- Weak demand and US tariff concerns persist

- Project-based demand expected to rebound post-March

In the domestic stainless steel market, prices of finished flat products remained steady w-o-w, while long product prices declined due to weak demand following the budget announcement and concerns over Trump tariffs. Overall, trade activity remained at low to moderate levels for the week.

LME nickel prices remain firm

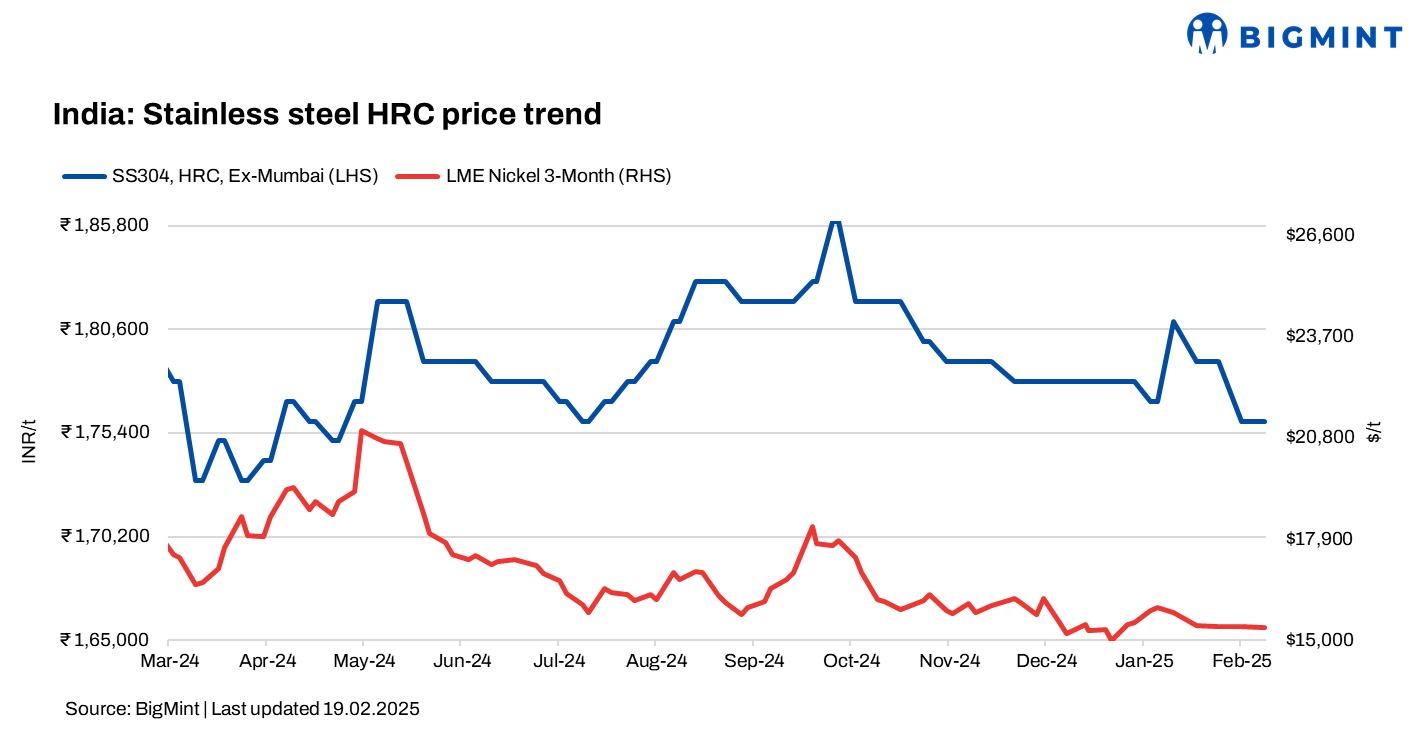

At the time of reporting, three-month London Metal Exchange (LME) nickel prices stood at $15,325/tonne (t), relatively stable given last week’s $15,355/t. Nickel stocks in LME-registered warehouses inched up by 7% to 189,516 t compared to 176,946 t in the previous week.

Finished flats range-bound w-o-w

BigMint’s benchmark assessment for stainless steel (304 series) hot-rolled coils (HRCs) stood at INR 176,000/t ex-Mumbai, steady w-o-w. Similarly, SS 316 HRCs were unchanged w-o-w at INR 320,000-322,000/t ex-Mumbai.

A mill source mentioned, “With the Holi festival approaching and the financial year-end just around the corner, there’s limited optimism for price hikes in the near term. As a result, the market is likely to remain stable, with no significant price changes expected until mid-April.”

The current demand for finished steel is exceptionally weak, particularly 316 grade material is seeing less inquiries in the market. Meanwhile, the demand for 200 series and 400 series are comparatively heard to be better.

Finished longs fall w-o-w

Prices of long products have fallen mainly due to weak domestic demand. While there are concerns about the US tariffs, particularly regarding exports to the US, it appears that their impact may not be lasting as per market participants.

BigMint’s assessment for SS 304L (25-100 mm) black round bars stood at INR 160,000/t ex-Mumbai, down by INR 2,000/t w-o-w.

Meanwhile, SS 316L black round bars stood at INR 269,000-271,000/t ex-Mumbai. Prices of SS 316L bright bars stood at INR 287,000-289,000/t ex-Mumbai, down by INR 2,000/t w-o-w.

A trader source informed BigMint, “The “Trump effect” has caused some short-term concerns in India, but its impact is expected to be temporary. The primary factors driving the market remain the LME and nickel prices. Looking ahead, there is optimism for a rebound in project-based demand after March, which could bring a more balanced market trend. Despite Trump’s duty announcement, exports have not been significantly affected as of now, with finished steel exports continuing smoothly. However, domestic market demand remains sluggish.”

SS 304 wire rods (5-16 mm) in Mumbai were recorded at INR 154,000-156,000/t, stable w-o-w.

China market

In China, domestic stainless steel prices for 304-grade CRCs stood at RMB 13,750/t ($1,887/t) exw, steady w-o-w, while FOB prices of 304-grade CRCs were at $1,890/t.

Chinese portside cargo prices for NPI (grade 13%>Ni>10%) remained stable w-o-w at RMB 960/t ($131/t). Meanwhile, FOB prices for NPI (grade 13%>Ni>10%) stood at $115/t, down by $1/t compared to the previous week.

Freight rates for small handysize vessels were as follows: from Bahudopi (Indonesia) to Ningde (China) at $20/t, from Weda to Tianjin at $24/t, and from Weda to Ningde at $22/t.

Raw materials overview

Ferro molybdenum: Indian ferro molybdenum prices witnessed an increase of INR 21,200/t ($244/t) w-o-w as compared to the previous assessment on 12 January. Prices have increased on a w-o-w basis, mainly driven by a rise in inquiries and a slight uptick in the global market.

As per BigMint’s assessment on 5 February, ferro molybdenum prices in India were at INR 2,560,000/t ($29,464/t) exw on a 60% pro rata basis.

Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si:4%) prices experienced an uptick of INR 1,000/t ($12/t) as compared to the previous assessment on 12 February. Most market participants were in a wait-and-watch mode ahead of the chrome ore auction from the Odisha Mining Corporation (OMC). Hence, sellers offered a limited volume in the market.

As per BigMint’s assessment on 19 February, Indian high-carbon ferro chrome (HC60%, Si:4%) prices were at INR 99,500/t ($1,145/t) exw-Jajpur.

Outlook

In the short term, the market is expected to remain range-bound with limited activity. Prices are likely to stay stable, as demand for stainless steel finished materials is not anticipated to see significant growth.

Leave a Reply