- Flats gain support from rising global prices

- LME nickel hits multi-month highs on supply concerns

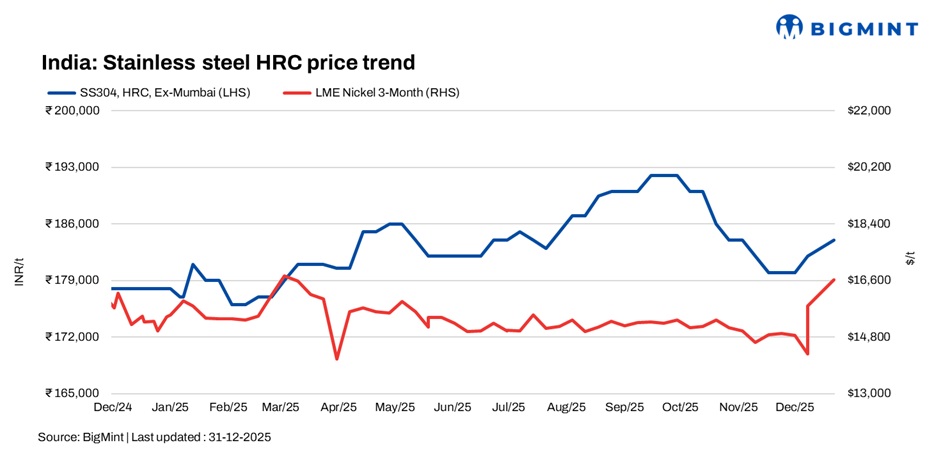

India’s stainless steel market recorded mixed movements across flats and longs during the week ended 31 December. While global price hikes and rising raw material costs offered selective support to flat products, the longs segment remained largely steady as weak domestic demand continued to cap buying interest.

Finished flats supported by global strength

India’s stainless steel flat market remained firm, underpinned by strengthening fundamentals and supportive global cues. Prices moved higher in line with global uptrends and rising nickel costs, with current levels nearing those seen in March 2025. Market participants attributed the firmness largely to supply-side constraints following production curbs in Indonesia and higher raw material costs.

Adding to the bullish sentiment, a leading stainless steel producer announced its second price hike in December, effective 30 December, citing firm cost-side pressures. The company raised 304/304L coils by INR 2,000/t, 316/316L coils by INR 3,000/t, JT HR coils by INR 1,000/t, and JT CR coils by INR 2,000/t. The revision followed a sharp rise in international nickel prices, with LME nickel currently hovering around $16,560/t, alongside supportive global market signals.

BigMint’s benchmark assessment for 304 HRC stood at INR 184,000/t ex-Mumbai, up INR 2,000/t w-o-w, while 316 HRC stood at INR 331,000/t, up INR 1,000/t w-o-w.

Finished longs market remains subdued

India’s stainless steel finished longs market remained muted, as weak domestic offtake continued to weigh on buying activity. Mills largely prioritised inventory liquidation over fresh production, keeping overall sentiment cautious.

Demand stayed soft, prompting most participants to remain in a wait-and-watch mode. Export activity was also slow amid the holiday season and subdued global cues, with mills focusing on clearing older export bookings rather than securing fresh orders. However, participants expect overseas enquiries and shipments to gradually improve over the next 7-8 days as international markets reopen and trading activity normalises.

BigMint’s benchmark assessments for stainless steel 304L (25 to 100 mm) black round bars was INR 153,000/t ex-Mumbai. Meanwhile, SS 316L black round bars were at INR 269,000/t ex-Mumbai, both up INR 1,000/t over the week.

Global sentiments

US finished stainless steel market sentiment remained weak toward the end of 2025, weighed down by slowing demand and cautious buying from service centres and industrial users. Mills reported softer order books, with some producers guiding for a 5-15% q-o-q drop in Q4 shipments amid economic uncertainty and year-end seasonality. Cold-rolled flat stainless consumption declined 4% y-o-y, and contract negotiations were delayed, reflecting subdued confidence. Overall, limited visibility on demand recovery continues to cap near-term optimism.

LME nickel rallies on Indonesia supply concerns

Nickel prices on the LME surged to a multi-month high during the week, reaching $16,720/t, marking a sharp 6.8% rise from $15,650/t assessed on 24 December. Current levels are close to those last seen in March 2025, driven largely by concerns over Indonesian supply curbs and tightening raw material availability.

Chinese stainless steel & NPI prices

In China, prices of domestic stainless steel 304-grade CRCs stood at RMB 13,300/t ($1,883/t) exw, while FOB tags of 304-grade CRCs were firm at $1,880/t.

Indonesian FOB prices of nickel pig iron (NPI) (8-12%) were at $117/t and NPI (10-14%) stood at $117/t.

Raw material market overview

Ferro molybdenum: Indian ferro molybdenum prices rose by INR 63,000/t ($201/t) w-o-w to INR 2,725,000/t ($30,331/t) ex-works as of 31 December, according to BigMint’s assessment. The increase was driven by strong domestic and global demand, along with higher LME molybdenum futures.

Ferro chrome: Indian high-carbon ferro chrome (HC60%) prices remained steady at INR 107,400/t ($1,181/t) exw-Jajpur.

Ferro silicon: Indian ferro silicon (70%) prices edged down slightly by INR 200/t ($2/t) as compared to the last assessment on 22 December. Prices didnt see any major fluctuation as the market was muted, awaiting offers from Bhutan for January 2026. Ferro silicon prices in India stood at INR 96,500/t ($1,073/t) exw-Guwahati, as per BigMints assessment on 29 December. However, in Bhutan, prices fell by INR 1,300/t ($14/t) w-o-w to INR 95,500/t ($1,062/t) exw.

Outlook

India’s stainless steel market is expected to remain firm in the near term, supported by strong global cues and elevated nickel prices. However, the longs segment may continue to face pressure, as weak domestic demand and slow export activity-particularly due to holidays in key importing regions are likely to limit any sharp upside in prices.

Leave a Reply