- Finished flats prices hold steady amid limited trading activity

- Imports from Vietnam, Thailand continue at competitive prices

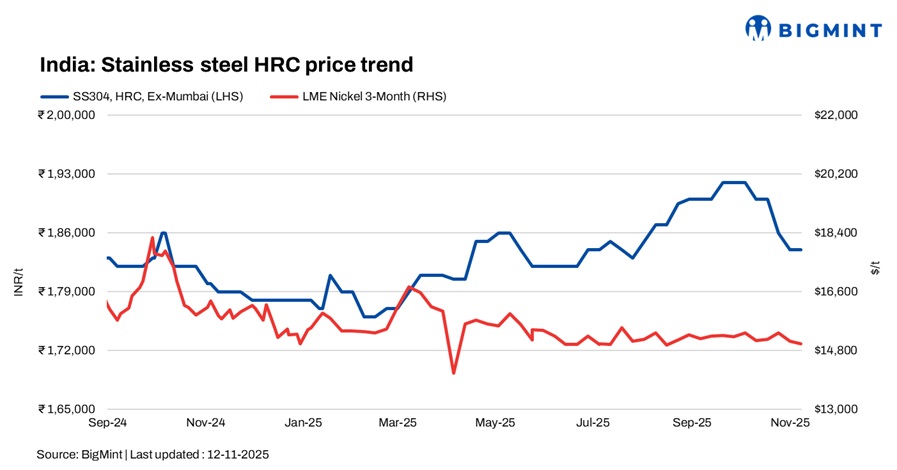

India’s domestic stainless steel market remained subdued this week amid persistent weak demand and market uncertainty. Finished flats prices held steady, while trade activity stayed limited, as participants waited for policy clarity, which is expected in mid-November.

Finished flats prices remain steady

BigMint’s benchmark assessments for stainless steel (304 series) hot-rolled coils (HRCs) stood at INR 184,000/tonne (t) ex-Mumbai, stable w-o-w.

Market activity was limited, with prices largely range-bound amid prevailing uncertainty. Participants waited for the upcoming policy announcement on BIS compliance for stainless steel imports, which is expected in mid-November. This is likely to provide clarity on future trade direction. Demand and supply dynamics remain stagnant for now.

A market source said, “There is speculation that Chinese imports may resume, potentially under BIS compliance, as Chinese offers remain 15-20% lower than other origins. Currently, imports from Vietnam and Thailand continue to dominate the market, with Vietnamese 304 cold-rolled (CR) indicative levels at $1,920-1,940/t, while JT CR was around $1,200/t and Thailand 304 CR was at $1,920-1,930/t.”

A trader noted, “Demand for the 300 series has weakened, leading to a steady decline in trade-level prices. Even though there is not excessive supply for this grade, subdued downstream activity and cautious end-user buying have kept prices under pressure, with most buyers avoiding fresh imports.”

Cheap imports pressure India’s stainless steel market

Despite strong domestic demand and steady growth, the Indian stainless steel finished market faces significant pressure from cheap imports, particularly from China, Vietnam, and Indonesia. These imports are priced at 5-10% below domestic levels, exacerbating price competition and affecting local producers. The industry has petitioned for anti-dumping duties, and an investigation by the Directorate General of Trade Remedies (DGTR) is underway, with hopes for a resolution that will restore fair market conditions. This ongoing import pressure remains a key risk factor amid otherwise positive domestic demand momentum.

Finished longs prices remain stable

BigMint’s benchmark assessments for stainless steel 304L (25 to 100 mm) black round bars were at INR 156,000/t, ex-Mumbai. Meanwhile, SS 316L black round bars were at INR 276,000/t, ex-Mumbai. Both were steady w-o-w.

A mill source stated, “Market conditions remain sluggish, which is typical for December. A major chunk of sales is export-oriented, and at present, we are primarily focused on fulfilling existing orders rather than taking on new ones.”

Indicative FOB prices for stainless steel longs were as follows: Indian 304 bright bars at $2,200-2,220/t and 316 bright bars at $3,700-3,730/t FOB Nhava Sheva.

Traders expect prices to soften further amid the prevailing trading lull, and softening molybdenum prices slightly eased cost pressures.

LME nickel tags steady w-o-w

At the time of reporting, three-month nickel prices on the London Metal Exchange (LME) stood at $15,005/t, range-bound compared to last week’s $15,100/t. Nickel stocks at LME-registered warehouses stood at 253,308 t, steady compared to 252,750 t in the previous week.

Chinese stainless steel, NPI prices

In China, prices of domestic stainless steel 304-grade CRCs stood at RMB 13,400/t ($1,882/t) exw, while FOB tags of 304-grade CRCs were firm at $1,870/t.

Chinese portside prices of nickel pig iron (NPI) (8-12%) were at RMB 909/t ($127/t). Meanwhile, Indonesian FOB prices of NPI (10-14%) stood at $113.51/t.

Raw materials scenario

Ferro molybdenum: Indian ferro molybdenum prices declined by INR 165,000/t ($1,863/t) as compared to the previous assessment on 5 November. Prices slipped w-o-w, as subdued end-user demand and declining global rates weighed on the market.

As per BigMint’s assessment on 12 November, ferro molybdenum prices in India stood at INR 2,775,000/t ($31,330/t) exw. Prices fell to a four-month low, last seen in early July 2025, as per data maintained with BigMint.

Ferro chrome: Indian high-carbon ferro chrome (HC60%) prices dropped by INR 1,500/t w-o-w to INR 116,500/t ($/t) exw-Jajpur.

Ferro silicon: Indian ferro silicon (70%) prices increased by INR 1,500/t ($17/t) as compared to the previous assessment on 3 November. Most sellers raised their offers due to a slight supply crunch, as some key suppliers in Bhutan ran out of stock. Additionally, active trades were concluded, which boosted sellers’ confidence. As per BigMint’s assessment on 10 November, ferro silicon prices in India were at INR 89,500/t ($1,009/t) exw-Guwahati. In Bhutan as well, prices increased by INR 1,000/t ($11/t) w-o-w to INR 89,000/t ($1,003/t) exw.

Ferrous scrap: India’s imported ferrous scrap market remained weak, as mills limited bookings amid sluggish steel demand, tight liquidity, and ample domestic supply. Shredded scrap offers hovered at $350-355/t and HMS 80:20 at $325-330/t CFR Chennai, but workable levels were lower around $315-320/t. Overall, subdued sentiment and sufficient domestic alternatives kept import activity muted.

Outlook

In the near term, the stainless steel market is likely to remain cautious, with limited demand recovery expected until policy clarity emerges. Market participants expect continued price pressure amid sufficient inventories, import competition, and slow downstream offtake.

Leave a Reply