- LME nickel prices increase marginally w-o-w

- Secondary mills operating at lower capacities

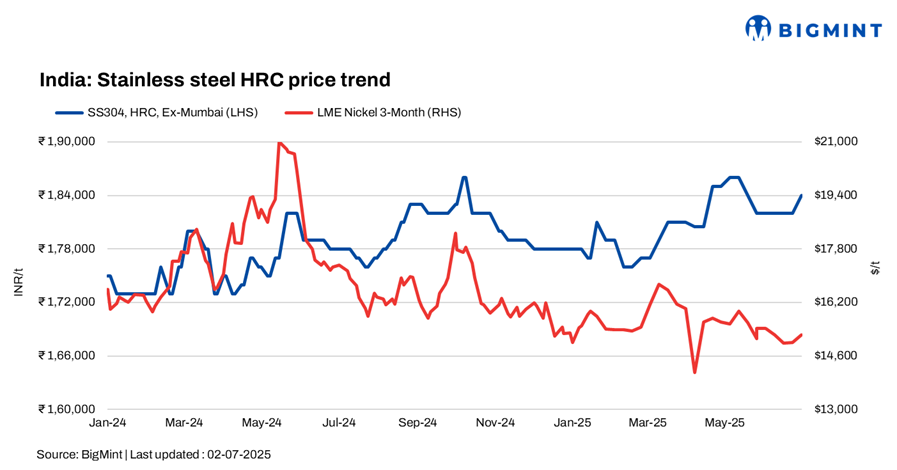

India’s stainless steel (SS) finished flats and longs prices showed a slight uptick w-o-w amid moderate demand. Meanwhile, LME nickel prices also inched up w-o-w.

BigMint’s benchmark assessment for stainless steel 304 series hot-rolled coils (HRCs) hovered at 184,000/tonne (t) up by INR 2,000/t, while 304L (25-100 mm) black round bars stood at INR 158,000/t, up by INR 1,000/t, both ex-Mumbai.

LME nickel up, Asian NPI remain steady w-o-w

At the time of reporting, three-month nickel prices on the London Metal Exchange (LME) stood at $15,265/t, showing an uptrend from last week’s $15,000/t. Nickel stocks in LME-registered warehouses stood at 203,886 t, range-bound compared to 204,120 t in the previous week.

Chinese portside prices of nickel pig iron (NPI) (grade 13%>Ni>10%) stood at RMB 915/t ($129/t). Meanwhile, Indonesian FOB prices of NPI (grade 13%>Ni>10%) stood at $110/t. Both were steady w-o-w.

Market insights

According to a market participant, “Buying activity remained subdued over the past week in the longs segment, with no significant trade volumes recorded. Secondary mills are still under pressure, operating at just 60-70% of their production capacity due to tepid demand and cautious buying.”

Although infrastructure development is moving forward and offering some support to the market, its slow pace continues to restrict a swift recovery in demand.

Additionally, as per BigMint’s assessment, SS 316 HRCs stood at INR 327,000/t and 316 cold-rolled coils (CRCs) at INR 335,000/t ex-Mumbai, both up by INR 2,000/t w-o-w.

Another source observed, “There is currently no demand for finished material in the market, largely due to the ongoing monsoon season. Significant movement is not anticipated until August.”

As per BigMint’s assessment, SS 316L black round bars stood at INR 269,000/t, while 316L (25-100 mm) bright bars were at INR 286,000-287,000/t, both ex-Mumbai. Additionally, SS 304 (5-16 mm) wire rods stood at INR 156,000/t ex-Mumbai.

Chinese stainless steel prices steady

In China, prices of domestic stainless steel 304-grade cold-rolled coils (CRCs) stood at RMB 13,450/t ($1,874/t) exw, stable w-o-w, while FOB tags of 304-grade CRCs were stable at $1,910/t.

Raw material scenario

Ferro molybdenum: Indian ferro molybdenum prices increased by INR 26,000/t ($303/t) as compared to the previous assessment on 25 June. Prices edged up amid regular domestic trades, while prices on the LME were largely stable.

Ferro molybdenum prices in India were at INR 2,700,000/t ($31,497/t) exw-India, as per BigMint’s assessment on 2 July. Trades for around 60 t were concluded in the assessment window within the price range of INR 2,650,000-2,750,000/t ($30,913-32,080/t) exw.

Ferro chrome: Indian high-carbon ferro chrome (HC60%, Si:4%) prices were at INR 99,800/t ($1,164/t) exw-Jajpur, dipping by INR 300/t w-o-w.

Vedanta-Ferro Alloys Corporation Ltd (FACOR) has scheduled an auction for high-carbon (HC) ferro chrome (10-150 mm) on 2 July. At the previous auction on 23 June, the bigger lot of 10-150 mm fetched an H1 price of INR 99,200/t ($1,157/t) exw. BigMint assessed ferro chrome (HC 60%, 10-150 mm) prices at INR 100,000/t ($1,166/t) exw-Jajpur on 27 June.

Ferro silicon: Indian ferro silicon (70%) prices were down slightly by INR 200/t ($2/t) in comparison with the last assessment on 23 June. Prices were steady, as the market did not witness any major movements, given that Bhutan’s new offers will be announced soon.

Ferro silicon prices in India were at INR 88,400/t ($1,033/t) exw-Guwahati on 30 June. In Bhutan, prices inched down by INR 200/t ($2/t) w-o-w to INR 88,000/t ($1,028/t) exw. Deals for around 1,500 t were finalised last week in both regions within the price range INR 88,000-89,000/t ($1,028-1,040/t) exw.

Ferrous scrap: India’s imported scrap market remained sluggish, weighed down by weak steel demand, monsoon-related disruptions, and the availability of cheaper domestic alternatives such as sponge iron and local scrap.

Shredded offers hovered at around $358-362/t CFR Nhava Sheva. Most bids were lower, in the range of $355-360/t, while HMS 80:20 remained largely stable at $333/t.

Market participants expect sluggish scrap demand to persist through July, unless iron ore prices or steel demand rebound. Buyers and sellers remain cautious amid weak steel sales and slow construction, while cheaper domestic scrap and steady rebar prices keep import interest low.

Outlook

Stainless steel prices are likely to stay range-bound amid weak demand and cautious buying. Market sentiment may improve post-monsoon with the expected recovery in construction activity.

Leave a Reply