- Liquidity crunch, geopolitical tensions pressure market

- LME nickel tags rise on softer USD, possible Fed rate cuts

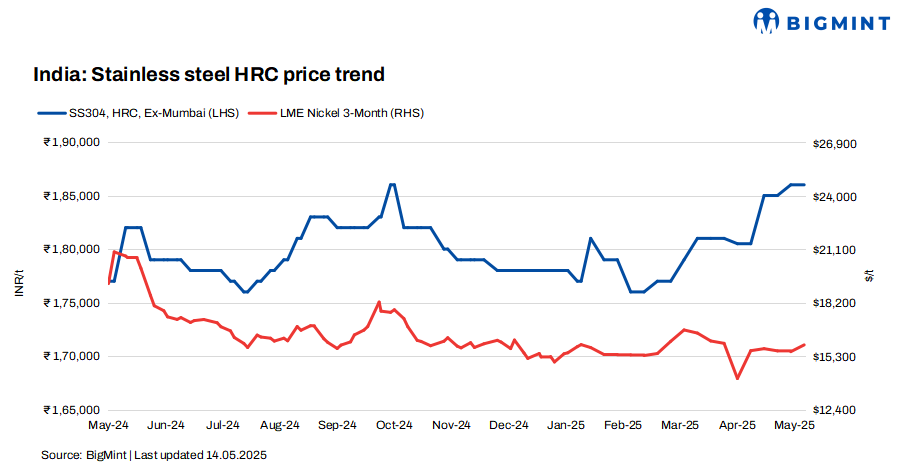

India’s stainless steel (SS) finished tags remained steady w-o-w this week, following a price hike by a major coil maker last week. Weak demand prevented price movements, with buyers adopting a cautious approach and limiting purchases.

Price assessments

BigMint’s benchmark assessment for stainless steel 304 series hot-rolled coils (HRCs) stood at INR 186,000/tonne (t), while 304L (25-100 mm) black round bars stood at INR 160,000/t, both ex-Mumbai and stable w-o-w.

Additionally, as per BigMint’s assessment, SS 316 HRCs stood at INR 325,000/t and 316 cold-rolled coils (CRCs) at INR 331,000/t ex-Mumbai, both stable w-o-w.

Meanwhile, SS 316L black round bars were priced at INR 270,000/t, while 316L (25-100 mm) bright bars were at INR 286,000-288,000/t, both ex-Mumbai. Furthermore, SS 304 (5-16 mm) wire rods stood at INR 156,000/t ex-Mumbai. Prices of all products were steady w-o-w.

LME nickel tags up, Asian NPI falls w-o-w

At the time of reporting, three-month nickel prices on the London Metal Exchange (LME) stood at $15,940/t, up by 2.5% against last week’s $15,565/t. Nickel stocks in LME-registered warehouses stood at 197,754 t, a minor decline compared to 200,082 t in the previous week.

Nickel prices experienced an uptick, driven by a softer US dollar and growing expectations of Federal Reserve interest rate cuts. The US Consumer Price Index (CPI) rose by 0.2% in April, falling short of market expectations and leading to a weaker dollar index. Coupled with the recent reset of US-China tariffs, the development fuelled speculation that the Federal Reserve may begin cutting interest rates in the coming months. These factors helped push up nickel prices.

Chinese portside prices of nickel pig iron (NPI) (grade 13%>Ni>10%) dropped by RMB 20/t ($2/t) w-o-w at RMB 948/metric tonne unit (mtu) ($134/mtu). Meanwhile, Indonesian FOB prices of NPI (grade 13%>Ni>10%) stood at $113/mtu.

India’s finished market sentiments

India’s stainless steel demand remained weak. According to a market participant, “Demand in the stainless steel market remained weak, with even export activity showing little momentum. There is no major work happening; only need-based buying has been seen.”

Another source noted, “Project-based activity has also slowed noticeably in recent days, likely influenced by ongoing geopolitical tensions and cautious sentiment across the sector.”

As per a source, “Sluggish sales of finished goods have led to liquidity constraints across the market. Additionally, the subdued market environment continues to pressure both producers and traders, limiting their ability to stimulate activity or improve margins.”

Adding to this, the Indian Stainless Steel Development Association (ISSDA) has raised concerns over a 3% y-o-y rise in cheap imports to 1.73 million tonnes (mnt) in FY’25, urging safeguard measures to protect domestic manufacturers. Market participants remained cautious amid these challenges.

Chinese stainless steel prices steady

In China, prices of domestic stainless steel 304-grade cold-rolled coils (CRCs) stood at RMB 13,850/t ($1,922/t) exw, stable w-o-w, while FOB tags of 304-grade CRCs were at $1,910/t.

Despite recent US tariff reductions, China’s stainless steel exports continued to encounter significant hurdles. While some duties were reduced, substantial tariffs remained on key products such as pipes and flanges, maintaining pressure on Chinese manufacturers. This persistent trade friction points to the limited impact of tariff adjustments on alleviating export challenges for China’s stainless steel industry.

Raw materials overview

Ferro molybdenum: Indian ferro molybdenum prices declined by INR 37,000/t ($433/t) w-o-w to INR 2,504,000/t ($29,335/t) exw, under pressure from bid-offer disparities.

Ferro chrome: Indian high-carbon ferro chrome (HC60%, Si:4%) prices were at INR 100,400/t ($1,175/t) exw-Jajpur, stable w-o-w.

Ferro silicon: Indian ferro silicon (70%) prices fell slightly by INR 800/t ($9/t) as compared to the previous assessment on 5 May.

As per BigMint’s assessment on 12 May, ferro silicon prices in India were at INR 94,700/t ($1,115/t) exw-Guwahati.

Ferrous scrap: India’s imported scrap prices edged up w-o-w last week. EU-origin shredded increased by $3-4/t w-o-w to $372/t CFR Nhava Sheva, while HMS 80:20 remained stable at $350/t CFR.

Demand remained subdued today due to a wide gap between bids and offers. Although inquiries improved, they were still below workable levels, keeping negotiations ongoing. The market continued to be weighed down by weak domestic steel demand, regional geopolitical tensions, and the approaching monsoon season.

Outlook

In the near term, prices are likely to be range-bound, with further declines for both raw and finished stainless steel materials unlikely. However, a significant rebound is not expected; any upward movement in prices is expected to be modest and gradual.

Leave a Reply