- Ferro molybdenum prices rise, lifting 316 tags

- LME nickel inventories increase to 4-year high

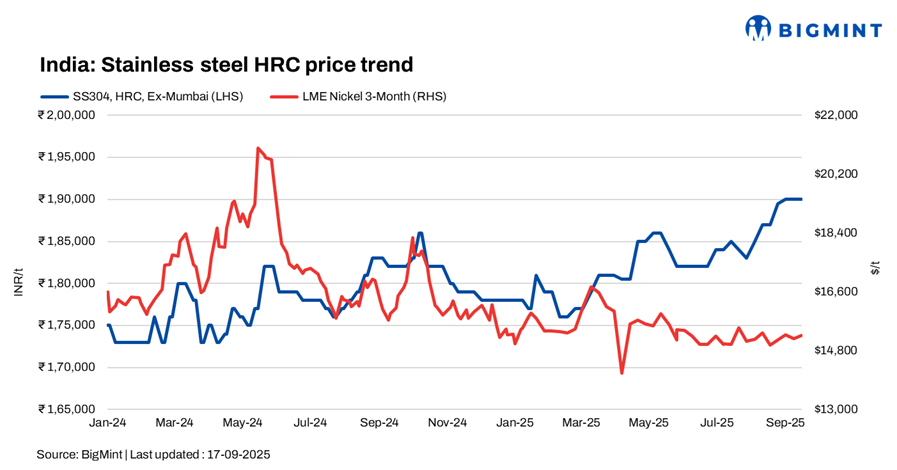

India’s stainless steel finished flats prices showed mixed trends w-o-w in a narrow range. The market remained stagnant this week, with 304-series prices unchanged, while 316-series tags edged up on firm molybdenum costs. Mills are also considering another price hike driven by rising input costs.

BigMint assessed 304-series hot-rolled coils (HRCs) at INR 190,000/tonne (t) ex-Mumbai, stable w-o-w, while 304L black round bars (25-100 mm) stood at INR 160,000/t, up by INR 2,000/t.

In contrast, 316-series HRCs stood at INR 345,000/t and cold-rolled coils (CRCs) at INR 350,000/t, both gaining by INR 5,000/t w-o-w.

As per a market participant, “Finished flats demand remained moderate. Only the fabricator and pipes and tubes sectors remained somewhat active.”

Finished longs sales remained low to moderate amid the availability of competitive semis in the market.

LME nickel tags remain range-bound w-o-w

At the time of reporting, three-month nickel prices on the London Metal Exchange (LME) stood at $15,265/t, up 0.8% from last week’s $15,160/t. Nickel stocks at LME-registered warehouses stood at 226,434 t, up 3.8% compared to 218,070 t in the previous week.

According to data released by the LME, nickel inventories have surged significantly over the past two weeks. On 16 September 2025, LME nickel stocks increased by 1,950 t, reaching a total of 226,400 t, the highest inventory level recorded in four years. During 2024, LME nickel inventories expanded by approximately 96,000 t, with the largest monthly rise occurring in February 2025, when stocks jumped by around 22,000 t. Notably, in just the first half of September 2025, inventories have already climbed by 17,000 t.

Chinese stainless steel, NPI prices remain stable

In China, prices of domestic stainless steel 304-grade CRCs stood at RMB 13,000-13,500/t ($1,829-1,900/t) exw, while FOB tags of 304-grade CRCs were firm at $1,900/t.

Chinese portside prices of nickel pig iron (NPI) (8-12%) remained firm w-o-w at RMB 954/t ($134/t). Meanwhile, Indonesian FOB prices of NPI (12-14%) stood at $119/t.

Raw materials scenario

Ferro molybdenum: Indian ferro molybdenum prices declined by INR 56,000/t ($638/t) as compared to the previous assessment on 10 September. Prices dropped due to lower domestic inquiries and a fall in LME futures, along with global tags.

Ferro molybdenum prices were at INR 3,110,000/t ($35,418/t) exw-India, as per BigMint’s assessment on 17 September.

Ferro chrome: Indian high-carbon ferro chrome (HC60%) prices rose INR 600/t w-o-w to INR 117,500/t ($1,337/t) exw-Jajpur.

Ferro silicon: Indian ferro silicon (70%) prices increased by INR 3,000/t ($34/t) in comparison to the assessment on 8 September.

As per BigMint’s assessment on 15 September, ferro silicon prices were at INR 89,000/t ($1,010/t) exw-Guwahati. In Bhutan, prices went up by INR 2,400/t ($27/t) w-o-w to INR 88,400/t ($1,003/t) exw.

Ferrous scrap: India’s imported scrap market remained sluggish today, with containerised shredded holding at $360-365/t CFR Nhava Sheva and HMS at $330-335/t CFR. Mills refrained from fresh bookings as rupee weakness, low domestic steel prices, and a $15-20 bid-offer gap curbed interest. Offers were heard from Bahrain at $355/t against bids of $340-345/t, UK HMS at $335/t versus bids of $320-325/t, Poland 2% HMS at $335/t, and Brazil 2% at $340/t. The seasonal slowdown and weak finished steel demand further dampened sentiment, leaving the market quiet with no recent sales heard. Buyers continued to lean on cheaper domestic scrap over imports, keeping overall activity subdued.

Outlook

India’s stainless steel market is poised for upward momentum in the near term, driven by rising raw material costs and global sentiment. Overall, the market outlook remains moderate, with trading expected to pick up in the upcoming week, supported by strong domestic demand.

Leave a Reply