility, while mills faced slower order inflows across domestic and export markets. Although rising nickel and alloy costs continued to provide underlying support to stainless steel values, the lack of meaningful demand recovery prevented producers from passing on higher input costs, keeping overall market sentiment under pressure.

Flat products under pressure

Stainless steel flat prices declined w-o-w amid weak buying interest and slow offtake from downstream sectors.

As per BigMint’s assessment, 304 HRC prices stood at around INR 220,000/t ex-Mumbai (down INR 2,000/t w-o-w), while 316 HRC prices were dropped by INR 3,000/t w-o-w at INR 405,000/t ex-Mumbai.

Import offers also remained largely stable. Market sources reported Vietnamese-origin 304 CRC offers at $2,298-2,300/t CFR India. Meanwhile, 1250 mm-width HR offers were heard at $2,267-2,277/t CFR India, while CR offers were reported at $2,319-2,350/t CFR India.

On the global front, Indonesia’s Tsingshan Holding Group raised 304-grade stainless steel export prices by $40/t effective 3 June. The increase was supported by continued uncertainty surrounding Indonesia’s nickel sector, the commencement of the country’s metal export control transition period from 1 June, and LME nickel prices crossing the $19,000/t mark, strengthening cost support across the stainless steel value chain.

Long products show mixed movement

India’s stainless steel longs market remained relatively quiet, with mills focusing on execution of existing orders. Export activity continued to underperform due to geopolitical uncertainties and container shortages, while domestic inquiries remained limited.

BigMint’s benchmark 304L black round bar prices declined by INR 5,000/t to INR 195,000/t ex-Mumbai. In contrast, 316L black round bar prices increased by INR 5,000/t to INR 347,000/t ex-Mumbai, supported by higher molybdenum costs.

In the export market, 304 bright bar offers were reported at $2,350-2,375/t FOB Nhava Sheva, while 316 bright bars were heard at $4,150-4,175/t FOB. For comparison, European domestic prices were assessed at $3,500-3,550/t for 304 bright bars and around $5,100/t for 316 bright bars.

Raw material scenario

Outlook

India’s stainless steel market is expected to remain muted in the near term. While elevated nickel prices, firm freight rates, and supportive global pricing may provide a floor to the market, weak downstream demand and cautious purchasing activity are likely to cap any significant upside in domestic stainless steel prices.

Leave a Reply