- Finished longs demand remains weak amid limited trading

- Chinese supplies limited due to BIS certification constraints

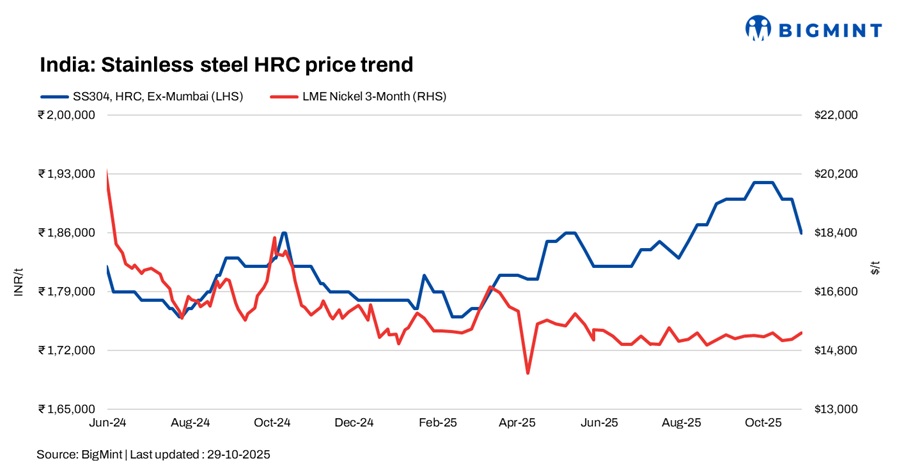

India’s stainless steel market witnessed a downtrend this week post Diwali holidays as the market has still not picked up tempo. BigMint’s weekly assessments for 304-series hot rolled coils (HRCs) dropped by INR 4,000/t to INR 186,000/t ex-Mumbai and 304L black round bars (25-100 mm) at INR 157,000/t fell INR 3,000/t w-o-w. Similarly, 316-series hot rolled coils (HRCs) were assessed at INR 343,000/t, while cold rolled coils (CRCs) stood at INR 348,000/t, both down by INR 2,000/t w-o-w.

Market scenario

Finished longs demand remains muted, with very limited trade activity reported in the market. Overall sales are dull, and buying sentiment continues to be weak. In Gujarat, market activity is particularly sluggish, as regular operations have yet to resume and no significant transactions have been noted in the current trading environment, market participants noted.

A mill source stated, “Finished flats demand in the market remains stable, though prices have not shown any significant upward movement. Imports from Vietnam are active, with Vietnam offers currently higher than Chinese material. However, Chinese supplies are largely absent due to the lack of BIS certification, which continues to restrict inflows. It is worth noting that Vietnamese pricing trends are still influenced by China, where prices have remained largely stable. Ocean freight costs have increased, now hovering around $1,400-1,500 for 20ft container.”

LME nickel tags edge high w-o-w

At the time of reporting, three-month nickel prices on the London Metal Exchange (LME) stood at $15,355/t, up by $200/t compared to last week’s $15150/t. Nickel stocks at LME-registered warehouses stood at 251,436 t, up slightly compared to 250,878 t t in the previous week.

Chinese stainless steel, NPI prices

In China, prices of domestic stainless steel 304-grade CRCs stood at RMB 13,550/t ($1,908/t) exw, while FOB tags of 304-grade CRCs were firm at $1,900/t.

Chinese portside prices of nickel pig iron (NPI) (8-12%) remained firm w-o-w at RMB 925/t ($130/t). Meanwhile, Indonesian FOB prices of NPI (10-12%) stood at $115.15/t.

Raw materials scenario

Ferro molybdenum: Indian ferro molybdenum prices declined over the week by INR 100,000/t ($1,134/t) compared to the previous assessment on 24 October. The drop was mainly driven by weak demand and sluggish consumption in the stainless-steel sector.

According to BigMint’s assessment on 29 October, ferro molybdenum prices in India stood at INR 2,950,000/t ($33,448/t) exw. Around 30 t of material were traded last week within the price range of INR 2,920,000 – 3,175,000/t ($33,108-35,994/t) exw.

Ferrous scrap: India’s imported scrap market stayed weak and largely inactive this week, weighed down by regional holidays and a persistent bid-offer gap. Mills avoided fresh bookings amid falling DRI prices and sluggish finished steel demand. Shredded scrap was heard at $350-355/t CFR, while HMS traded around $315-320/t, and PNS hovered near $355-360/t. Limited arrivals and cautious sentiment kept trading muted, with participants seeing little chance of a quick recovery despite some signs of stability in other Asian markets.

Ferro chrome: Indian high-carbon ferro chrome (HC60%) prices dropped by INR 200/t w-o-w to INR 120,200/t ($/t) exw-Jajpur.

Ferro silicon: Indian ferro silicon (70%) prices saw a decline of INR 1,600/t ($18/t) as compared to the previous assessment on 17 October. With limited inquiries and few bulk deals at lower rates, overall price levels in the market moved lower.

As per BigMint’s assessment on 27 October, ferro silicon prices in India were INR 87,100/t ($987/t) exw-Guwahati. In Bhutan, it came down by INR 900/t ($10/t) w-o-w to INR 87,600/t ($992/t) exw.

Outlook

The stainless steel market is projected to remain under pressure in the near term due to continued weak demand and slow sales.

Leave a Reply