- LNG supply curbs impact mills’ rolling operations

- Freights surge across Southeast Asian trade routes

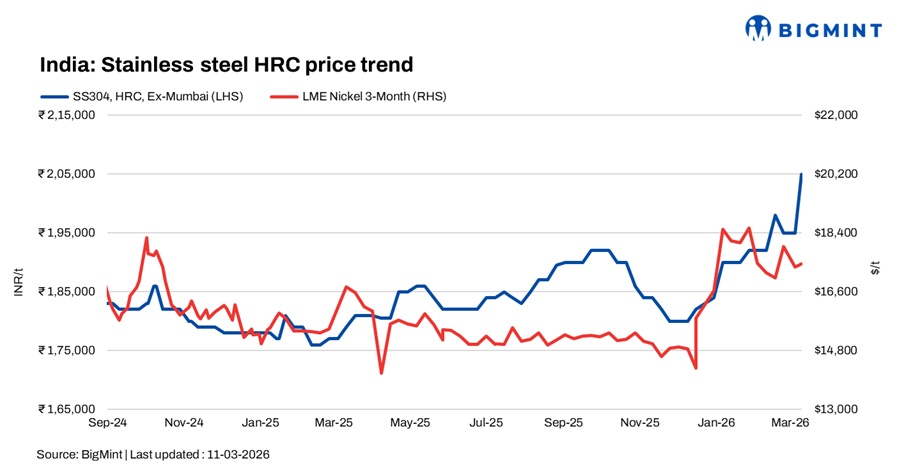

India’s stainless steel finished product prices increased w-o-w on 11 March 2026 as escalating US-Iran conflict in the Middle East triggered energy supply disruptions and logistical challenges. Government directives limiting LNG supply have begun impacting rolling and heating operations at several stainless steel mills. According to industry sources, production schedules at some facilities were disrupted by around 10-15%, tightening supply and lending support to prices.

Finished flats prices surge

BigMint’s benchmark 304 HRC was assessed at INR 205,000/t ex-Mumbai, up INR 10,000/t w-o-w, while 316 HRC increased by INR 12,000/t w-o-w to INR 360,000/t.

A major stainless steel coil producer raised prices, effective 9 March, increasing 304/304L grades by INR 7,000/t, 316/316L by INR 10,000/t, and JT grades by around INR 3,500/t, citing higher input costs and global uncertainties.

Meanwhile, freights across regional trade routes surged sharply, with shipping costs from Southeast Asia nearly doubling in recent weeks. As a result, imports of stainless steel flats remained subdued, as higher freight charges and war-related disruptions reduced the viability of overseas purchases for Indian buyers. Market participants also reported container delays amid heightened geopolitical tensions.

Global raw material pressures intensify

Global stainless steel cost pressures also strengthened after Indonesia’s Tsingshan raised its 304 stainless steel export offers by $50/t on 10 March, with Southeast Asia HRC offers heard at $1,980-2,010/t. Market participants noted that export prices have risen by nearly $65/t since the Lunar New Year, reflecting rising raw material costs.

The increase was largely driven by firm ferro nickel prices and tighter nickel ore availability from Indonesia. The Indonesian government set the 2026 nickel ore mining quota (RKAB) at 260-270 million tonnes (mnt), significantly lower than last year’s 379 mnt, tightening raw material supply.

Finished longs segment remains weak

In the longs segment, 304L (25-100 mm) black round bars were assessed at INR 168,000/t ex-Mumbai, up INR 2,000/t w-o-w. Meanwhile, 316L black round bars increased by INR 5,000/t to INR 300,000/t ex-Mumbai, supported by higher alloy input costs.

Export activity remained muted, with no fresh bookings reported from major mills as suppliers adopted a wait-and-watch approach amid ongoing geopolitical uncertainty.

Raw material scenario

Outlook

Indian stainless steel prices are expected to remain supported in the near term if geopolitical tensions persist. Continued supply disruptions, higher logistics costs, and energy constraints may further tighten market availability and sustain price levels.

Leave a Reply